Roku's Q2 2025 Earnings and Strategic Moves: A Path to Sustained Growth in a Competitive Streaming Landscape

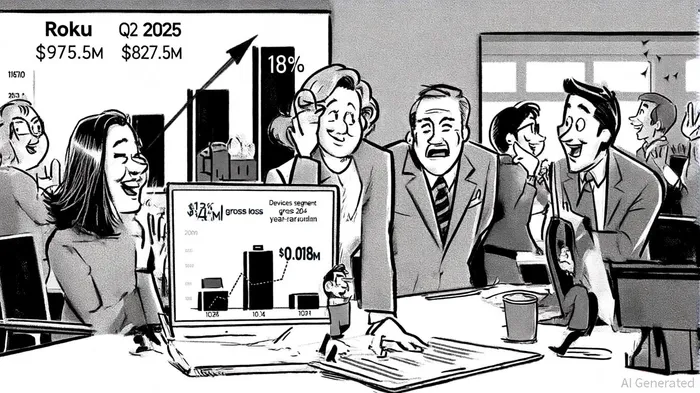

In Q2 2025, RokuROKU-- (ROKU) delivered a stunning financial turnaround, posting a net profit of $10.5 million—a stark reversal from a $34 million net loss in the same period the prior year[1]. Total revenue surged 15% year-over-year to $1.11 billion, driven by a 18% increase in platform revenue to $975.5 million[2]. This growth underscores Roku's successful pivot toward monetizing its ecosystem through advertising and subscription services, with streaming hours on its platform rising 17% to 35.4 billion[3]. The Devices segment, historically a drag on profitability, saw its gross loss shrink to a negligible $0.018 million, reflecting a strategic shift toward higher-margin Roku-branded TVs[1].

Market Position: Dominance in Devices, Challenges in Content

Roku maintains a commanding 66.5% market share among cord-cutters in North America, outpacing AmazonAMZN-- Fire TV (30.3%), Google TV (20.6%), and AppleAAPL-- TV (16.8%)[4]. However, its revenue-based market share in the broader Broadcasting Media & Cable TV industry remains modest at 1.96%, trailing ComcastCMCSA-- (55.3%) and NetflixNFLX-- (18.9%)[5]. This dichotomy highlights Roku's role as a device and platform enabler rather than a content creator. While Amazon Prime Video and Netflix dominate streaming service usage in the U.S. (22% and 21%, respectively), Roku's strength lies in its neutral platform strategy, aggregating content from multiple providers and offering affordability and ease of use[6].

Strategic Initiatives: Advertising, AI, and Global Expansion

Roku's long-term growth hinges on three pillars: advertising innovation, AI-driven personalization, and international expansion. The company's partnership with Amazon Ads now reaches 80 million U.S. connected TV (CTV) households, enhancing ad targeting and measurement capabilities[7]. Additionally, Roku launched the Roku Data Cloud in January 2025, providing advertisers with proprietary TV data to refine campaigns[8]. These moves position Roku to capture a share of the $40 billion CTV advertising market projected for 2027[9].

Technologically, Roku is investing heavily in AI-powered features, including a recommendation engine to boost content discovery and user engagement[10]. Its 2025 hardware lineup—featuring the Pro Series with Mini-LED and 120Hz refresh rates—caters to premium users while maintaining its budget-friendly Select Series[11]. Internationally, Roku aims to expand into five new markets by Q3 2025 and localize content for 15 markets, with 30% of its active accounts already outside the U.S.[12].

Challenges and Risks

Despite its momentum, Roku faces headwinds. Rising competition from Amazon, Apple, and Google—each with deep pockets and integrated ecosystems—threatens to erode its market share[13]. Consumer fatigue with subscription costs has also led to a 44% cancellation rate for SVOD services, pushing users toward free ad-supported streaming (FAST) platforms like Tubi and Pluto TV[14]. Roku's own foray into original content, such as the $12 million Weird Al biopic, is a step toward differentiation but pales against the budgets of Netflix or Disney[15].

Regulatory challenges further complicate its global ambitions. A U.S. court recently dismissed Roku's attempt to set a global FRAND royalty rate for HEVC patents, underscoring the jurisdictional hurdles in international expansion[16]. Meanwhile, R&D spending surged 75% year-over-year to $221 million in one quarter, raising questions about how quickly these investments will translate into profitability[17].

Long-Term Outlook: A Neutral Platform in a Fragmented Market

Roku's strategic focus on platform monetization and user retention bodes well for its long-term prospects. With 89.8 million active accounts and 253.7 minutes of daily streaming per user in Q4 2024[18], the company has demonstrated its ability to sustain engagement. Its guidance for double-digit platform revenue growth and operating income positivity by Q4 2025[19] reflects confidence in its advertising and subscription models.

Historically, a simple buy-and-hold strategy following Roku's earnings releases has shown a modest edge, with an average 5.6% cumulative return over 30 days compared to the benchmark[20]. However, the statistical significance of this edge remains weak, suggesting that while the trend is encouraging, it should not be the sole basis for investment decisions.

However, Roku must navigate a fragmented streaming landscape where consumer preferences are shifting toward bundling and personalized ad experiences[20]. Its success will depend on maintaining its device dominance while expanding its content and advertising offerings to compete with vertically integrated rivals. For investors, Roku represents a high-growth opportunity in the CTV revolution—but one that requires patience as it balances innovation with profitability.

Comentarios

Aún no hay comentarios