Seer, Inc. (NASDAQ:SEER): Institutional Ownership Dynamics and the Road to Growth

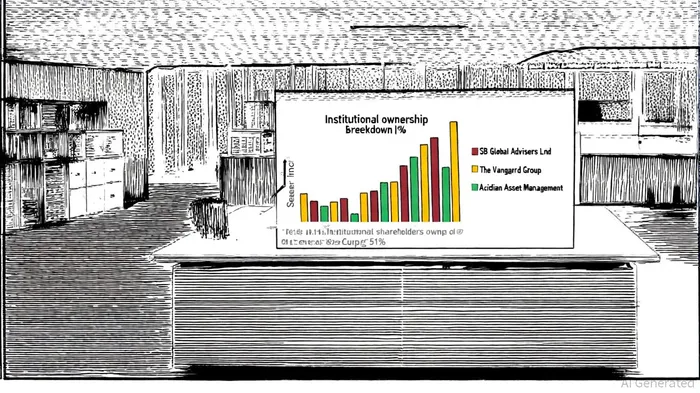

The institutional ownership landscape of SeerSEER--, Inc. (NASDAQ:SEER) offers a compelling lens through which to assess the company's growth potential and market confidence. As of Q2 2025, institutional investors collectively hold 41% of the company, with the top 12 shareholders accounting for 51% of the outstanding shares [1]. This concentration suggests a mix of strategic commitments and cautious reallocations, reflecting both optimism and skepticism about Seer's trajectory.

Institutional Ownership: A Tale of Two Trends

While some institutions have deepened their stakes in SEER, others have scaled back. Bridgeway Capital Management LLC increased its position by 15.5%, Geode Capital Management LLC by 16.5%, and Jacobs Levy Equity Management Inc. by a striking 124.5% [2]. These moves signal confidence in Seer's long-term value proposition, particularly its leadership in proteomics and its recent product innovations. Conversely, Invesco Ltd.IVZ-- reduced its holdings by 30.7%, JPMorgan ChaseJPM-- & Co. by 8.1%, and Two Sigma Investments LP by 2.7% [2]. Such divergent actions highlight the nuanced calculus of institutional investors, balancing Seer's technological promise against its financial performance and valuation concerns.

SB Global Advisers Ltd. remains the largest institutional holder, with a 9.17% stake valued at $11.298 million [3]. This position, alongside The Vanguard Group's 3.93% and Acadian AssetAAMI-- Management's 3.84%, underscores the presence of seasoned investors who likely view Seer as a high-conviction bet in the biotech sector. However, the absence of major new entrants in the top institutional ranks raises questions about broader market adoption.

Financial Performance: Progress Amid Challenges

Seer's financials tell a story of resilience and reinvention. For the full year 2024, the company reported $14.2 million in revenue, a 15% decline from 2023, driven by reduced product sales and the absence of grant revenue [4]. Despite this, the company maintained a 50% gross margin and ended the year with $300 million in cash, cash equivalents, and investments [4]. These metrics suggest a strong balance sheet, even as top-line growth has lagged.

The Q2 2025 results, however, offer a more optimistic outlook. Revenue surged 32% year-over-year, fueled by the launch of the Proteograph® ONE assay and SP200 automation instrument [5]. This growth aligns with Seer's full-year 2025 revenue guidance of $17–$18 million, representing a 24% increase at the midpoint over 2024 [5]. Analysts, however, have tempered expectations, slashing 2024 revenue forecasts to $14 million and lowering price targets, citing valuation concerns [6].

Industry Tailwinds and Strategic Positioning

Seer operates in a sector poised for explosive growth. The global proteomics market, valued at $27.8 billion in 2024, is projected to reach $58.16 billion by 2030, driven by advancements in precision medicine, AI-driven platforms, and high-throughput technologies [7]. Seer's recent 2,440% revenue growth—attributed to its Proteograph Product Suite—positions it as a key player in this transformation [8]. Collaborations with Thermo Fisher ScientificTMO-- and expansion into Europe further amplify its potential to capture market share [8].

The company's focus on scalable, cost-effective proteomic solutions also aligns with industry trends. For instance, the development of a proteomic aging clock using plasma proteins highlights the expanding applications of Seer's technology in preventive medicine [7]. Such innovations could differentiate Seer in a competitive landscape increasingly dominated by AI and multi-omics integration.

Risks and Considerations

While Seer's institutional ownership and industry positioning are promising, risks persist. The recent analyst downgrades reflect concerns about the company's ability to sustain growth and justify its valuation. Additionally, the biotech sector's inherent volatility—exacerbated by regulatory hurdles and R&D uncertainties—could impact Seer's trajectory.

Conclusion: A Calculated Bet on the Future

Seer, Inc. presents a paradox: a company with cutting-edge technology and strong institutional backing, yet one that faces skepticism from analysts and financial volatility. The institutional ownership dynamics reveal a market split between those who see Seer as a transformative force in proteomics and those who question its ability to convert innovation into consistent revenue.

For investors, the key lies in balancing Seer's long-term potential with its near-term challenges. The company's cash reserves, strategic partnerships, and alignment with industry trends suggest a solid foundation for growth. However, the recent analyst caution and mixed institutional actions underscore the need for vigilance. As the proteomics market accelerates, Seer's ability to execute on its vision will determine whether it becomes a breakout success or a cautionary tale.

Comentarios

Aún no hay comentarios