Is Your Savings Account Still a Smart Place for Your Cash?

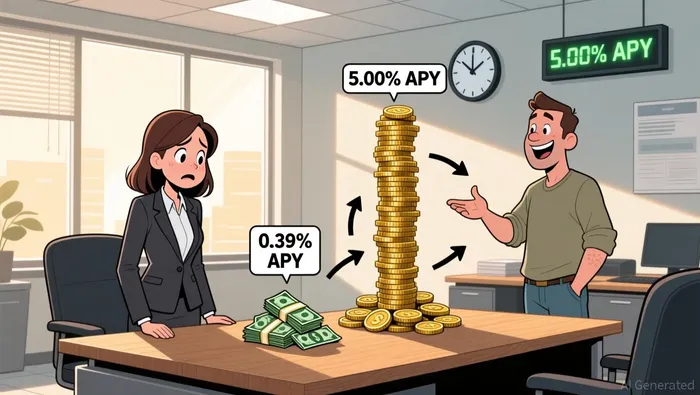

The math here is straightforward, and it's not in your favor. Most people are leaving money on the table simply by keeping it in a standard savings account. The national average pays a mere 0.39% APY. That's the baseline, the floor. Meanwhile, the smartest savers are locking in rates that are more than ten times higher. The top high-yield savings accounts are offering up to 5.00% APY as of this week. That's a massive gap.

This isn't just about a better return; it's about a battle against inflation. When your cash earns 0.39% but prices are rising, you're effectively losing purchasing power every year. The difference between a 0.39% return and a 5.00% return is the difference between watching your savings shrink and watching them grow. It's like leaving your money in a low-interest drawer while the cost of groceries climbs.

The good news is that the top rates are still available. The bad news is that this window is closing. The Federal Reserve has been cutting its benchmark rate, lowering it three times in 2025. That trend is expected to continue into 2026, which will pressure all deposit yields lower. Analysts predict top yields will continue the downward slide next year. The forecast is for the highest national savings rates to fall to around 3.70% by the end of 2026.

The bottom line is that you need to act now. The simple math is clear: your cash is losing ground. To keep pace, you need to shop around and move your money into a high-yield account. The alternative is to quietly accept that your savings are being eroded.

The Business Behind the Best Rates: Why Online Banks Pay More

The simple business logic here is about costs and choices. Think of a high-yield savings account as your personal rainy day fund that actually earns interest, unlike a regular savings account that barely keeps pace with inflation. The best places for that cash are online banks and credit unions, and the reason is straightforward: they have lower operating costs.

Traditional banks with physical branches have a big overhead. They need to pay for buildings, tellers, and all the staff to run those locations. That's money they have to cover, and they often do it by offering lower rates on the deposits they take in. Online banks and credit unions, by contrast, operate with a much leaner model. They have no physical branches to maintain, which slashes their expenses. That's the key. They can pass those savings directly to you in the form of higher interest rates.

It's like comparing a local diner to a national chain. The diner has to pay for a prime downtown location and a full staff, so its prices are higher. The chain, with its streamlined kitchens and drive-thrus, can offer a similar meal for less. In banking, the online model is the chain. They use that cost advantage to pay you more for your money. That's why the top rates, like the 5.00% APY offered by Varo Money, are almost always found at these digital-first institutions.

And here's the practical part: these accounts are just as safe and accessible as any other. They are backed by the same insurance as traditional banks-FDIC for banks and NCUA for credit unions-which protects your deposits up to $250,000. You can access your cash instantly, just like in a checking account, but with a much better return. This makes them a far smarter place for your emergency fund or short-term savings than a checking account, which typically pays little or no interest, or worse, under the mattress where it loses value to inflation.

The bottom line is that the best rates are a direct result of a simpler, cheaper business. By choosing an online bank or credit union, you're not just getting a higher number; you're aligning your money with a model that's built to reward savers.

What to Watch: The Next Moves for Your Cash

The immediate catalyst to watch is the Federal Reserve's next move. The central bank held its benchmark rate steady last month, pausing its recent cutting trend. The market sees low odds of another cut at the upcoming March meeting. Yet, the broader expectation is for one more reduction in 2026. This sets the stage for a gradual, but steady, decline in the rates banks pay on savings.

The key risk for savers is that this downward slide continues. Forecasts point to the top national savings APY falling to around 3.70% by the end of 2026. That's a drop of over a full percentage point from the peak yields seen in 2025. In other words, the window for locking in today's top rates is closing. The best deposit rates are still above inflation, but they are not expected to stay at these levels.

So, what should you do? The practical takeaway is to act now. The smartest savers are already moving their cash to capture the highest yield before it slips away. Start by comparing the top rates from online banks and credit unions. You'll find institutions like Varo Money offering up to 5.00% APY, a stark contrast to the national average. Crucially, ensure any account you choose is backed by FDIC insurance for banks or NCUA insurance for credit unions, protecting your deposits up to $250,000.

This isn't about chasing a fleeting peak. It's about securing a better return for your emergency fund or short-term savings while you still can. The business logic is clear: online banks pay more because they have lower costs, and that advantage is being passed to you. By moving your cash now, you're not just getting a higher number; you're protecting your purchasing power against the inevitable pressure of falling interest rates.

Comentarios

Aún no hay comentarios