Sally Beauty's Strategic Turnaround and Growth Potential: Post-Meeting Analyst Optimism and Re-Rating Potential

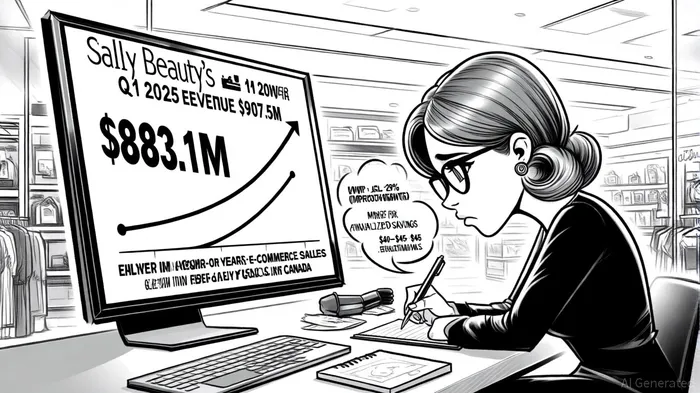

In the first quarter of 2025, Sally BeautySBH-- Holdings (SBH) delivered a mixed performance, with revenue falling short of expectations but non-GAAP earnings exceeding forecasts. This duality has sparked a nuanced debate among analysts, who are now weighing the company's strategic initiatives against macroeconomic headwinds. According to a Financial Content report, SBH's Q1 revenue of $883.1 million marked a 2.8% year-on-year decline, missing analyst estimates by $24.4 million. However, disciplined expense management and margin expansion—driven by a 1.3 percentage point increase in operating margin to 7.9%—underscored the company's operational resilience, according to the same report.

Notably, historical backtesting from 2022 to 2025 reveals that when SBHSBH-- beats earnings expectations, the stock has historically averaged a 7.11% gain on Day 4 post-announcement, with a 67% win rate, though the sample size is limited to three events.

Strategic Initiatives: Digital Expansion and Cost Discipline

SBH's management has prioritized digital transformation as a core pillar of its turnaround strategy. E-commerce sales for Sally U.S. and Canada surged 29% year-on-year, reflecting the success of digital marketplace enhancements and personalization efforts, as noted in the Financial Content report. CEO Denise Paulonis emphasized these gains during the Q1 earnings call, noting that digital initiatives are “critical to unlocking long-term value.” Complementing this, the company's “Happy Beauty” store refresh program has generated early positive feedback, with increased cross-shopping and customer engagement, according to the Q1 call coverage.

Cost control remains another focal point. The Fuel for Growth program, aimed at driving operational efficiency, is projected to deliver $40–$45 million in annualized savings by 2026, per the Financial Content report. These savings, coupled with a $70 million brand refresh initiative slated for H2 2025, position SBH to mitigate inflationary pressures and reinvest in growth, as discussed in the Q1 call coverage. Analysts have highlighted the “disciplined approach to margin preservation” as a key differentiator, despite near-term revenue challenges, in a Nasdaq article reviewing analyst views.

Analyst Sentiment: Divergence and Cautious Optimism

Post-earnings analyst sentiment remains polarized. While Morgan Stanley's Simeon Gutman maintained an Underweight rating with a $12.00 price target, TD Cowen's Oliver Chen upgraded to Buy with a $16.00 target, citing “strong digital momentum and margin resilience,” according to the Nasdaq article. As of June 2025, the average price target across five analysts stands at $13.80, a 17.45% increase from prior estimates, with a high of $16.00 and a low of $12.00. This divergence reflects broader uncertainties around consumer spending and sector-specific risks, such as the flu season's impact on BSG (Beauty Systems Group) performance, which was raised during the Q1 call coverage.

Notably, analysts have praised SBH's proactive stance on innovation. Susan Anderson of Canaccord Genuity, for instance, highlighted the company's “aggressive product portfolio refresh” as a catalyst for differentiation in a crowded market, another point covered in the Q1 call reporting. However, concerns persist about scaling growth, given SBH's market capitalization remains below industry averages, as the Nasdaq piece also notes.

Re-Rating Potential: Balancing Risks and Rewards

The path to re-rating hinges on SBH's ability to execute its strategic pillars. Digital expansion, in particular, offers a high-impact lever: e-commerce now accounts for a growing share of Sally U.S. and Canada's sales, with management targeting further acceleration through AI-driven personalization, per the Financial Content report. If successful, this could drive revenue growth and justify a premium valuation.

However, risks remain. A prolonged softness in transaction trends, as noted by Chen during the Q1 call, could delay margin recovery. Additionally, the brand refresh initiative, while promising, carries execution risks. Investors must also monitor the Fuel for Growth program's progress, as unmet savings targets could erode confidence.

Conclusion

Sally Beauty's strategic turnaround is a work in progress, marked by both tangible progress and lingering uncertainties. While the company's margin discipline and digital momentum have earned cautious optimism from analysts, the road to re-rating will require consistent execution. For investors, the key lies in balancing the potential of SBH's initiatives with macroeconomic and operational risks. As the market watches for H2 2025 updates, the $13.80 average price target suggests a moderate upside, but only if the company can translate its strategic vision into sustained performance.

Comentarios

Aún no hay comentarios