Slowing U.S. Job Growth: Early-Warning Signals and Equity Valuation Implications

The U.S. labor market is showing signs of strain, with August 2025's employment report underscoring a marked slowdown in job creation. According to CNBC's jobs report, nonfarm payrolls rose by just 22,000 in August, far below the forecasted 75,000. The unemployment rate climbed to 4.3%, reflecting a weakening labor market, according to a Kansas City Fed bulletin. Revisions to prior months' data further cloud the picture: June's figures were downgraded by 13,000 jobs, while July saw a modest upward adjustment of 6,000, as CNBC reported. These trends, coupled with sector-specific divergences, signal early-warning signals for investors to monitor.

Labor Market Indicators: JOLTS and Wage Trends

The July 2025 JOLTS report paints a picture of a stagnant labor market. Job openings fell to 7.2 million, with a quits rate of 2%-a historically low level that suggests workers are less inclined to switch jobs, as CNBC noted. This lack of dynamism has dampened wage growth for job switchers, a key driver of broader wage inflation. Meanwhile, average hourly earnings in August rose by 0.3%, slightly below expectations, according to the Kansas City Fed. While the Federal Reserve's preferred inflation metrics have cooled, the combination of low quits and flat wage growth indicates a labor market that is neither overheating nor collapsing-yet.

Historical context reveals that such conditions often precede equity valuation shifts. During the Great Recession (2007–2009), prolonged unemployment and productivity stagnation led to hysteresis effects, where employment levels failed to rebound to pre-crisis norms, as CNBC reported. Similarly, the post-pandemic labor market rebound was rapid but uneven, contrasting with the Great Recession's prolonged slump, according to the Kansas City Fed. These patterns highlight the importance of sector-specific analysis in assessing equity risks.

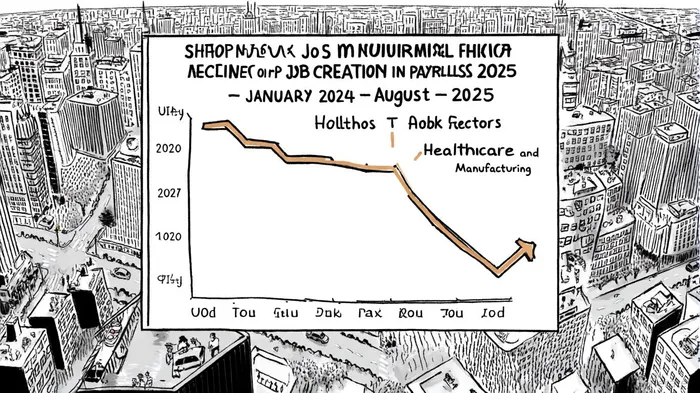

Sector-Specific Impacts and Equity Valuations

Healthcare and social assistance have emerged as a bright spot, adding 31,000 jobs in August 2025, CNBC reported. This resilience, driven by an aging population and stable demand, has likely supported equity valuations for firms in this sector. Conversely, manufacturing and trade-exposed industries have faced headwinds, with manufacturing shedding 12,000 jobs in August and 78,000 since January 2025, as CNBC noted. Federal spending cuts, tariff uncertainty, and supply chain disruptions have compounded these challenges, weighing on corporate margins and equity valuations.

The technology sector, meanwhile, reflects a boom-and-bust cycle. Rapid hiring during the post-pandemic recovery gave way to a sharp slowdown as the Federal Reserve raised interest rates, leading to job cuts and compressed valuations, according to a BLS analysis. Nonprofessional services, particularly leisure and hospitality, have shown mixed performance, with strong growth in some periods and moderation in others, as noted by the Kansas City Fed. These sector-specific trends underscore the uneven nature of the labor market slowdown and its cascading effects on equity markets.

Policy Implications and Market Outlook

The anticipation of a Federal Reserve rate cut in September 2025 adds another layer of complexity. As job growth decelerates and unemployment rises, investors are pricing in a 25-basis-point cut at the FOMC's September meeting, according to the Kansas City Fed. Lower interest rates could buoy interest-sensitive sectors like housing and real estate investment trusts (REITs), while consumer discretionary sectors may struggle if the economic slowdown persists. Banking stocks face a dual challenge: reduced net interest margins from lower rates could offset potential gains from increased loan demand.

For growth stocks, particularly in technology, a lower discount rate environment may provide some relief. However, valuations remain stretched compared to historical averages, raising concerns about overvaluation, according to BlackRock's equity outlook. The S&P 500's strong performance in 2025, driven by outperforming earnings and broad-based sector participation, may not be sustainable if labor market weakness persists, BlackRock observes.

Conclusion

The U.S. labor market is at a crossroads, with early-warning signals pointing to a potential inflection point for equity valuations. While healthcare and resilient sectors offer defensive opportunities, manufacturing and technology face near-term headwinds. Investors must remain vigilant to sector-specific risks and the Federal Reserve's policy response. As the September rate cut looms, the interplay between labor market dynamics and monetary policy will likely shape the next chapter of equity market performance.

Comentarios

Aún no hay comentarios