The Simply Good Foods Company: A Cautionary Tale for Retail Investors

The premium snack sector, once a goldmine for innovation-driven brands, is now witnessing a shift in dynamics as consumer preferences evolve and competition intensifies. For retail investors, The Simply Good Foods Company (SMPL)—a key player in this space—has become a cautionary tale of declining market share and operational underperformance, despite its strategic acquisitions and brand diversification efforts.

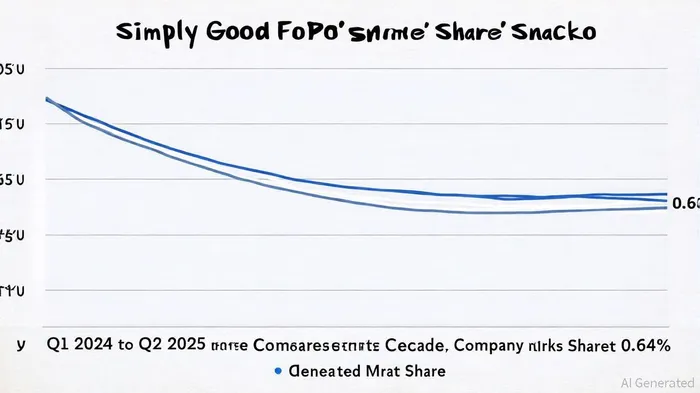

Market Share Erosion Amid Stagnant Growth

According to data from CSIMarket, Simply Good FoodsSMPL-- held a 0.64% market share in the premium snack sector during Q2 2025, a marginal decline from 0.66% in Q1 2025[1]. This represents a broader trend: while the company reported a 13.71% year-on-year revenue increase in Q2 2025, this growth lagged behind the industry average of 24.78% among its competitors[1]. The company's market share in the U.S. nutritional bar category, though robust at 13% as of 2023[4], contrasts sharply with its weak performance in the broader premium snack market.

The erosion of market share is particularly concerning given the company's reliance on high-margin brands like Quest and Atkins. Competitors such as CLIF Bar, KIND, and Special K have capitalized on shifting consumer demands for clean-label ingredients and functional benefits, further squeezing Simply Good Foods' position[1].

Operational Underperformance: A Closer Look

While Simply Good Foods boasts a 10.8% net margin—outpacing its peers—it has struggled to translate this into sustainable profitability. In Q2 2025, the company's net income fell by 0.56% year-on-year, a stark contrast to the 95.66% growth reported by competitors[1]. This discrepancy is partly attributed to soaring SG&A expenses. For the year-to-date period ending May 31, 2025, the company's SG&A expenses surged by 30% to $115.3 million, driven by OWYN integration costs and employee-related expenses[1]. As a percentage of revenue, these expenses reached 32.0%, far exceeding Conagra Brands' 13.88% and Campbell Soup's 10% in the same period[5][6].

Inventory management also raises red flags. The company's inventory to sales ratio of 9.31 in Q2 2025 fell below its historical average, signaling potential inventory buildup[1]. Meanwhile, peers in the Consumer Non-Cyclical sector achieved higher inventory turnover ratios, underscoring Simply Good Foods' operational inefficiencies[1].

Strategic Challenges and Investor Implications

The company's 2025 strategic priorities—diversification, innovation, and international expansion—aim to mitigate brand concentration risks[2]. However, these efforts have yet to offset the headwinds from rising costs and competitive pressures. For instance, the acquisition of OWYN, while expanding product offerings, introduced a non-cash inventory purchase accounting adjustment that reduced gross margins by 90 basis points in Q4 2024[3].

Retail investors should also note the company's gross margin of 38.8% in Q4 2024, a 120-basis-point improvement driven by lower ingredient costs[3]. Yet, this metric alone cannot compensate for the structural weaknesses in SG&A and inventory management.

Conclusion: A Ticking Time Bomb?

The Simply Good Foods Company's story is a reminder that even high-margin brands can falter in a hyper-competitive sector. While its net margin outperforms peers, the combination of declining market share, bloated SG&A expenses, and inventory inefficiencies paints a troubling picture. For investors, the key takeaway is clear: Simply Good Foods' operational underperformance and strategic vulnerabilities warrant caution. In a sector where agility and cost discipline are paramount, the company's current trajectory may not be sustainable.

Comentarios

Aún no hay comentarios