Rollins' Q3 2025 Earnings: What to Expect

As RollinsROL--, Inc. (ROL) prepares to release its Q3 2025 earnings on October 22, 2025, investors are keenly focused on how the company's operational resilience and market positioning will hold up amid shifting retail and real estate dynamics. With analysts forecasting an adjusted earnings per share (EPS) of $0.33 for the quarter-a 13.8% increase from $0.29 in the same period last year-Rollins' ability to navigate macroeconomic headwinds will be critical to its performance, according to a Yahoo Finance preview.

Operational Resilience: A Track Record of Growth

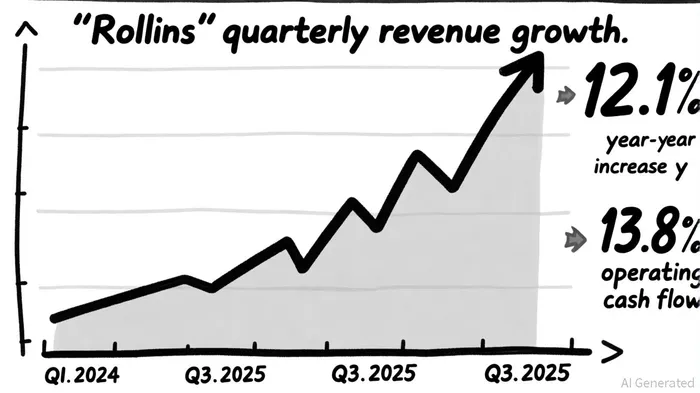

Rollins has demonstrated consistent operational strength in recent quarters. In Q2 2025, the company reported a 12.1% year-over-year revenue increase to $999.5 million, driven by 7.3% organic growth and 4.8% from acquisitions, including the integration of Saela Pest Control, according to a Rollins press release. Adjusted EPS for Q2 rose 11.1% to $0.30, outpacing expectations. Operating cash flow surged 20.7% to $175 million, underscoring the company's financial discipline, as shown in Rollins SEC filings.

However, margin pressures persist. Rising operational costs, particularly in insurance and fleet expenses, led to a 60-basis-point decline in operating margins to 19.8% in Q2 2025, according to an Investing.com report. Rollins' capital allocation strategy, which includes strategic acquisitions and shareholder returns, remains a key differentiator. The company invested $254 million in acquisitions during the first half of 2025 and returned $79 million to shareholders via dividends, per the Investing.com earnings page.

Market Positioning: Retail and Real Estate Tailwinds

The retail and real estate sectors are undergoing significant transformation, and Rollins is well-positioned to benefit. In the retail space, limited new development pipelines and high capital costs have constrained supply, keeping retail vacancy rates at historic lows and driving up asking rents, as noted in the CBRE retail outlook. This environment favors well-located properties, such as grocery-anchored centers and experiential retail hubs, which align with Rollins' services for foodservice and logistics clients.

In commercial real estate, industrial and shopping center sectors are posting positive net operating income (NOI) growth, while office and self-storage face declines, according to Aprio insights. Rollins' Commercial segment, which includes pest and termite control for businesses, is likely to see sustained demand from industrial and retail tenants seeking to maintain operational efficiency. For example, the company's Q2 2025 Commercial revenue grew 10.1% year-over-year to $299.63 million, according to a Yahoo Finance article, a trend that could accelerate in Q3 as industrial activity remains robust.

The residential real estate market is also stabilizing. Multifamily construction activity has cooled, with units under construction declining to 706,000 in Q3 2025 from a peak of nearly 1 million earlier in the year, Aprio notes. This slowdown, coupled with rising home inventory, signals a return to balance in the housing market. Rollins' Residential segment, which saw a 5.9% year-over-year revenue increase to $428.29 million in Q2 2025, per the Rollins 10-Q, stands to benefit from sustained demand for pest control services in both new and existing housing stock.

Challenges and Opportunities

While Rollins' recurring revenue model and market leadership provide a strong foundation, challenges remain. Margin pressures from operational costs and integration risks from acquisitions could weigh on profitability. Additionally, economic uncertainties, such as inflation and interest rate volatility, may dampen consumer and business spending.

However, the company's strategic initiatives-such as technology investments and operational efficiencies-aim to offset these risks. Rollins targets a 30% incremental EBITDA margin improvement through automation and process optimization, according to a Monexa analysis, a goal that could enhance long-term profitability.

Conclusion: A "Moderate Buy" in a Shifting Landscape

Analysts maintain a "Moderate Buy" rating for ROLROL-- stock, with a 5% potential upside from current levels, per a Barchart article. Rollins' Q3 2025 earnings will be a critical test of its ability to sustain growth amid evolving retail and real estate dynamics. If the company meets or exceeds the $0.33 adjusted EPS forecast, it could reinforce investor confidence in its operational resilience and market positioning.

Historical data from 2022 to 2025 suggests that a simple buy-and-hold strategy following ROL's earnings releases has yielded a 61.7% win ratio over 30 trading days, with an average cumulative excess return of +2.66% compared to the benchmark. While these results are not statistically significant, they indicate a modestly positive trend for investors who have historically held the stock post-earnings.

Comentarios

Aún no hay comentarios