SoFi's 2025 Stock Surge: Can the Momentum Last Amid Macroeconomic and Competitive Headwinds?

The Numbers: A Rocket Ship of Revenue and Profitability

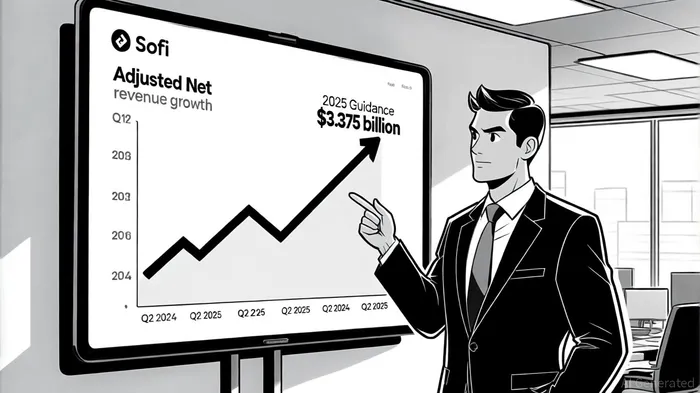

SoFi's Q2 2025 earnings report was nothing short of explosive. Adjusted net revenue hit a record $858.2 million, a 44% year-over-year jump, while fee-based revenue-its lifeblood-soared 72% to $377.5 million, according to an earnings beat. The company added 850,000 new members in the quarter, bringing its total to 11.7 million, and expanded its product base to 17.1 million, as noted in the Q2 report. Even more impressive: GAAP net income hit $97.3 million, and adjusted EBITDA surged 81% to $249.1 million.

SoFi didn't just meet expectations-it raised the bar. The company now forecasts $3.375 billion in adjusted net revenue for 2025, a 30% growth rate. This isn't just a one-quarter miracle; it's a reflection of SoFi's ability to scale its Financial Services Productivity Loop, a model that cross-sells multiple products to members, deepening relationships and boosting profitability.

Macroeconomic Tailwinds-and a Few Storm Clouds

The broader economic backdrop has been a mixed bag. The Federal Reserve's rate cuts in Q3 2025, noted in a quarterly markets review, have reignited demand for loans, a critical part of SoFi's business. Lower rates mean cheaper borrowing for consumers, which should boost SoFi's lending volumes. But here's the catch: If rates stay "higher for longer," as some economists predict, a TastyReferrals analysis warns that SoFi's growth could stall. High rates make loans more expensive, slowing member acquisition and squeezing net interest margins.

Inflation is also easing, with the Global Macroeconomic Outlook projecting global rates to drop to 5.43% in 2025. That's good news for consumer spending, which fuels SoFi's fee-based revenue. However, a potential economic downturn could lead to higher loan defaults, threatening credit quality, according to a Panabee analysis. SoFi's management has shown it can navigate these risks-its Q2 net income was a record despite macro volatility-but the road ahead isn't without potholes.

Competitive Pressures: Can SoFi Keep Its Crown?

SoFi isn't just competing with fintech startups; it's up against giants like PayPal, Robinhood, and even traditional banks like Bank of America, according to MarketBeat. Yet, SoFi's dominance is undeniable. It holds a staggering 99.70% market share, per CSIMarket, a testament to its integrated platform and national bank charter, which gives it access to low-cost deposits.

But competition is heating up. Rivals are investing heavily in AI-driven personalization and embedded finance, areas where SoFi is also innovating. The company's recent foray into blockchain-based remittances and AI-powered tools like "Cash Coach," as noted in an earnings write-up, is a smart move to stay ahead. However, with 69% of fintech firms now profitable, per a DigitalSilk report, the race for market share is only intensifying.

Regulatory Risks: A Double-Edged Sword

The regulatory landscape in 2025 has been a rollercoaster. The CFPB's deregulatory push-scrapping rules on open banking and payday lending-has reduced compliance costs for SoFi, according to a June regulatory update. But this deregulation has also led to a patchwork of state-level regulations, increasing operational complexity, a point emphasized in a Forbes analysis. For example, Massachusetts now requires stringent AI underwriting standards, per a Venable review, which could slow SoFi's product launches.

SoFi's national bank charter is a buffer here, but it's not foolproof. If states continue to impose conflicting rules, the company could face higher costs and slower innovation cycles.

The Verdict: A High-Volatility Bet with Long-Term Potential

SoFi's 2025 growth story is built on a foundation of strong financials, strategic innovation, and a favorable macroeconomic environment. Its ability to raise guidance and maintain profitability in seven consecutive quarters is a green light for bulls. But the stock's beta of ~1.9 means it's a high-volatility play.

The key risks? A prolonged high-rate environment, regulatory fragmentation, and margin compression in its lending business. However, SoFi's diversified revenue streams-spanning loans, investing, and blockchain-provide a buffer. If the company can maintain its cross-sell rate (targeting 1.7 products per member by year-end) and execute its AI and crypto relaunch plans, it could cement its position as a top-10 financial institution.

For now, SoFi remains a compelling-but not risk-free-bet. Investors should keep a close eye on Q3 earnings in October on the earnings calendar and watch for any signs of slowing growth.

Comentarios

Aún no hay comentarios