Sellas Life Sciences' Share Offering and Its Implications for Investors: Evaluating Dilution Risk Versus Growth Potential in Biotech Equity Investments

In the high-stakes world of biotech equity investing, the tension between growth potential and dilution risk often defines a company's trajectory. SELLAS Life SciencesSLS-- Group, Inc. (SLS) has recently navigated this tightrope with a $23.6 million warrant exercise in September 2025, raising critical questions for shareholders. While the offering bolsters the company's cash reserves to advance its late-stage pipeline, the accompanying share dilution-amid a rapidly expanding share count-demands careful scrutiny.

A Strategic Raise, But at What Cost?

The September 2025 transaction involved the exercise of warrants by a current institutional investor, generating gross proceeds of $23.6 million, according to the company's announcement. In exchange, the investor received new unregistered warrants to purchase 19,685,040 shares at $1.88 per share, exercisable immediately and expiring in five years, the company said. This structure-common in biotech fundraising-provides SELLASSLS-- with immediate liquidity while deferring full dilution until the new warrants are exercised. However, the sheer scale of the offering must be contextualized within the company's already ballooning share count.

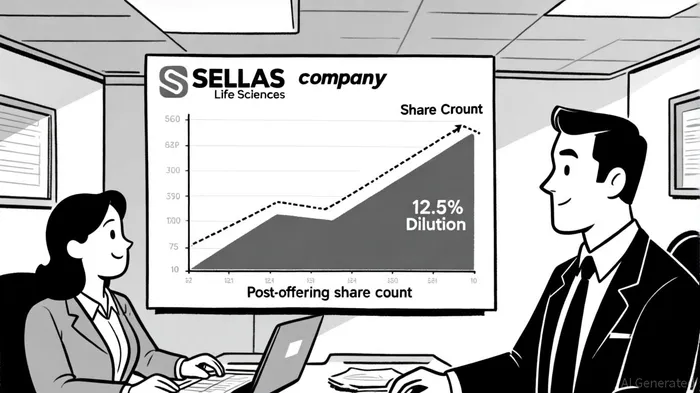

As of March 2025, SELLAS had 88 million shares outstanding, which surged to 99 million by June 2025-a 12.5% increase, according to historical shares-outstanding data. This expansion was driven by a Q1 2025 registered direct offering and an 800,000-share expansion of the Employee Stock Purchase Plan (ESPP), which contributed additional dilution, the company disclosed. The September 2025 warrant exercise, if fully exercised, would add another 19.6 million shares, pushing the total shares outstanding to approximately 118.6 million-a 34.8% increase from March 2025 levels. For investors, this raises concerns about whether the company's growth justifies such aggressive equity issuance.

Pipeline Progress: A Justification for the Raise?

The answer lies in SELLAS' clinical pipeline. Its lead asset, SLS009 (tambociclib), has shown notable promise in relapsed/refractory AML. SELLAS' second-quarter 2025 financial results and corporate update reported a median overall survival (mOS) of 8.9 months in AML-MRC patients and 8.8 months overall-figures that compare favorably to historical benchmarks of 4–6 months. The company also noted a 67% overall response rate (ORR) in AML-MRC patients and said the FDA recommended initiating a first-line AML trial in Q1 2026.

Meanwhile, the Phase 3 REGAL trial for GPS (galinpepimut-S) in AML received a positive interim analysis from the Independent Data Monitoring Committee (IDMC), with final results expected by year-end 2025, the company reported. If successful, GPS could become a cornerstone of AML treatment, offering SELLAS a clearer path to commercialization.

Financially, the company appears better positioned to fund these ambitions. As of June 30, 2025, SELLAS held $25.3 million in cash and equivalents, and the September 2025 warrant exercise added another $23.6 million to the balance sheet, according to the company's disclosures. These funds are earmarked for clinical development, including the aforementioned trials, and general operations. While the company has not publicly detailed its cash burn rate in the same update, the recent fundraising suggests management believes available capital-augmented by the warrant proceeds-can support near-term development plans.

Dilution Risk: A Double-Edged Sword

The key question for investors is whether the dilution is justified by the pipeline's potential. SELLAS' share count has grown by over 34% in six months, a pace that could erode shareholder value if the company fails to deliver on its clinical milestones. However, the biotech sector's inherent risk-reward dynamic often necessitates such trade-offs. For SELLAS, the $1.88 exercise price of the new warrants-set against a stock price near $1.69 at the time of the announcement-suggests the investor viewed the offering as accretive with some downside protection.

Critically, the dilution is not uniform. The ESPP expansion and the Q1 registered direct offering already diluted existing shareholders, while the new warrants represent a deferred obligation. If the stock price rises above $1.88, the full dilution impact will materialize; if it falls below that level, the warrants may expire unexercised. This dynamic creates a probabilistic risk that investors must weigh against the company's clinical progress.

Conclusion: Balancing Optimism and Caution

SELLAS Life Sciences' recent fundraising efforts highlight the delicate balance biotech firms must strike between securing capital and preserving shareholder value. The company's pipeline-particularly SLS009's encouraging Phase 2 data-provides a compelling rationale for the raise. However, the rapid share count growth and potential for further dilution require investors to adopt a measured approach.

For those willing to tolerate the risk, SELLAS offers a high-reward opportunity in a sector where breakthroughs can redefine market dynamics. Yet, the path forward hinges on the success of its late-stage trials and disciplined capital allocation. As the REGAL trial's final analysis approaches and the first-line AML trial for SLS009 begins, the coming months will be pivotal in determining whether the dilution is a necessary evil or a misstep.

Comentarios

Aún no hay comentarios