SITE Centers' Strategic Divestiture and Capital Allocation Implications: A Real Estate Sector Repositioning

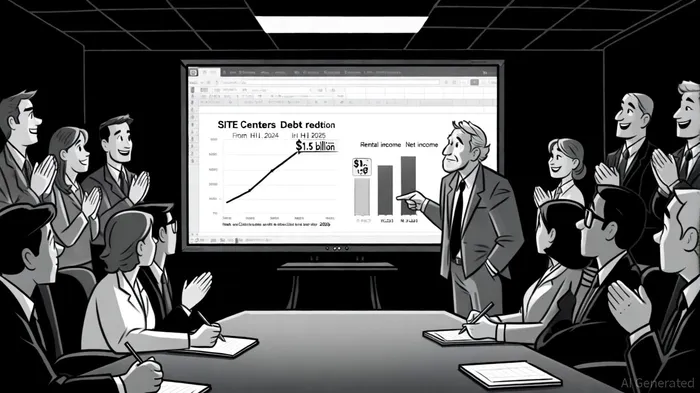

SITE Centers Corp. (NYSE: SITC) has embarked on a dramatic strategic overhaul in 2025, reshaping its portfolio and capital structure through aggressive divestitures. The company's decision to spin off 79 convenience properties in October 2024 and sell five additional shopping centers in the first half of 2025 has reduced its portfolio to 31 properties totaling 8.3 million square feet. While this has led to a 65% decline in rental income and a 76% drop in net income for the six months ending June 30, 2025 [2], the move has also slashed consolidated indebtedness by over 80%, from $1.5 billion to $0.3 billion [2]. This deleveraging effort has cut interest expenses by $26 million for the period, significantly lowering financial risk and freeing up capital for shareholder returns [2].

The company's capital allocation strategy has prioritized debt reduction and shareholder value. SITE CentersSITC-- has declared special dividends totaling $4.75 per common share in Q2/Q3 2025, distributing proceeds from asset sales directly to investors [2]. However, the remaining portfolio faces operational headwinds. New leases signed in the first half of 2025 exhibit a negative cash lease spread of -17.6%, and occupancy has fallen to 87.5% from 90.6% in December 2024 [2]. These challenges underscore the difficulty of maintaining rental income in a shrinking portfolio, even in high-income suburban locations.

SITE Centers' strategy aligns with broader trends in the real estate sector, where capital efficiency and debt reduction are increasingly prioritized over aggressive growth. According to a report by StepStone Insights, the 2025 real estate landscape is defined by a shift toward income-generating assets with stable cash flows, as investors seek resilience amid macroeconomic uncertainty [3]. The company's focus on necessity-anchored shopping centers—properties with essential retail tenants—has helped stabilize occupancy, but the broader sector faces structural challenges. For instance, the retail REIT industry's average P/E ratio of 26.9x in 2025 contrasts sharply with SITE Centers' negative P/E of -13.3x, reflecting its earnings volatility and market skepticism [1].

Analysts have mixed views on the company's valuation. Ladenburg Thalmann initiated coverage with a “Neutral” rating and a $10 price target, citing the need for further stabilization post-spinoff [1]. Meanwhile, J.P. Morgan Research notes that U.S. retail REITs, including SITE Centers, benefit from strong consumer spending and limited new supply, which support leasing activity and pricing power [6]. However, risks such as tariff-related economic slowdowns and rising labor costs could dampen tenant performance, particularly for smaller REITs like SITE Centers [4].

The company's capital-recycling approach—selling non-core assets, paying down debt, and reinvesting in redevelopment—positions it to stabilize core rental income and support shareholder-friendly policies. By Q2 2025, SITE Centers had generated $53.2 million in disposition gains, partially offsetting declining operating performance [3]. Yet, the path forward is not without hurdles. The company's debt reduction to $288.4 million as of June 2025 [3] must be balanced against potential refinancing costs for joint venture maturities in 2026/2027 and macroeconomic headwinds affecting tenant demand [3].

For investors, SITE Centers' strategic repositioning highlights the tension between short-term earnings volatility and long-term capital efficiency. While the company's debt reduction and dividend payouts enhance shareholder value, the negative lease spreads and occupancy declines signal operational fragility. In a sector where capital flows increasingly target distressed opportunities and recapitalization plays, SITE Centers' smaller, more focused portfolio could attract investors seeking undervalued assets with redevelopment potential [2]. However, the broader shift in demand from traditional retail to logistics and data centers suggests that SITE Centers' focus on suburban shopping centers may require further adaptation to remain competitive [5].

In conclusion, SITE Centers' 2025 divestitures and capital allocation strategy reflect a pragmatic response to sector-wide pressures. By prioritizing debt reduction and capital returns, the company has mitigated financial risk but exposed itself to operational challenges in a shrinking portfolio. For REIT investors, the key question is whether the company's leaner structure and focus on necessity retail can generate sustainable cash flows in a market increasingly defined by fragmented demand and structural shifts in property utilization.

Comentarios

Aún no hay comentarios