Scinai Immunotherapeutics' ADS Offering and Strategic Implications: Evaluating Capital-Raising Efficiency and Growth Catalysts in the Biotech Sector

Scinai Immunotherapeutics Ltd. has emerged as a compelling case study in biotech capital-raising efficiency, leveraging a Standby Equity Purchase Agreement (SEPA) to secure $7.18 million in gross proceeds as of September 2025. This structured financing mechanism, which allows the company to sell up to $10 million in American Depositary Shares (ADSs) over 36 months, reflects a strategic alignment with industry trends favoring non-dilutive, on-demand capital solutions[1]. By avoiding warrants or additional dilution, ScinaiSCNI-- has preserved shareholder value while funding critical growth initiatives, including its nanobody therapeutics pipeline and CDMO business expansion[2].

Capital-Raising Efficiency: A Benchmark Analysis

The biotech sector's capital landscape in 2024–2025 has been marked by polarization, with investors prioritizing late-stage assets and scientifically validated pipelines[3]. Scinai's SEPA terms—executed at a 3% discount to market price ($3.03 per ADS)—align with industry benchmarks for structured financings, which emphasize flexibility and cost predictability[4]. According to a report by EY, biotech firms are increasingly adopting such mechanisms to navigate macroeconomic uncertainties, including high interest rates and inflation[5]. Scinai's ability to raise $1.38 million in a single drawdown underscores its operational credibility and the market's confidence in its dual-revenue model[6].

Comparatively, industry data reveals that mega-rounds (>$100 million) in 2024 were concentrated among firms with proven clinical milestones and experienced leadership[7]. While Scinai's funding scale is modest, its SEPA structure offers a less disruptive alternative to traditional equity offerings, which often trigger volatility. This approach mirrors broader sector shifts toward private placements and royalty deals, which are projected to grow at a 45% CAGR[8].

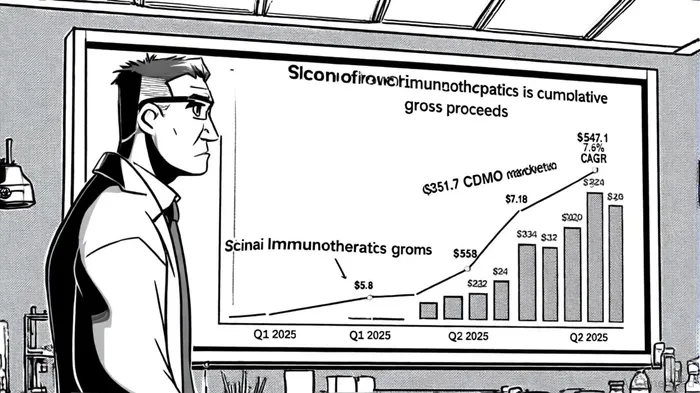

Growth Catalysts: CDMO Expansion and Nanobody Innovation

Scinai's CDMO segment, a key driver of its 2025 revenue guidance ($2 million), is positioned to benefit from a broader industry rebound. The global healthcare CDMO market, valued at $351.7 billion in 2024, is forecasted to reach $547.1 billion by 2030, driven by demand for biologics, ADCs, and small-molecule outsourcing[9]. Scinai's focus on U.S.-based manufacturing and specialized technologies aligns with this trend, as pharmaceutical firms prioritize supply chain diversification[10]. Analysts note that CDMOs with mature client pipelines and operational scalability—such as Scinai's projected breakeven by 2026—are better positioned to capitalize on this growth[11].

Meanwhile, Scinai's nanobody pipeline represents a high-impact innovation lever. Nanobodies, derived from camelid antibodies, offer advantages in stability, specificity, and intracellular targeting, making them attractive for oncology and neurology applications[12]. The sector's shift toward later-stage dealmaking—evidenced by a 2024 biopharma partnering value peak of $191 billion—highlights the strategic value of platforms with clear translational potential[13]. Scinai's IND-enabling studies, supported by SEPA proceeds, could position it to secure partnerships or licensing deals, mirroring successes in AI-driven drug discovery and cell therapy platforms[14].

Strategic Implications and Risks

While Scinai's capital structure and growth vectors are robust, challenges persist. The CDMO sector faces bottlenecks in CGT manufacturing scalability, and early-stage biotechs remain underfunded amid macroeconomic headwinds[15]. Additionally, the company's reliance on a single SEPA investor (Yorkville Advisors) introduces concentration risk, though its $2.8 million remaining capacity provides flexibility[1].

Investors must also weigh the biotech sector's valuation dynamics. Cell and gene therapy firms trade at premium multiples, whereas diagnostics and tools offer more stable returns[16]. Scinai's dual focus on therapeutics and CDMO services offers a balanced risk profile, but its path to profitability hinges on successful IND filings and CDMO margin expansion.

Conclusion

Scinai Immunotherapeutics' ADS offering exemplifies efficient capital-raising in a fragmented biotech landscape, combining non-dilutive financing with strategic growth levers. Its CDMO business, poised to benefit from a $547.1 billion market by 2030, and its nanobody pipeline, aligned with high-value therapeutic trends, position the company to navigate sector volatility. However, execution risks—particularly in clinical translation and manufacturing scalability—demand close monitoring. For investors, Scinai represents a niche opportunity in a sector increasingly defined by innovation and operational discipline.

Comentarios

Aún no hay comentarios