The Shifting Tides of Consumer Sentiment: A Strategic Inflection Point for U.S. Equity Sectors

The U.S. consumer-driven equity sectors are at a crossroads. Recent data from the University of Michigan Consumer Sentiment Index reveals a nuanced story: while short-term optimism about economic conditions has improved, long-term expectations remain clouded by inflationary fears and policy uncertainty. This duality—between near-term resilience and structural caution—has created a unique inflection pointIPCX-- for market leadership and tactical asset allocation. Investors must now navigate a landscape where consumer behavior is increasingly fragmented, with divergent impacts across sectors and demographics.

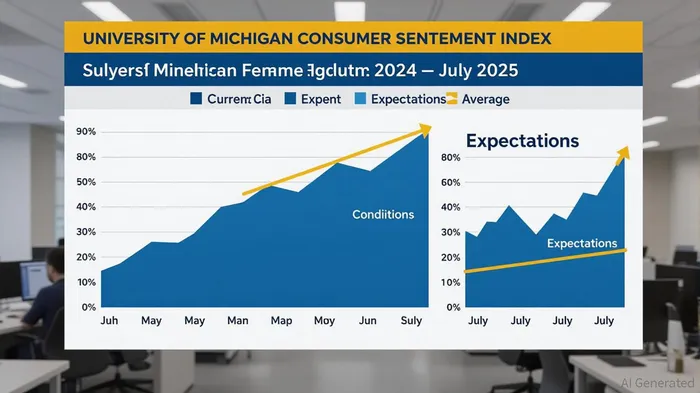

The Dual Forces of Consumer Sentiment

In July 2025, the Consumer Sentiment Index rose to 61.8, the highest level since February, driven by a 3.1% increase in the "Current Conditions" component to 66.8. This suggests that households are cautiously embracing near-term economic stability, particularly in employment and business activity. However, the "Expectations" component grew only marginally to 58.6, remaining 14.8% below its 2024 level. This gap reflects a critical psychological divide: while consumers are willing to spend on immediate needs, they remain wary of future risks, particularly inflation.

Inflation expectations have moderated slightly, with 12-month expectations dropping to 4.4% and long-run expectations to 3.6%—a welcome but incomplete normalization. These figures remain above the pre-pandemic benchmarks of 2.8% and 3.0%, underscoring lingering discomfort with pricing pressures. As Joanne Hsu, director of the Surveys of Consumers, noted, "Unless inflation risks stabilize, confidence will remain fragile." This dynamic has profound implications for equity sectors, as consumer spending patterns shift between essentials and discretionary items.

Sector Leadership: From Cyclical to Defensive

The interplay between sentiment and sector performance is already evident. Consumer discretionary and staples sectors have exhibited a mixed trajectory. Retail sales, while up 2.3% year-to-date through June, have been driven largely by services (e.g., travel, dining) rather than goods. Real retail sales, adjusted for inflation, have stagnated over six months, signaling a shift toward "experiences" over "things." This aligns with broader post-pandemic trends, where households prioritize spending on health, travel, and digital subscriptions over traditional retail categories like apparel or electronics.

The staples sector, meanwhile, has seen muted growth. Groceries and household goods have avoided the sharp price surges of recent years, but categories like eggs, meat, and baked goods remain elevated. This reflects a broader recalibration of consumer priorities: households are spending less on big-box retailers and more on essential, high-quality goods. The sector's resilience, however, is underpinned by structural factors, such as demographic shifts and the rising cost of living, which ensure steady demand for non-discretionary items.

Tactical Allocation: A Defensive Pivot

The current macroeconomic environment demands a tactical pivot toward defensive positioning. Global growth remains below long-term trends, and trade policy risks—exemplified by recent U.S. tariff announcements—threaten to reignite inflationary pressures. In this context, equity allocations should favor sectors with strong balance sheets, low volatility, and structural growth drivers.

- Health Care and Utilities: These sectors, with their stable cash flows and low sensitivity to trade cycles, are well-positioned to outperform. For instance, healthcare providers are trading at a forward P/E of 13x, below their historical average, offering attractive risk-adjusted returns.

- Consumer Staples: While valuations are stretched relative to long-term averages, the sector's defensive characteristics make it a cornerstone in a volatile market.

- Technology (Selectively): The AI and software subsectors remain pivotal, despite recent volatility. Falling compute costs are creating margin tailwinds, but investors should focus on high-quality, fundamentally strong companies rather than speculative plays.

Conversely, cyclical sectors like industrials, materials, and financials face headwinds. These sectors, which are more exposed to global trade and interest rate sensitivity, should be underweighted. The ISM Manufacturing Index's contraction to 48.5 in June 2025 underscores the fragility of the goods-producing economy, further reinforcing the need to avoid overexposure.

The Role of Inflation and Policy Uncertainty

The Federal Reserve's balancing act between inflation control and growth support remains a wildcard. While the recent decline in inflation expectations is encouraging, the risk of a "too-tight" policy environment persists. This uncertainty has pushed investors toward low-volatility strategies, with defensive sectors like utilities and staples acting as buffers against market downturns.

Moreover, the upcoming election cycle introduces additional volatility. Political shifts could alter trade policies, fiscal spending, and regulatory frameworks, all of which will influence consumer behavior and sector dynamics. Investors must remain agile, adjusting allocations in response to policy developments and sentiment shifts.

Conclusion: Positioning for Resilience

The U.S. consumer-driven equity sectors stand at a strategic inflection point. While near-term sentiment data suggests a cautious pivot toward defensive positioning, long-term structural trends—such as the rise of AI and the rebalancing of consumer priorities—offer growth opportunities. Tactical allocations should prioritize quality, low volatility, and sector-specific value, while remaining vigilant to macroeconomic and policy risks.

For investors, the key takeaway is clear: in an environment of fragmented growth and persistent uncertainty, resilience—not momentum—will define successful portfolios. By aligning allocations with the evolving contours of consumer sentiment, investors can navigate the shifting tides and position themselves for both stability and long-term returns.

Comentarios

Aún no hay comentarios