ON Semiconductor's Recent Underperformance Amid a Rising Market: A Case for Mispriced Value in a Cyclical Recovery

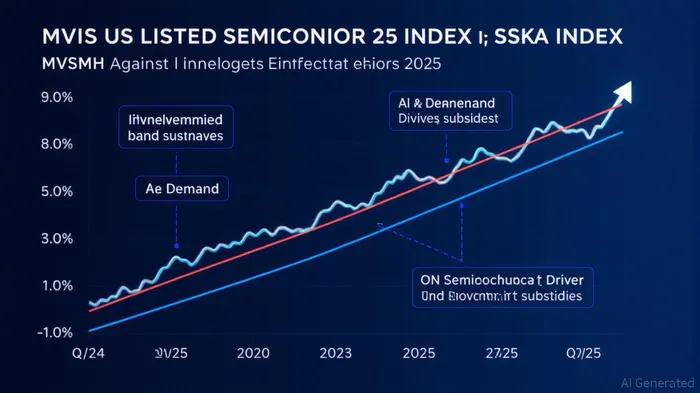

The semiconductor sector has entered a robust growth phase in 2025, driven by insatiable demand for AI and high-performance computing (HPC) chips. According to a report by the Semiconductor Industry Association (SIA), global semiconductor sales surged 23.2% year-over-year in Q3 2024, reaching a record $166.0 billion[2]. This momentum carried into Q3 2025, with Applied MaterialsAMAT-- reporting a 17% year-over-year increase in non-GAAP earnings per share and $7.3 billion in revenue[2]. The MVIS® US Listed Semiconductor 25 Index (MVSMH), which tracks the 25 largest U.S.-listed semiconductor firms, delivered a 20.80% year-to-date return as of Q3 2025[1], underscoring the sector's resilience amid macroeconomic volatility.

Yet, within this thriving landscape, ON Semiconductor—a key player in power and analog solutions—has lagged. While the sector thrives on AI-driven demand and advanced process nodes, ON Semiconductor's stock has failed to mirror these gains. This underperformance raises a critical question: Is the market mispricing ON Semiconductor's long-term potential in a cyclical recovery?

Sector Drivers: AI, HPC, and Geopolitical Tailwinds

The semiconductor industry's 2025 growth is anchored by three pillars:

1. AI and HPC Demand: Data-center chip sales skyrocketed from $64.8 billion in 2023 to $112 billion in 2024[2], with NVIDIA's H100 GPUs and AMD's MI300 family leading the charge. NVIDIA's revenue nearly doubled in 2024 to $46 billion[2], reflecting the sector's ability to capitalize on AI workloads.

2. Advanced Process Nodes: TSMC's 2nm (N2) and Intel's 18A nodes are entering high-volume manufacturing by late 2025[2], enabling next-generation chips for AI and consumer electronics.

3. Government Subsidies: The U.S. CHIPS Act ($52 billion) and EU Chips Act (€43 billion) are accelerating supply chain diversification and R&D investments[2], creating a favorable policy environment.

ON Semiconductor's Strategic Position and Valuation Disconnect

ON Semiconductor, despite its expertise in automotive and industrial semiconductors, has not yet aligned with the sector's AI/HPC-driven narrative. Its business model remains heavily reliant on analog and power solutions, which, while essential, face slower growth compared to discrete GPUs and logic chips. This strategic divergence may explain its muted performance relative to the MVSMH index.

However, the absence of recent financial data for ON SemiconductorON-- (as of Q3 2025) complicates a direct valuation assessment. If the company's fundamentals—such as revenue growth, margin expansion, or R&D allocation—remain stable or improve, its current stock price could represent a mispriced opportunity. For instance, if ON Semiconductor is underinvested in AI-related R&D or faces temporary supply chain bottlenecks, the market may be discounting its potential to adapt to sector trends.

Cyclical Recovery and Investor Implications

Semiconductors are inherently cyclical, with valuations often overshooting during upturns and correcting during downturns. The current bull market, fueled by AI and HPC, has created a “two-speed” recovery: companies directly enabling AI (e.g., NVIDIANVDA--, AMD) have surged, while those with indirect exposure (e.g., ON Semiconductor) have stagnated. This divergence suggests a potential re-rating if ON Semiconductor can pivot toward AI-driven markets or demonstrate operational resilience.

Investors should monitor two key metrics:

1. R&D Allocation: Has ON Semiconductor increased investments in AI/edge computing solutions?

2. Customer Diversification: Is the company expanding into high-growth segments like AI infrastructure or automotive HPC?

Conclusion: A Case for Selective Optimism

While the semiconductor sector's 2025 trajectory is firmly upward, ON Semiconductor's underperformance highlights a valuation gap. If the company can leverage its analog and power expertise to support AI and HPC ecosystems—whether through product innovation or strategic partnerships—its stock could experience a re-rating. For now, the lack of Q3 2025 financial data limits a granular analysis, but the broader sector trends suggest that cyclical recovery could eventually correct mispriced value.

Comentarios

Aún no hay comentarios