Singles' Housing Risk Matrix: O'Leary's Cautionary Framework for Cash Preservation

, the Shark Tank star and financial guru, advocates for a "five-year rule" that prioritizes renting over early homeownership. He argues that high closing costs and around 6–7% can erode returns for short-term homeownership. This approach aims to mitigate financial risk while singles build their careers and wealth.

By living within walkable distances of work, individuals save on transit costs and invest those savings instead of purchasing a home. O'Leary emphasizes delaying homeownership until long-term stability-such as starting a family-when community and school systems become more important. Current high rates make renting cheaper than buying in most major U.S. markets for first-time buyers, freeing capital for elsewhere.

However, this strategy isn't universally ideal. Those valuing long-term stability or planning to stay in one location may benefit more from owning. But for in uncertain market conditions, renting preserves flexibility and liquidity. The upfront savings from avoiding mortgages and closing costs can be redirected toward investments with potentially higher returns-though this requires disciplined execution and tolerance for rental volatility.

Visibility Decline & Policy Uncertainty: Core Risk Signals

Kevin O'Leary highlights a critical financial friction for single homebuyers: the risk of "visibility decline." When two singles form a partnership, their combined income visibility for lenders drops instantly from one documented salary to two potentially conflicting budgets, making mortgage qualification suddenly much harder. This shock can trap households in unaffordable payments if relocation or job loss occurs soon after purchase according to analysis. He specifically warns that singles facing this income restructuring risk forced sales during life transitions, incurring steep closing costs and minimal equity gains as research shows.

Compounding this personal financial vulnerability is policy instability. O'Leary notes how volatile interest rates directly attack single buyers' thin margins. With mortgage rates historically stuck near 6-7%, even a 0.5% spike can push payments beyond reach for earners with no backup income. Regional housing mandates further amplify uncertainty – rules limiting renovations or rentals reduce asset flexibility, while fluctuating property taxes erode cash flow predictability. For singles without financial buffers, these policy swings transform housing from wealth-building into high-stakes speculation.

O'Leary's prescribed defense hinges on liquidity preservation. He argues singles should defer homeownership until demonstrating five-year stability near their intended workplace, using the saved commuting costs and mortgage expenses to build investable capital instead. Renting provides the needed exit flexibility to avoid payment shocks, while disciplined investing creates a financial safety net immune to housing market volatility or policy shifts. This approach prioritizes cash reserves over illiquid assets precisely because singles face the highest visibility and regulatory risks in the housing market.

Liquidity Sacrifice & Opportunity Cost

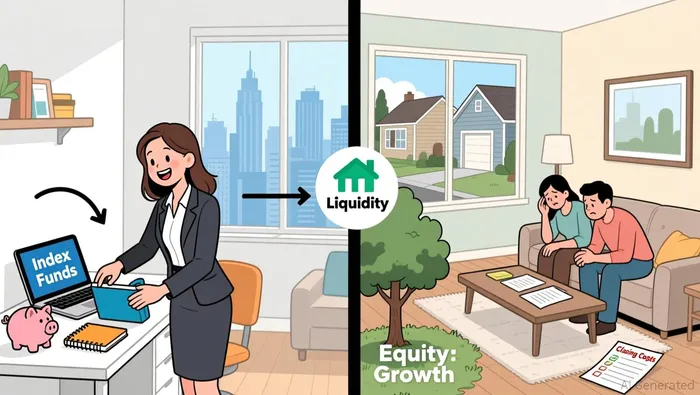

Building on the housing affordability challenges discussed earlier, premature homeownership carries hidden liquidity costs that can erode long-term wealth-building potential. Kevin O'Leary's "five-year rule" explicitly warns against this trap, citing 6–7% mortgage rates and closing costs that drain capital at a time when singles should prioritize flexibility according to financial analysis. His analysis shows renting becomes cheaper than buying in most major U.S. markets today, creating an opportunity to redirect commuting savings into liquid investments.

When singles lock capital into property, they sacrifice two key advantages: market-timing flexibility during corrections and access to high-yield opportunities. Index funds historically deliver 5–7% annual returns as data shows-returns that require capital to remain available during volatility dips. Homeownership, however, forces money into illiquid real estate, where equity gains stagnate under high rates. This inflexibility means missing chances to buy quality assets at discounts during market turmoil-a cost that compounds when combined with opportunity losses from stagnant home equity.

The liquidity sacrifice is most acute for singles without family commitments. Their capital becomes trapped in property, unable to respond to market catalysts or emergencies. While homeownership provides security later in life, the early exit imposes a portfolio rigidity that risks compounding opportunity costs during critical wealth-building years.

Comentarios

Aún no hay comentarios