Rithm Capital (RITM): A Case of Valuation Misalignment Amid Rising Markets

In the current market environment, where broad indices like the S&P 500 have surged by 19.44% year-to-date (TTM) [1], Rithm CapitalRITM-- (RITM) has exhibited a mixed performance. While the stock has delivered a 13.86% TTM return [1], it lags behind the S&P 500 and underperforms its software industry peers, which have averaged 8.20% YTD [3]. This divergence raises questions about valuation misalignment and the potential for a re-rating.

Valuation Misalignment: A Tale of Contrasts

RITM's valuation metrics starkly contrast with those of its peers. As of September 2025, the stock trades at a price-to-earnings (P/E) ratio of 9.6x, significantly below the U.S. Mortgage REITs industry average of 13.9x and the software sector's peer average of 21.5x [1]. This suggests RITMRITM-- is undervalued relative to both its sector and the broader market. Additionally, its enterprise value to EBITDA (EV/EBITDA) ratio of 53.83 [3] appears inflated compared to SaaS benchmarks, where infrastructure SaaS trades at 6.9x NTM revenue [1]. This disconnect hints at a potential mispricing, particularly given RITM's robust fundamentals.

Fundamentals: Profitability vs. Leverage

RITM's financials underscore its resilience. The company reported a net income of $726.28 million in the last 12 months, translating to a 21.89% net profit margin [3]. Such profitability is rare in the mortgage REIT space, where declining earnings have historically plagued the sector [3]. However, its debt-to-equity ratio of 3.93 [3]—far exceeding the REITs industry average of 0.88 [3]—introduces risk. While leverage amplifies returns in favorable conditions, it also heightens vulnerability during interest rate hikes or liquidity crunches.

Catalysts for Re-Rating

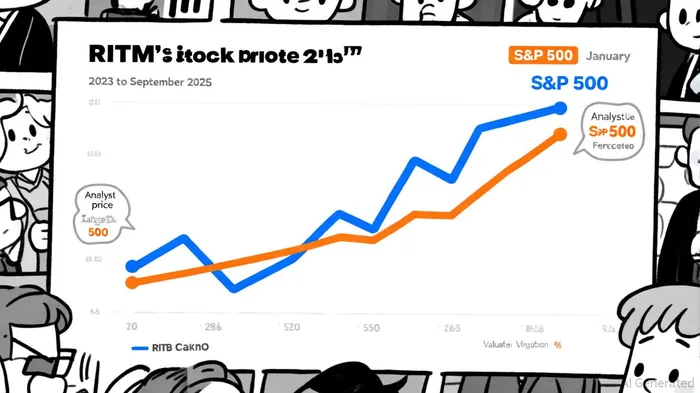

Analysts project a compelling upside for RITM. A consensus price target of $13.69 implies a 14.64% potential gain from its current price of $11.94 [2]. This optimism is grounded in RITM's outperformance in the software industry index (18.63% YTD vs. 8.20% median) [3] and its ability to maintain a 17.05% CAGR over three years [1]. Furthermore, the stock's low P/E ratio suggests a margin of safety, particularly as broader market multiples expand.

Risk/Reward Dynamics

The investment case for RITM hinges on balancing its undervaluation with structural risks. On the reward side, its profitability and strong analyst ratings (average “Buy” recommendation) [2] justify a re-rating. On the risk side, the high debt load and recent technical downgrade to “Sell candidate” [3] warrant caution. Investors must weigh RITM's potential to narrow its valuation gap against macroeconomic headwinds, such as rising interest rates, which could pressure its leverage-heavy model.

Conclusion

Rithm Capital presents an intriguing opportunity for investors seeking undervalued assets in a rising market. Its valuation metrics, while at odds with peers, align with its strong earnings and industry-leading profit margins. However, the path to re-rating is not without hurdles. For those who can tolerate the risks of high leverage, RITM's combination of mispricing and catalysts—from analyst optimism to sector-specific tailwinds—makes it a compelling case study in valuation arbitrage.

Comentarios

Aún no hay comentarios