Sage Potash's Capital Restructuring: Balancing Debt Reduction and Long-Term Value Creation

Sage Potash Corp. (SAGE.V) has embarked on a strategic initiative to optimize its capital structure, leveraging debt-to-equity conversions and non-dilutive financing to position itself for long-term growth. Recent moves, including a "shares for debt" transaction and a $14 million grant from the U.S. Department of Agriculture, underscore the company's focus on reducing leverage while preserving equity value for shareholders. However, the implications of these actions-particularly the issuance of new shares to settle debt-require careful scrutiny in the context of the potash industry's capital-intensive nature and historical precedents.

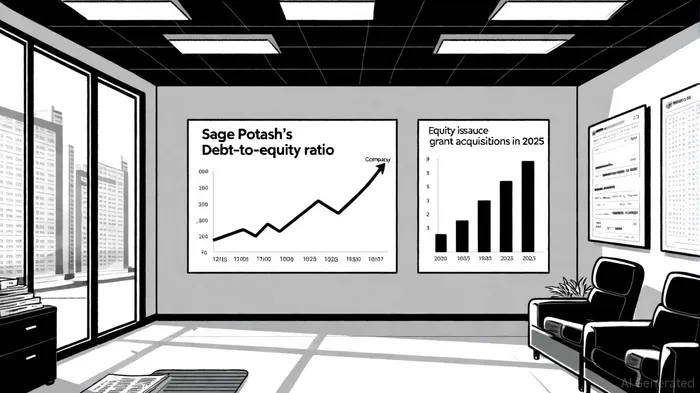

Strategic Debt Reduction: A Conservative Approach

Sage Potash's current debt-to-equity ratio of 0.0% indicates a purely equity-funded capital structure, a rarity in the potash sector, where companies often rely on debt to finance exploration and development, according to Macroaxis' debt-to-equity analysis. This conservative stance may reflect either a deliberate strategy to avoid debt or potential gaps in financial reporting. Nevertheless, the company's recent decision to issue 500,000 common shares at $0.27 per share to settle $135,000 in debt obligations signals a proactive approach to debt management, as disclosed in Sage Potash's meeting release. By converting liabilities into equity, Sage Potash aims to strengthen its balance sheet and free up capital for its core operations in Utah's Paradox Basin, according to MarketScreener's shareholder page.

This strategy aligns with broader industry trends. For example, Intrepid Potash (IPI) has historically reduced its debt-to-equity ratio from 0.09 in 2010 to 0.26 in 2025, demonstrating how sustained debt reduction can enhance financial stability in the sector, as shown in Macrotrends' debt-to-equity chart. However, such conversions are not without trade-offs. The issuance of new shares dilutes existing shareholders' ownership stakes, potentially signaling financial distress to the market, as explained in FasterCapital's debt-to-equity guide. Sage's recent transaction, while relatively small in scale, sets a precedent for future restructuring efforts that must balance debt reduction with shareholder value preservation.

The Role of Non-Dilutive Capital: A Strategic Advantage

Sage Potash's $14 million grant from the USDA represents a critical inflection point in its capital strategy, according to MarketScreener's news release. Unlike equity financing, grants provide non-dilutive capital that can fund infrastructure development and exploration without compromising ownership structure. This funding, directed toward its Sage Plains Potash Property, supports the company's long-term vision of district-scale potash production in a low-cost, solution-mining-friendly environment, per the company's investor page.

The ability to secure such grants highlights Sage's alignment with policy priorities, such as domestic mineral security and sustainable resource development. In contrast, companies reliant on debt or equity financing face higher costs and greater market volatility. For instance, a 2024 ScienceDirect study on market-based debt-to-equity conversions in China found that such strategies can enhance corporate green innovation by reallocating resources toward sustainable projects. While Sage's context differs, the principle of leveraging external funding to reduce reliance on debt resonates with its current approach.

Long-Term Value Implications: Risks and Opportunities

The potash industry's capital-intensive nature means that companies must navigate a delicate balance between growth investment and financial prudence. Debt-to-equity conversions, while effective in reducing leverage, can trigger market skepticism if perceived as a sign of distress. For example, a 2023 analysis noted that shareholder dilution often correlates with short-term stock price declines, as investors react to reduced ownership stakes, as discussed in Aaron Hall's analysis. Sage's recent issuance of 500,000 shares, though modest, could test market confidence if repeated on a larger scale.

Conversely, a well-executed capital restructuring can enhance long-term value. By eliminating debt servicing costs and improving financial flexibility, Sage Potash can redirect resources toward high-impact projects, such as advancing its Sage Plains deposit toward production. Historical case studies, including Intrepid Potash's debt reduction from $150 million in the mid-2010s to $2 million in 2024, illustrate how disciplined capital management can transform a company's trajectory, as shown in Macrotrends' long-term debt data.

Conclusion: A Prudent Path Forward

Sage Potash's capital structure optimization reflects a strategic emphasis on stability and scalability. While the company's debt-to-equity conversion efforts and grant acquisitions mitigate immediate financial risks, their long-term success will depend on Sage's ability to execute its exploration plans and maintain investor trust. For shareholders, the key will be monitoring how these actions influence operational milestones, such as resource upgrades and production timelines, while ensuring that dilution remains controlled.

In an industry where capital discipline separates survivors from casualties, Sage Potash's current trajectory suggests a commitment to building a resilient, equity-driven foundation-one that could position it as a key player in North America's potash landscape.

Comentarios

Aún no hay comentarios