The Risks and Opportunities in the U.S. Student Loan Market Amid Political and Economic Shifts

The U.S. student loan market is at a crossroads, shaped by a confluence of political policy shifts, economic pressures, and evolving credit risk dynamics. As federal student loan payments resumed in October 2023 after a three-year pandemic pause, the ripple effects on household spending, borrower behavior, and asset-backed securities (ABS) markets have become impossible to ignore. For investors, the interplay between policy uncertainty, rising delinquencies, and structural changes in repayment frameworks presents both significant risks and nuanced opportunities.

Political and Economic Shifts: A Double-Edged Sword

The resumption of federal student loan payments has had an immediate and measurable impact on consumer spending. According to a Federal Reserve analysis, households with high exposure to student debt curtailed spending by an estimated $80 billion annually, a drag on aggregate demand that disproportionately affected regions with higher concentrations of college-educated borrowers. This shift underscores the sensitivity of the broader economy to student loan policy changes.

Simultaneously, legislative actions under the Trump administration-such as the One Big Beautiful Bill Act-have introduced structural shifts in repayment and forgiveness. The Biden-era SAVE plan, which offered low monthly payments and expedited forgiveness, is being phased out by 2028, forcing borrowers into new repayment structures like the Repayment Assistance Plan (RAP) or the standard plan, as reported by an NPR report. These changes, coupled with reduced borrowing limits for graduate and parent PLUS loans, have created uncertainty for borrowers and lenders alike.

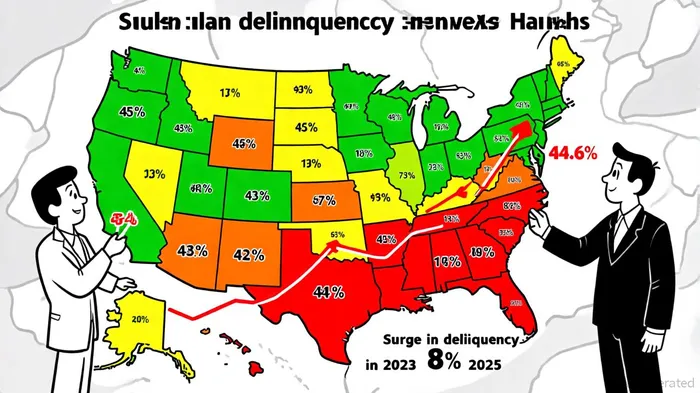

Credit Risk in Student Loan ABS: A Ticking Time Bomb?

The resumption of payments has also triggered a sharp rise in delinquency rates, with over nine million borrowers now behind on payments as of early 2025, according to a New York Fed analysis. Delinquency rates surged from below 1% to nearly 8%, with prime and superprime borrowers-historically considered low-risk-experiencing the most significant credit score drops (165–171 points on average), based on a CSLA Institute analysis. This erosion of credit quality has profound implications for ABS investors.

For asset-backed securities collateralized by student loans, the degradation of borrower credit profiles has forced a reevaluation of risk models. Traditional assumptions about repayment behavior are no longer valid, as shown in a ReceivablesInfo analysis, which documents 15% delinquency among prime borrowers and 11% among superprime borrowers. Investors must now incorporate dynamic indicators like real-time employment status and digital engagement into their models, moving beyond static thresholds.

Geographic disparities further complicate the picture. Southern states like Mississippi report delinquency rates as high as 44.6%, while borrowers over 40 with delinquencies represent a growing demographic risk, the New York Fed shows. These trends threaten the diversification of ABS portfolios and could lead to downgrades in credit ratings for student loan-backed securities.

Investor Responses: Navigating Uncertainty

Despite these risks, the student loan ABS market has shown resilience. In 2024, issuance totaled $9.3 billion, a modest increase from $8.3 billion in 2023, according to a Fitch report. However, investors remain cautious. Fitch Ratings notes that elevated delinquency rates in private student loan collateral pools and macroeconomic pressures-such as inflation and high interest rates-are likely to persist.

Investor strategies are adapting to this environment. Some lenders now exclude forborne student loans from debt-to-income calculations, while others rely on credit bureau data to assess risk, as highlighted in a Loomis Sayles blog. Meanwhile, fintech innovations and private refinancing platforms are emerging as stabilizing forces, offering structured pathways for borrowers navigating federal policy instability-an observation Loomis Sayles also emphasizes.

Opportunities Amid the Storm

While the risks are clear, the market also presents opportunities for savvy investors. The student loan market is projected to grow from $4.47 trillion in 2025 to $6.19 trillion by 2030, driven by government funding expansion, fintech innovation, and new income-driven repayment rules, according to Mordor Intelligence. Non-bank financial companies (NBFCs) are gaining traction, offering agile, technology-driven solutions to borrowers with limited financial histories, a trend Mordor Intelligence highlights.

For ABS investors, the key lies in balancing risk mitigation with growth potential. This includes prioritizing high-quality collateral pools, leveraging behavioral data in risk models, and hedging against policy volatility through diversified portfolios.

Conclusion

The U.S. student loan market is a microcosm of broader economic and political tensions. While rising delinquencies and policy uncertainty pose significant risks to ABS investors, the sector's projected growth and technological advancements offer a counterbalance. For those willing to navigate the complexities of credit risk assessment and policy forecasting, the market remains a compelling-if volatile-arena for strategic investment.

Comentarios

Aún no hay comentarios