Smiths Group's Strategic Reinvention: A Catalyst for Sustained Shareholder Value

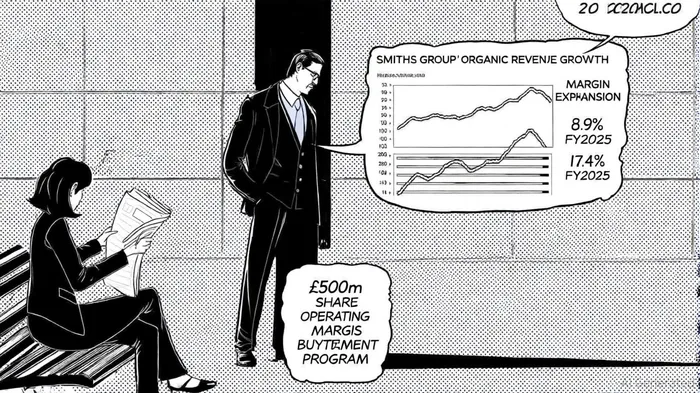

Smiths Group's FY2025 results have ignited a compelling narrative of operational reinvention. The company not only outperformed its revenue guidance by delivering 8.9% organic growth but also expanded its operating margin to 17.4%, a testament to its disciplined cost management and strategic refocusing[1]. This performance, coupled with a £500m share buyback program—nearly 80% completed by September 2025—signals a transformation that is redefining its competitive positioning and unlocking value for shareholders[1].

Strategic Restructuring: Sharpening the Focus

At the heart of Smiths Group's turnaround is a strategic overhaul aimed at divesting non-core assets and concentrating on high-margin industrial technologies. The planned separation of Smiths Interconnect and Smiths Detection—either via demerger or sale—reflects a calculated move to streamline operations[2]. By exiting these businesses, the company is reallocating capital to its core divisions, John Crane and Flex-Tek, which dominate high-performance flow and heat management solutions. Flex-Tek, in particular, has surged ahead, posting high single-digit revenue growth in aerospace and construction, sectors poised to benefit from global infrastructure spending[2].

This refocusing is not merely defensive. Smiths Group's £500m share buyback program, accelerated to return capital to shareholders, underscores its confidence in a leaner, more agile structure[1]. Morningstar analysts note that the company's 16.7% margin expansion in H1 2025 and 17.4% operating margin by year-end validate the effectiveness of its cost-cutting measures and operational discipline[3]. Such metrics suggest that the firm is transitioning from a diversified industrial conglomerate to a specialized engineering leader, a shift that could enhance its valuation multiples.

Operational Resilience and Market Positioning

Smiths Group's ability to navigate headwinds further strengthens its case for long-term value creation. A recent cyberattack on John Crane's energy division—a sector critical to its growth—was swiftly contained, demonstrating operational resilience[2]. Similarly, concerns over U.S. tariffs have been mitigated by the company's “local-for-local” manufacturing model, which minimizes exposure to cross-border trade shocks[2]. These capabilities, combined with a 10.6% revenue surge in Q3 2025, highlight its adaptability in volatile markets[2].

The company's 3-4% R&D investment as a percentage of revenue also positions it to capitalize on emerging trends, such as decarbonization and advanced materials, in its core markets[1]. For instance, Flex-Tek's innovations in heat management systems align with the aerospace industry's push for fuel efficiency, a trend expected to drive demand for decades.

Shareholder Value: A Dual Engine of Growth

Smiths Group's strategic initiatives are creating a dual engine for shareholder returns: operational efficiency gains and capital deployment discipline. The 170 basis-point rise in return on capital employed (ROCE) to 18.1% in FY2025[1] illustrates improved asset utilization, while the 5.1% dividend increase and £500m buyback program signal a commitment to rewarding equity holders[1]. Analysts at The Financial Analyst argue that the separation of Smiths Interconnect—expected by year-end—could unlock $1.2 billion in shareholder value, based on precedent transactions in the industrial sector[2].

However, risks remain. The success of the demerger hinges on securing favorable terms for Smiths Detection, a business with niche but high-margin capabilities in security technology. Delays or undervaluation in the disposal process could temper short-term gains. Additionally, while Flex-Tek's growth is robust, its exposure to cyclical sectors like aerospace means earnings could fluctuate with macroeconomic shifts.

Conclusion: A Compelling Case for Long-Term Investors

Smiths Group's FY2025 outperformance is more than a one-off triumph—it is the product of a deliberate, multi-year strategy to simplify its business and focus on high-conviction markets. With organic revenue growth guidance of 4-6% for FY2026[1] and a balance sheet rated for investment-grade stability[1], the company appears well-positioned to sustain its momentum. For investors, the combination of margin expansion, disciplined capital returns, and strategic clarity presents a compelling case. As Roland Carter, CEO, aptly stated: “Our transformation is not just about today—it's about building a business that thrives in the decades ahead.”[1]

Comentarios

Aún no hay comentarios