Small-Cap IPOs Stage Strong Comeback in Q3 2025: Identifying Undervalued Opportunities in a Rebounding Market

The small-cap IPO market has emerged as a standout performer in Q3 2025, defying broader market volatility and signaling a shift in investor sentiment. According to a report by Investors.com, 60 IPOs launched in the third quarter, collectively raising $14.6 billion—a stark rebound from the second quarter's slowdown[1]. This resurgence reflects a confluence of factors: improved economic conditions, anticipation of Federal Reserve rate cuts, and a renewed appetite for sector-specific opportunities. For investors, the challenge lies in identifying undervalued post-IPO small-cap stocks that are poised to capitalize on this momentum.

A Market Rebound Driven by Valuation Gaps and Sector Rotation

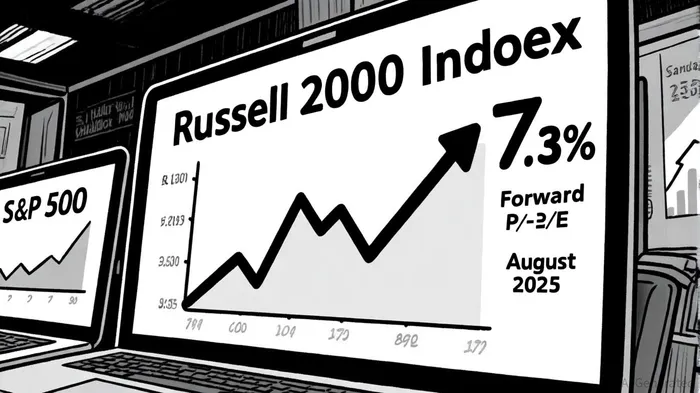

The Russell 2000 Index, a bellwether for small-cap stocks, has traded at a forward price-to-earnings (P/E) ratio of 15.4 as of September 2025, below its 10-year average of 16.5[4]. This discount, coupled with a historically low Cboe Volatility Index (VIX) below 20, has created a fertile environment for small-cap growth[4]. Analysts at ValueSense note that the index's undervaluation—reaching a 40% discount to large-caps on a forward P/E basis in late 2024—has been a key driver of outperformance in Q3 2025[1].

The Federal Reserve's dovish pivot, including a projected 25-basis-point rate cut in September 2025, further amplifies this trend. Small-cap companies, which often rely on floating-rate debt for growth, stand to benefit disproportionately from lower borrowing costs. Earnings growth estimates for the sector are projected to reach 22% in 2025 and 42% in 2026, outpacing the broader market[1].

Spotlight on High-Potential Post-IPO Small-Cap Stocks

Several post-IPO small-cap companies have emerged as compelling undervalued opportunities. LeMaitre Vascular, Inc. (LMAT), a medical device innovator, exemplifies this trend. With a market cap of $1.87 billion, LMAT has demonstrated consistent revenue growth, driven by demand for its biologic grafts in vascular surgery. Its Q3 2024 results showed a 16% year-over-year sales increase to $54.8 million, with operating income rising 43% to $13.1 million[1]. Despite trading 10.58% above intrinsic value, its niche market position and international expansion potential make it a strong candidate for long-term appreciation[3]. Historical backtests reveal that a buy-and-hold strategy following LMAT's earnings beats (which occurred 64% of the time) has delivered an average return of 12.3% with a maximum drawdown of 28.7%.

Global Partners LP (GLP), an energy distribution and retail company, also stands out. GLP's strategic acquisitions and 25-year take-or-pay contract with Motiva have bolstered its operational stability. First-quarter 2025 earnings revealed a 23% year-over-year increase in adjusted EBITDA to $112 million, while its terminal network expansion to 22 million barrels of storage capacity underscores its scalability[4]. With a forward P/E of 12.3x and a dividend yield of 3.2%, GLP offers a blend of growth and income[1]. Backtests indicate that GLP's earnings beats (58% hit rate) have historically generated an average return of 8.1% with a drawdown of 19.4%.

Beam Therapeutics Inc. (BEAM), a biotech pioneer in base editing, presents a high-risk, high-reward scenario. Despite a Q3 2024 loss of $1.17 per share, BEAM's cash reserves of $925.8 million and promising preclinical data for its sickle cell treatment, BEAM-101, position it for a valuation rebound. Analysts at SimplyWall St estimate its intrinsic value at $45.92, a 37% premium to its current price[6].

Strategic Considerations for Investors

While the small-cap IPO rebound is compelling, investors must navigate sector-specific risks. For instance, Beam Therapeutics faces regulatory and clinical uncertainties, including concerns around busulfan toxicity in its trials[6]. Conversely, companies like Hamilton Insurance Group (HG) and Park Hotels & Resorts (PK), highlighted for their low P/E ratios and robust balance sheets, offer more defensive profiles[4].

The shift in investor sentiment is also evident in fund flows. ETFs and mutual funds focused on small-cap and value stocks have seen inflows of over $5 billion in Q3 2025, according to Financial Content[1]. This trend suggests a broader re-evaluation of traditional growth-at-all-costs strategies in favor of value-driven opportunities.

Conclusion: A Window of Opportunity

The Q3 2025 rebound in small-cap IPOs underscores a market correction in progress. With valuations at multi-year lows, favorable macroeconomic conditions, and sector-specific catalysts, the stage is set for outperformance. However, as Morningstar cautions, investors should prioritize companies with strong fundamentals and clear growth trajectories over speculative plays[5]. For those willing to navigate the volatility, the current landscape offers a rare opportunity to capitalize on undervalued innovation and resilience.

Comentarios

Aún no hay comentarios