Shareholder Value Erosion and Fiduciary Failures in Dayforce's $12.3B Thoma Bravo Takeover?

The $12.3 billion acquisition of DayforceDAY--, Inc. (NYSE: DAY) by Thoma Bravo at $70 per share has sparked a firestorm of legal and governance scrutiny. While the board of directors has declared the deal “in the best interests of stockholders,” multiple investigations by law firms—including Halper Sadeh LLC, The Ademi Firm, and Kaskela Law LLC—are probing whether the process violated fiduciary duties and federal securities laws. These inquiries center on three critical questions: Did the board secure the best possible price? Was the auction process robust enough to attract competing bids? And did shareholders receive full disclosure of material risks?

Corporate Governance and the “Fairness” of the Sale

Dayforce's board, led by CEO David Ossip and a slate of independent directors, claims to have conducted a “thorough review” of the Thoma Bravo offer. The board's rationale, outlined in SEC filings, emphasizes the 32% premium over the unaffected share price and the strategic benefits of going private, such as long-term growth flexibility[3]. However, the absence of a robust auction process raises red flags. According to a report by Business Wire, the merger agreement includes “significant penalties” if Dayforce pursues alternative bids, effectively neutering shareholder opportunities to negotiate a higher price[1]. This structure, critics argue, undermines the board's duty to maximize value.

The board's governance framework—complete with audit, compensation, and acquisition committees—appears sound on paper. Yet, as noted in Dayforce's corporate governance documents, the same directors who approved the deal also sit on committees tasked with overseeing mergers and executive compensation[1]. This overlap, while not uncommon, invites questions about potential conflicts of interest, particularly when the board's own “independent” directors have not publicly challenged the $70/share valuation.

Financial Rationale vs. Market Realities

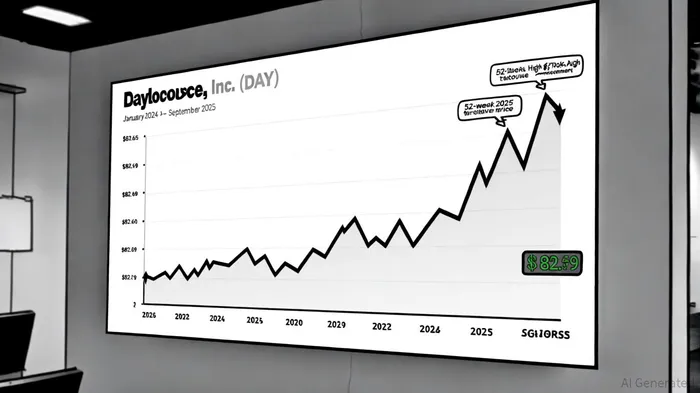

Proponents of the deal highlight Dayforce's strong recurring revenue model and 40%+ bookings growth in recent quarters[4]. However, the $70/share offer represents a 15.5% discount to the company's 52-week high of $82.69[2]. Analysts at Sahm Capital note that Dayforce's fair value estimate stood at $70.17 per share prior to the announcement, suggesting the offer is “marginally undervalued” given its cloud-based HCM market position[4]. Meanwhile, the company's 2024 net income plummeted 67% to $18.1 million, raising concerns about its ability to sustain growth amid intensifying competition[4].

Thoma Bravo's financial rationale hinges on private equity valuations, with the Abu Dhabi Investment Authority (ADIA) injecting capital as a minority investor[3]. Yet, as Axios observes, this transaction reflects a broader trend of private equity firms “snapping up software assets” during a labor market downturn, often prioritizing short-term gains over long-term innovation[3]. For Dayforce shareholders, this dynamic risks locking in value at a suboptimal price.

Fiduciary Breaches and Shareholder Recourse

The crux of the legal investigations lies in whether Dayforce's board fulfilled its fiduciary duties of care and loyalty. Halper Sadeh LLC's probe, for instance, alleges the board failed to “obtain the best possible consideration” and “disclose all material information” about the merger[1]. Similarly, Kaskela Law LLC argues that the $70/share offer “undervalues DAY shares” given prior analyst price targets above $80[5]. These claims gain traction when considering the merger's restrictive terms, which limit Dayforce's ability to solicit competing offers—a move that could deter shareholders from challenging the deal.

The SEC's preliminary proxy statement for the merger reveals that the board's approval was based on a “fairness opinion” from financial advisors, though details about due diligence processes remain opaque[3]. Shareholders now face a dilemma: Approve the deal and risk undervaluing their stake, or push for greater transparency and potentially delay the transaction.

Conclusion: A Governance Lesson in Private Equity Takeovers

Dayforce's sale underscores the tension between private equity strategies and shareholder value preservation. While the board has framed the deal as a win for long-term growth, the lack of competitive bidding and the price discount to recent highs suggest a governance lapse. As Halper Sadeh LLC and other firms continue their probes, the case serves as a cautionary tale about the importance of rigorous auction processes and full disclosure in high-stakes mergers. For investors, the takeaway is clear: Corporate governance is not just about structure—it's about ensuring that directors act with the same rigor and transparency as they would in their own financial interests.

Comentarios

Aún no hay comentarios