Sector Rotation Amid Inflation: Assessing Tech and Consumer Discretionary Vulnerability in a Slowing Economy

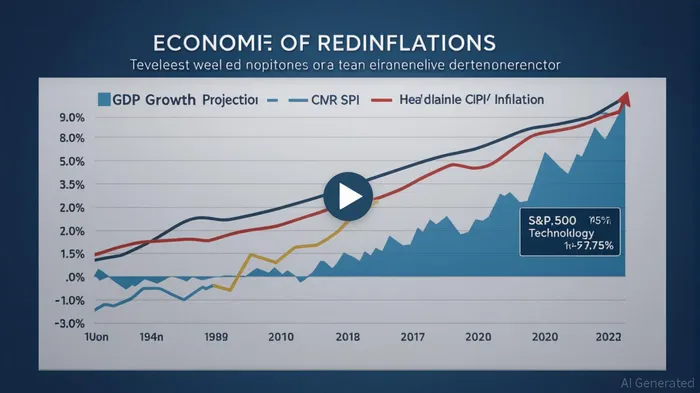

The U.S. economy stands at a crossroads in 2025, with growth projections of 1.3% in Q3 and an annual average of 1.7% for the year, tempered by inflationary pressures that remain stubbornly above the Federal Reserve’s 2% target [1]. This macroeconomic backdrop has intensified scrutiny of sector rotation strategies, particularly for Technology and Consumer Discretionary stocks, which face divergent risks and opportunities.

Technology: AI-Driven Resilience Amid Volatility

The Technology sector has defied conventional wisdom, with the S&P 500 reaching record highs despite a core CPI of 3.1% and slowing GDP growth [1]. Artificial intelligence (AI) has emerged as a linchpin of earnings growth, with investment flows surpassing 2024 levels and driving tangible revenue gains [2]. By mid-2025, blended 1-year forward EPS for the sector showed robust growth, even as price volatility persisted [1]. This resilience stems from AI’s ability to offset labor and operational costs—a critical advantage in an inflationary environment. However, the sector’s reliance on long-term secular trends leaves it exposed to short-term interest rate fluctuations and valuation corrections if AI adoption slows.

Consumer Discretionary: Tariff-Induced Margin Compression

The Consumer Discretionary sector, in contrast, faces acute near-term challenges. Tariff hikes and inflation have eroded operating margins by 1.5%, with automakers, apparel firms, and homebuilders bearing the brunt [4]. Tesla’s 16% operating margin miss in Q2 2025, driven by $300 million in tariff-related costs, exemplifies the sector’s fragility [4]. Similarly, General MotorsGM-- and FordF-- reported billion-dollar hits to EBIT adjusted margins, underscoring the vulnerability of import-dependent businesses [4]. While large retailers like WalmartWMT-- and AmazonAMZN-- have leveraged supply chain efficiencies to maintain margins (Amazon’s North America operating margin reached 5.98% [3]), smaller players struggle to absorb cost shocks.

Strategic Implications for Investors

The divergent trajectories of these sectors highlight the importance of strategic positioning. Technology’s AI-driven growth offers a hedge against inflation but requires patience through cyclical volatility. Conversely, Consumer Discretionary’s margin pressures suggest caution, particularly for small-cap names. However, the sector’s long-term recovery potential—projected to materialize in 2026 as tariffs ease—could create attractive entry points for selective investors [4].

For now, the Federal Reserve’s anticipated rate cuts and modest 2.1% inflation-adjusted income growth in Q2 2025 provide a floor for consumer spending [3]. Yet, the specter of stagflation and policy uncertainty demands a disciplined approach to sector rotation. Investors should prioritize Technology’s innovation-driven narratives while hedging against Consumer Discretionary’s near-term headwinds through diversified exposure to communication services and financials [4].

Source:

[1] Third Quarter 2025 Survey of Professional Forecasters [https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/spf-q3-2025]

[2] Slower Growth, Higher Inflation And S&P 500 All-time Highs [https://www.jpmorganJPM--.com/insights/markets/top-market-takeaways/tmt-slower-growth-higher-inflation-and-s-and-p-five-hundred-all-time-highs]

[3] Assessing the Resilience of Retail and Tech Stocks Amid ... [https://www.ainvest.com/news/personal-income-growth-implications-consumer-driven-sectors-assessing-resilience-retail-tech-stocks-inflationary-pressures-2508/]

[4] Consumer Discretionary Sector Outlook: Tariffs and ... [https://www.lpl.com/research/blog/consumer-discretionary-sector-outlook.html]

Comentarios

Aún no hay comentarios