ROOT Stock Loses 34% YTD, Trades at a Premium: Should You Buy the Dip?

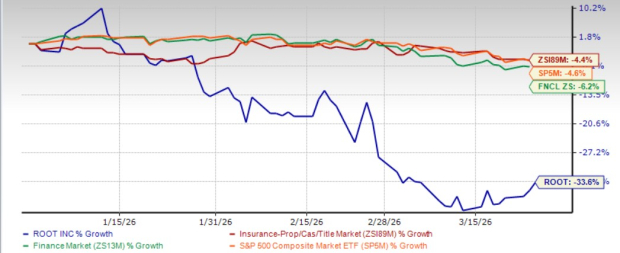

Shares of Root Inc. ROOT have lost 34.4% year to date, underperforming the industry, the sector and the Zacks S&P 500 composite.

ROOT, a provider of automobile and renters insurance products, envisions being the largest and most profitable personal lines insurance carrier in the United States. Improved underwriting via telematics, lower loss ratios, efficient customer acquisition, and scaling profitable policies through data-driven pricing and retention position ROOTROOT-- for long-term growth.

ROOT vs. Industry, Sector & S&P 500 YTD

Image Source: Zacks Investment Research

Shares of its peer Lemonade LMND have lost 4.2%, while those of another peer, EverQuote EVER, have lost 41.1% year to date.

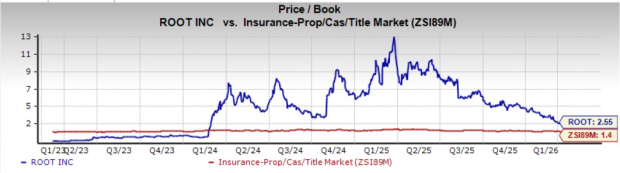

ROOT Shares Are Expensive

Root shares trade at a price-to-book value ratio of 2.55, above the industry average of 1.4.

Image Source: Zacks Investment Research

In fact, LemonadeLMND-- and EverQuoteEVER-- are also trading at a premium to the industry.

Average Target Price for ROOT Suggests Upside

Based on short-term price targets offered by five analysts, the Zacks average price target is $90 per share. The average suggests a 92.6% upside from the last closing price.

The Case for ROOT

Root is increasingly relying on advanced technology to strengthen its pricing strategy, placing artificial intelligence and machine learning at the center of underwriting improvements. These tools have enhanced risk assessment and pricing precision, driving notable growth, especially within the partnership channel, wherein new business volumes nearly tripled year over year. In the second quarter of 2025, the company rolled out a refined pricing model across several states, reinforcing its competitive edge.

Root continues to target the vast $350 billion auto insurance market, where it sees ample room for expansion. Its growth roadmap is built on three key pillars: expanding geographically, diversifying distribution channels, and deepening partnerships. By entering additional states and broadening customer access points, the company is steadily increasing its policies in force while leveraging automation and data-driven insights.

To strengthen its presence among independent agents, Root has integrated its products with major comparative rating platforms like EZLynx and PL Rating. At the same time, partnership channel growth is being propelled by expansion across automotive, financial services and agent-driven segments. Continued investment in customer acquisition is also supporting the growth of its direct business.

On the financial front, disciplined cost management and targeted marketing efforts are expected to further improve margins. The company has maintained a gross loss ratio below its long-term target of 60–65%, enabling selective price reductions without compromising profitability. Strong underwriting performance has driven significant margin expansion, culminating in its first profitable year in 2024.

ROOT’s Return on Capital

Return on equity (ROE) in the trailing 12 months was 15.3%, outperforming the industry average of 7.3%. ROE, a profitability measure, reflects how effectively a company is utilizing its shareholders’ funds. It is noteworthy that ROOT has been generating improved ROE.

The same holds true for return on invested capital (ROIC), which has been improving over time. This reflects ROOT’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 8.7%, higher than the industry average of 5.7%.

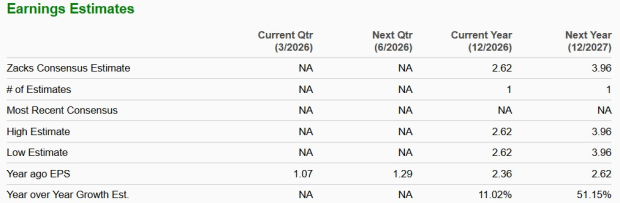

Growth Estimates of ROOT

The Zacks Consensus Estimate for 2026 and 2027 earnings implies a 11% and 51.2% year-over-year increase, respectively. The company has a Growth Score of A.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for 2026 and 2027 earnings has witnessed no movement in the last 30 days.

The consensus estimate for 2026 and 2027 earnings of LMNDLMND-- has moved north in the past 30 days. While the consensus estimate for EVER’s 2026 earnings moved south in the past 30 days, the same for 2027 moved north.

What to Do With ROOT Shares Now?

ROOT intends to continue to invest in business and technology, leverage telematics and data science to price auto insurance and target lower-risk drivers. Long-term upside depends on loss ratio improvement, regulatory navigation, and scaling profitable growth while maintaining disciplined capital management over time sustainably. A VGM Score of A instill confidence.

Given its premium valuation, investors can adopt a wait-and-see approach for this Zack Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EverQuote, Inc. (EVER): Free Stock Analysis Report

Lemonade, Inc. (LMND): Free Stock Analysis Report

Root, Inc. (ROOT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios