Ryder's Strategic Position in the 3PL Industry and Growth Implications for Investors

The third-party logistics (3PL) industry is undergoing a transformative phase, driven by e-commerce acceleration, digital innovation, and nearshoring trends. For investors, companies like Ryder SystemR-- Inc. (R) stand out as strategic assets, combining market resilience with forward-looking initiatives. As of Q1 2025, Ryder holds a 5.91% share of the U.S. 3PL market, a marginal increase from 5.71% in Q4 2024, as reported by CSI Market. While this pales in comparison to industry giants like UPS (42.43%) and FedEx (41.04%), Ryder's niche expertise in fleet management, supply chain solutions, and sustainable logistics positions it as a high-growth contender, according to CSI Market.

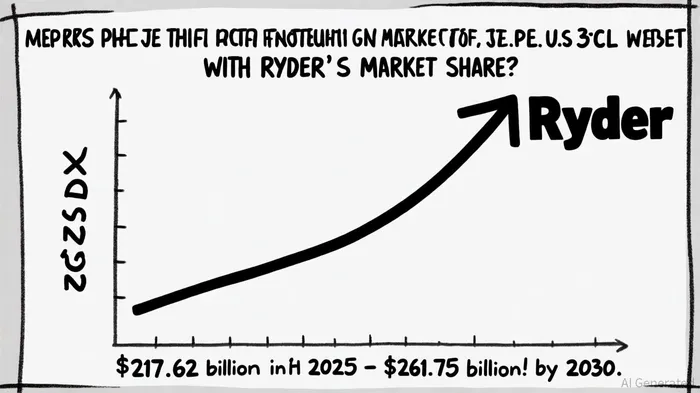

Market Share and Competitive Position

Ryder's dominance in the full-service truck leasing segment-where it commands 25% market share-underscores its operational depth. This strength is complemented by its recognition as a "Top 10 3PL" in the Inbound Logistics Readers' Choice, a testament to its customer-centric innovation. However, the company faces stiff competition from digital freight brokers and global logistics titans like C.H. Robinson, XPO Logistics, and DHL, according to a Porter Five Forces analysis. These rivals leverage advanced AI-driven platforms to undercut traditional players on pricing and scalability, as noted in a SWOT analysis.

Growth Drivers: E-Commerce and Sustainability

The U.S. 3PL market is projected to grow at a 3.76% CAGR, reaching $261.75 billion by 2030, per CSI Market. Ryder's strategic alignment with this trajectory is evident in its investments:

- Technology: The RyderShare™ platform, a digital marketplace for asset utilization, enhances fleet efficiency and customer integration, as highlighted in the SWOT analysis.

- Sustainability: Aggressive adoption of electric vehicles (EVs) and green logistics solutions aligns with regulatory and consumer demands, consistent with the SWOT analysis.

- Nearshoring: As supply chains shift toward North America, Ryder's U.S.-Mexico logistics infrastructure gains relevance, according to CSI Market.

Strategic Risks and Mitigation

Despite its strengths, Ryder must navigate challenges such as high R&D costs for technology adoption and margin pressures from digital competitors, as described in the SWOT analysis. However, its diversified revenue streams-spanning transportation, leasing, and supply chain solutions-provide a buffer against sector-specific downturns, per the SWOT analysis.

Investment Implications

For capital allocation, Ryder's 5.91% market share reported by CSI Market represents untapped potential. Its focus on innovation and sustainability could drive market share gains as the industry matures. Investors should monitor quarterly reports for SCS segment performance, which reflects demand for integrated logistics solutions, as noted in the SWOT analysis. Historically, a simple buy-and-hold strategy following earnings releases has shown a positive drift of approximately 2.6% over 6–7 trading days, with a 75% win rate, though the effect tends to fade after 10 days, according to a historical earnings event study (2022–2025). While UPS and FedEx dominate, Ryder's agility in niche markets and technological pivots may yield outsized returns for long-term holders.

In conclusion, Ryder's strategic positioning in the 3PL sector-bolstered by its technological edge and sustainability focus-makes it a compelling investment. As the industry evolves, its ability to adapt to digital and environmental trends could catalyze capital appreciation, particularly for investors seeking exposure to a resilient, innovation-driven player in a high-growth sector.

Comentarios

Aún no hay comentarios