Shift4 Payments: A Post-M&A Buy Opportunity with a Clear Growth Path

Shift4 Payments, Inc. (NYSE: FOUR) has emerged as a compelling investment opportunity in the post-merger and acquisition (M&A) landscape, driven by its disciplined expansion strategy and robust financial performance. With a revised 2025 guidance of $1.66–$1.73 billion in gross revenue less network fees and a market cap of $7.84 billion as of September 8, 2025, the company is poised to capitalize on its strategic repositioning in the payments sector [1]. This analysis explores Shift4's valuation re-rating potential and its disciplined M&A-driven growth, supported by recent financial metrics and analyst insights.

Strategic Valuation Re-Rating: A Post-M&A Catalyst

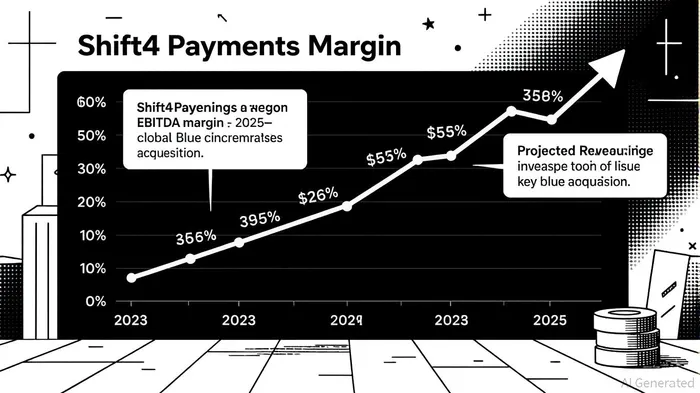

Shift4's recent acquisition of Global Blue Group Holding AG, funded by €680 million in 5.500% senior notes and $550 million in 6.750% senior notes, has reshaped its capital structure and market perception [2]. Despite concerns about financial leverage, analysts argue that the company's valuation remains attractive relative to historical averages and peers. For instance, its EBITDA margins reached 46% in Q1 2025, exceeding guidance, while its projected EBITDA margin expansion to over 50% in Q2 2025 underscores operational efficiency [2].

A report by Finimize highlights that Shift4's stock price of $86.47 reflects a discount to its intrinsic value, given its strong cash flow generation and cross-selling synergies from the Global Blue acquisitionBACC-- [2]. This suggests a re-rating potential as the market digests its expanded capabilities in digital payments and tax-free commerce.

Disciplined M&A-Driven Expansion: Fueling Long-Term Growth

Shift4's M&A strategy is characterized by strategic alignment with industry trends. The acquisition of Global Blue, a leader in cross-border tax-free retail, complements Shift4's core payment processing business, creating cross-selling opportunities and expanding its global footprint [2]. Analysts at DA Davidson and Benchmark have upgraded their ratings to Buy, with price targets of $124 and $111, respectively, citing the company's ability to integrate acquisitions profitably [2].

Financial performance reinforces this optimism. Shift4FOUR-- reported 30.68% year-over-year revenue growth in Q1 2025 and raised its full-year guidance, driven by higher payment volumes and cost discipline [2]. Projections indicate a 21.5% annual revenue growth rate and 40.6% earnings growth, with return on equity (ROE) expected to reach 34.7% in three years [1]. These metrics highlight the company's capacity to scale profitably while maintaining margins.

Analyst Outlook and Risk Mitigation

While leverage ratios remain a concern, Shift4's improved corporate family rating from Moody'sMCO-- and its track record of margin expansion mitigate risks [2]. The company's focus on high-margin verticals, such as digital payments and tax-free retail, further insulates it from macroeconomic volatility. Additionally, its revised 2025 guidance reflects confidence in sustaining growth amid competitive pressures from firms like American ExpressAXP-- and MarqetaMQ-- [2].

Conclusion: A Buy Opportunity with Clear Catalysts

Shift4 Payments' post-M&A trajectory is underpinned by a combination of disciplined capital allocation, margin resilience, and strategic expansion. With a stock price that appears undervalued relative to its growth prospects and analyst price targets, the company offers a compelling entry point for investors seeking exposure to the evolving payments sector. As the market re-rates its valuation to reflect its enhanced capabilities, Shift4 is well-positioned to deliver outsized returns over the next 12–24 months.

Comentarios

Aún no hay comentarios