Is Sensata Technologies Holding plc (NYSE:ST) Potentially Undervalued in a High-Growth Industrial Automation Landscape?

In the rapidly evolving industrial automation sector, where digital transformation and AI-driven efficiency are reshaping manufacturing, Sensata Technologies Holding plcST-- (NYSE: ST) emerges as a compelling value investment. Despite operating in a high-growth landscape, the company's valuation metrics suggest it is trading at a material discount to sector averages, raising questions about whether the market is underappreciating its operational strengths and strategic positioning.

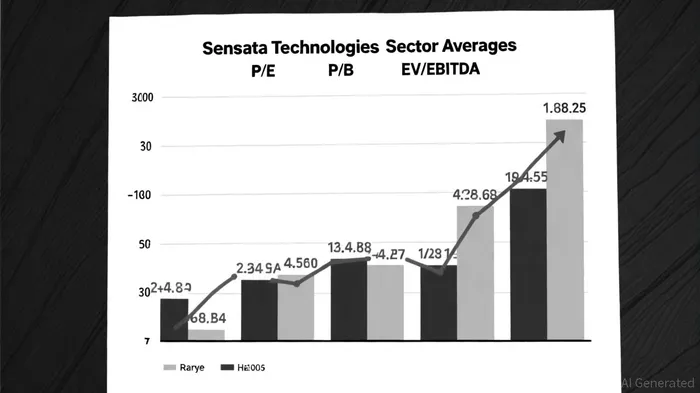

Valuation Metrics: A Stark Disconnect from Peers

Sensata's price-to-earnings (P/E) ratio of 9.74 as of September 19, 2025, stands in sharp contrast to the industrial automation sector's average P/E of 25.56[1]. This 62% discount implies that investors are pricing in significantly lower growth expectations for SensataST-- compared to its peers, despite the company's robust free cash flow generation and stable balance sheet. Similarly, Sensata's price-to-book (P/B) ratio of 1.21–1.61[2] lags far behind the industrials sector's P/B of 6.35[3], while its EV/EBITDA multiple of 9.31–9.7[4] is nearly 40% below the sector's 16.70 average. These metrics collectively suggest a potential undervaluation, particularly for a firm with a 91% free cash flow conversion rate and a net leverage ratio of 3.0x[5].

Sector Tailwinds: Automation's Accelerating Growth Trajectory

The industrial automation sector is poised for sustained expansion, driven by AI, IoT, and electrification. Market forecasts project the industry to grow at a 10.8% CAGR, reaching $378.57 billion by 2030[6], fueled by demand for predictive maintenance, smart factories, and energy-efficient systems. Sensata's core competencies in sensor and control technologies align directly with these trends. For instance, its recent launch of the High Efficiency Contactor (HEC)—enabling 400V/800V EV charging compatibility—positions it to capitalize on the electrification boom[7].

Moreover, macroeconomic factors are favorable. Lower interest rates, persistent labor shortages, and the proliferation of AI-powered automation tools (e.g., digital twins, computer vision) are accelerating adoption across non-automotive industries, which now account for 56% of automation orders[8]. Sensata's 68% revenue contribution from outside North America[9] further insulates it from regional economic volatility, enhancing its appeal in a globalized market.

Financial Resilience Amid Revenue Challenges

While Sensata reported an 8.9% year-over-year revenue decline in Q2 2025[10], this was primarily due to strategic divestitures and product lifecycle management, not operational underperformance. The company maintained an impressive 19% adjusted operating margin[11] and generated $115.5 million in free cash flow during the quarter[12]. Its Sensing Solutions segment even achieved 8.6% revenue growth, underscoring underlying demand for its mission-critical components.

Critics may point to a 28% drop in R&D spending in Q2 2025[13], but this appears to be a temporary reallocation rather than a long-term cut. Management has emphasized “operational excellence” as a priority, focusing on margin expansion and capital efficiency[14]. With a healthy balance sheet and a history of disciplined capital deployment, Sensata is well-positioned to reinvest in innovation as growth opportunities emerge.

Strategic Positioning: A Quiet Leader in Electrification

Sensata's leadership in electrification further strengthens its case as a value play. The company's partnerships with global OEMs and its 40-year legacy in industrial sensing solutions[15] provide a durable competitive moat. Its focus on electrification spans e-mobility, renewable energy, and industrial systems, aligning with multi-decade secular trends. CEO Stephan von Schuckmann's emphasis on “returning to growth” through operational excellence and electrification[16] signals a clear strategic vision, even as the company targets flat 2025 revenue.

Risks and Considerations

Investors should remain cautious about short-term revenue pressures and the R&D spending decline. Additionally, Sensata's valuation discount may reflect legitimate concerns about its growth trajectory compared to peers. However, in a sector where 60% of companies have already adopted automation[17], Sensata's operational efficiency and sector-leading margins suggest its current valuation may not fully capture its long-term potential.

Conclusion: A Value Opportunity in a High-Growth Sector

Sensata Technologies appears to be a classic value investing opportunity: a company trading at a significant discount to sector averages while generating strong cash flow and aligning with transformative industry trends. Its undervaluation may stem from short-term revenue challenges and market skepticism about growth, but the confluence of favorable sector dynamics, operational discipline, and strategic innovation in electrification positions it for outperformance. For investors seeking exposure to industrial automation without paying premium valuations, Sensata offers an attractive entry point ahead of broader market recognition.

Comentarios

Aún no hay comentarios