Root, Inc. (NASDAQ:ROOT): Is the Market Mispricing a Long-Term Winner Amid Short-Term Volatility?

Root, Inc. (NASDAQ:ROOT) has seen its stock dip 2.38% in post-earnings trading despite a remarkable Q2 2025 performance that underscores its transformation into a profitable, technology-driven insurer. With a net income of $22 million—up from a $7.8 million loss in Q2 2024—and record gross earned premiums of $371 million, the company has demonstrated its ability to turn strategic adjustments into tangible results[2]. Yet, the market's muted reaction raises a critical question: Is Root's stock being unfairly discounted, or does the volatility reflect legitimate concerns about its long-term execution?

Historical data on earnings-related price movements offers a nuanced perspective. A backtest of ROOT's performance around earnings releases from 2022 to 2025 reveals that the stock has historically outperformed the benchmark by a median of 47% over a 30-day window, compared to the benchmark's 19%[3]. While this pattern is not statistically significant at conventional levels, it suggests a tendency for positive drift following earnings events. Notably, the win-rate for holding the stock improves from 33% on the day of the earnings release to 58% by day 30, though the small sample size (12 events) and high volatility warrant caution[3].

Strong Fundamentals, Strategic Shifts, and a Changing Risk Profile

Root's Q2 results highlight a company in ascension. Its net combined ratio improved to 95.2%, a 750-basis-point drop from 102.7% in the prior year, signaling underwriting profitability[3]. This was driven by a reduced gross accident period loss ratio (59.6% in Q2 2025 vs. 61.0% in Q2 2024) and a strategic overhaul of its reinsurance program, which cut ceded premiums to 4.9% of gross premiums earned from 15.1%[3]. These moves reflect a disciplined approach to risk management and capital efficiency.

However, growth comes at a cost. Policies in force rose to 455,493 as of Q2 2025, up 12% year-over-year, but this expansion was accompanied by a 70.5% quarter-over-quarter spike in other insurance expenses, largely due to partnership commissions[3]. While such costs are a natural byproduct of scaling, they underscore the challenge of balancing growth with margin preservation.

Valuation Metrics Suggest a Mispricing Opportunity

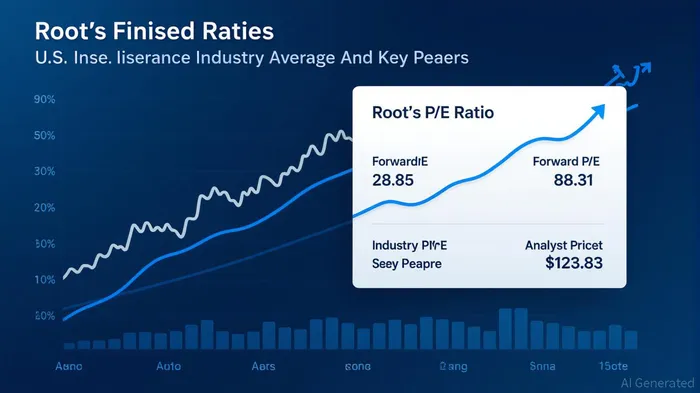

Root's valuation appears disconnected from its fundamentals. The stock trades at a trailing P/E of 20.85 and a forward P/E of 88.31[1], significantly above the U.S. insurance industry's average P/E of 15.9x[2]. Yet, this premium is not unwarranted when considering Root's technological edge. The company's R&D investments—$47.2 million in 2023—have fueled innovations like a 68% faster quote generation system and AI-driven underwriting models[1], which position it to outperform peers in a market where 68% of consumers prioritize digital convenience[1].

Comparisons to peers further highlight this disconnect. Metromile trades at a P/E of 52.4x, while Clearcover and Nationwide Digital are valued at 18.24x and 9.23x, respectively[3]. Root's price-to-book ratio of 6.21 also dwarfs the industry average of 1.57[3], reflecting the market's premium for its intangible assets—data, technology, and customer acquisition efficiency. Analysts, meanwhile, see upside: The average 12-month price target of $123.83 implies a 22.92% potential gain from current levels[3].

Industry Tailwinds and Long-Term Catalysts

The insurtech sector is poised for explosive growth, with a projected CAGR of 26% from 2025 to 2032[2]. Root's focus on telematics, AI, and embedded insurance aligns perfectly with these trends. Its partnerships with CarvanaCVNA--, Hyundai Capital America, and Experian[1] are expanding distribution channels, while its 54% drop in interest expense to $5.3 million[3]—thanks to favorable loan terms—boosts financial flexibility.

Yet, risks persist. Rising marketing costs and the phasing out of reinsurance partnerships could pressure margins in the short term[1]. Additionally, the company's forward P/E of 88.31 suggests skepticism about near-term earnings growth, which may be why the stock fell despite beating estimates.

Conclusion: A Calculated Bet on Innovation

Root's stock weakness appears to be a function of near-term guidance caution and the market's inherent wariness of high-growth tech plays, not a reflection of its long-term potential. The company's financial discipline, technological moat, and alignment with industry tailwinds make it a compelling candidate for long-term investors willing to weather volatility. At current levels, RootROOT-- offers a rare combination of proven execution, disruptive innovation, and a valuation that, while elevated, is justified by its trajectory in a $96.1 billion insurtech market by 2032[2].

For those with a multi-year horizon, the current dip may represent an opportunity to invest in a company that is redefining insurance—one algorithm, one policy, and one customer at a time.

Comentarios

Aún no hay comentarios