Slovakia's Fiscal Austerity Measures: Implications for European Emerging Markets Investors

Slovakia's 2025 fiscal austerity measures, aimed at reducing a 5.9% budget deficit through €2.7 billion in savings, have ignited a contentious debate over their economic and political consequences. While the government frames these measures as essential for fiscal discipline and credibility, the immediate fallout—public protests, a sharp slowdown in domestic consumption, and sectoral contractions—raises critical questions for investors in Central European equities. For European emerging markets investors, the challenge lies in balancing the short-term pain of austerity with the long-term promise of fiscal stability and structural reforms.

The Austerity Experiment: Winners and Losers

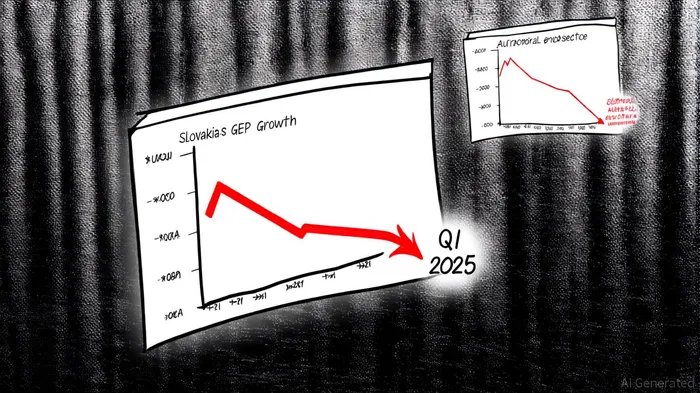

The Slovak government's consolidation package, enacted in October 2024, included tax hikes on higher earners, a VAT increase on certain food products, and cuts to social benefits like the child tax bonus [1]. These measures, while targeting deficit reduction, have disproportionately burdened middle- and working-class households. According to a report by SME Spectator, Slovakia's GDP growth in Q1 2025 fell to 0.9% year-on-year, the weakest in two years, as consumer spending on durable goods plummeted—car registrations dropped 13% year-on-year [2].

The automotive sector, a cornerstone of Slovakia's export-driven economy, has been particularly hard hit. With car production accounting for roughly 12% of GDP, reduced domestic demand and global trade tensions (notably U.S.-EU tariff disputes) have compounded challenges. Bloomberg analysts note that Slovakia's fiscal tightening has exacerbated these vulnerabilities, creating a drag on regional supply chains and investor confidence [3].

Investor Sentiment and Equity Market Reactions

The equity market response to Slovakia's austerity measures has been mixed. While the government's commitment to fiscal discipline has reassured bond investors—Slovakia's 10-year bond yields fell by 30 basis points in early 2025—equity markets have remained cautious. The MSCI Central Europe Index, which includes Slovak firms, underperformed its European peers in Q1 2025, reflecting concerns over domestic demand and policy uncertainty [4].

Sectoral shifts highlight the risk-adjusted return dynamics. Defensive sectors like utilities and healthcare have outperformed, while cyclical sectors such as automotive and consumer discretionary lagged. A Goldman Sachs analysis underscores that European equities, including those in Central Europe, trade at a 5% discount to fair value estimates amid trade uncertainties, but sectoral disparities persist [5]. For investors, the key question is whether these dislocations represent opportunities or red flags.

Regional Contagion Risks and Macroeconomic Spillovers

Slovakia's fiscal experiment is not isolated. Central European economies, including Poland and Hungary, face similar pressures to balance fiscal consolidation with growth. The European Central Bank's Financial Stability Review warns that interconnected financial systems amplify contagion risks, particularly in export-dependent economies [6]. For instance, a slowdown in Slovakia's automotive sector could ripple through regional supply chains, affecting German and Czech manufacturers.

Moreover, the political backlash against austerity measures—thousands protested in Bratislava in September 2025—signals broader social unrest risks. Such instability could deter foreign direct investment and delay the implementation of structural reforms, further complicating the region's growth trajectory.

The Path Forward: Caution or Opportunity?

For investors, the calculus hinges on two factors: the efficient use of EU recovery funds and the resolution of global trade tensions. Slovakia's access to €12 billion in EU recovery grants could offset some of the austerity-driven drag, but execution risks remain. The IMF has emphasized that without structural reforms to diversify the economy and boost productivity, Slovakia's long-term growth prospects will remain constrained [7].

In the short term, risk-adjusted returns in Central European equities appear mixed. Defensive allocations and high-dividend sectors may offer stability, while cyclical sectors face headwinds. However, the potential for a rebound in 2026—driven by falling interest rates and improved fiscal transparency—could create asymmetric opportunities for patient investors.

Conclusion

Slovakia's austerity measures exemplify the delicate balancing act between fiscal responsibility and social stability. While the immediate economic pain is evident, the long-term success of these policies will depend on their implementation and the broader regional context. For European emerging markets investors, the lesson is clear: diversification, sectoral selectivity, and a close watch on macroeconomic spillovers will be critical in navigating the evolving landscape.

Comentarios

Aún no hay comentarios