Saratoga Investment's Q2 2025 Performance: A Test of Business Model Resilience Amid Mixed Results

In the second quarter of 2025, Saratoga Investment Corp.SAR-- (SAR) demonstrated a compelling mix of resilience and vulnerability in its business model, navigating a challenging economic landscape marked by rising interest rates and shifting credit conditions. While the company outperformed industry benchmarks in key metrics like Return on Equity (ROE), it also faced headwinds that caused its earnings to fall short of Wall Street expectations. This duality underscores the nuanced dynamics of business development companies (BDCs) in a post-pandemic market.

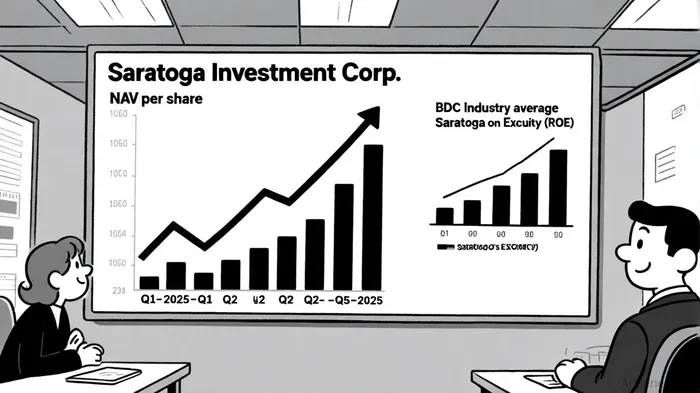

Key Metrics Highlight Resilience

Saratoga's Q2 results revealed a 3.6% increase in Net Asset Value (NAV) and a 0.4% rise in NAV per share year-over-year, reflecting disciplined portfolio management, according to a GlobeNewswire release. The company's quarterly ROE of 13.8%-with a trailing twelve-month (LTM) ROE of 9.1%-surpassed the BDC industry average of 7.3%, a testament to its ability to generate returns in a high-interest-rate environment. This outperformance was driven by strategic investments in middle-market companies and a focus on leveraged loans and mezzanine debt.

Adjusted net investment income (NII) surged by 38.3% year-over-year to $18.2 million, fueled by the full recovery of the Noland investment, management said on the earnings call. Meanwhile, total investment income of $43.0 million exceeded analyst estimates of $37.12 million, signaling robust revenue generation, according to GuruFocus. These figures suggest that Saratoga's business model remains well-positioned to capitalize on its core strengths, particularly its expertise in structuring complex debt instruments.

Mixed Results and Market Realities

Despite these positives, Saratoga's Q2 earnings of $0.84 per share fell below the $0.67 per share expected by analysts, while revenue of $30.626 million lagged behind the projected $32.4 million, per the GlobeNewswire release. This shortfall highlights the pressures BDCs face in maintaining consistent performance amid macroeconomic volatility. A 0.3% decline in assets under management (AUM) to $995.3 million further illustrates the challenges of scaling in a competitive market.

However, historical backtesting of SAR's past 22 earnings-miss events from 2022 to 2025 reveals that the stock has generated an average cumulative excess return of +2.5% over 30 trading days, with a win rate peaking at 86% by day 28, suggesting potential for post-miss mean reversion. While the earnings miss is a near-term concern, these historical patterns indicate that the market may exhibit corrective tendencies over time.

However, the company's liquidity position remains robust, with $385.5 million in available capital to deploy, management said on the earnings call. This flexibility allows SaratogaSAR-- to pursue accretive opportunities, such as the recent return of its Zollege investment to accrual status, which reduced non-accrual investments to just 0.2% of portfolio fair value. Such actions reinforce the company's commitment to risk mitigation and portfolio quality.

Dividend Stability and Investor Appeal

Saratoga's base dividend of $0.75 per share, with an annualized yield of 12.3% based on its $24.41 stock price, continues to attract income-focused investors, per the GlobeNewswire release. This high yield, combined with a strong balance sheet and strategic asset allocation, positions the company as a defensive play in a market where credit risk remains elevated.

Conclusion: Resilience with Caution

Saratoga's Q2 performance exemplifies the dual-edged nature of BDC operations in 2025. Its ability to generate strong ROE and maintain a high-yield dividend underscores the resilience of its business model, particularly in its focus on middle-market lending. Yet, the earnings miss and AUM contraction serve as reminders of the fragility inherent in a sector sensitive to interest rate cycles and credit cycles. For investors, the key takeaway is that Saratoga's strategic agility and liquidity buffer provide a solid foundation for navigating near-term uncertainties, though continued vigilance will be required to sustain long-term growth.

Comentarios

Aún no hay comentarios