Rising Redress Costs in UK Motor Finance: Implications for Lenders and Investors

The UK motor finance sector is navigating a seismic shift as the Financial Conduct Authority (FCA) rolls out a sweeping redress scheme to address historical mis-selling practices. This initiative, aimed at rectifying opaque commission arrangements between brokers and lenders, has triggered a cascade of financial and operational challenges for institutions. For investors, the implications extend beyond short-term volatility, raising critical questions about credit risk, balance sheet resilience, and the long-term sustainability of the sector.

The Financial Burden of Redress

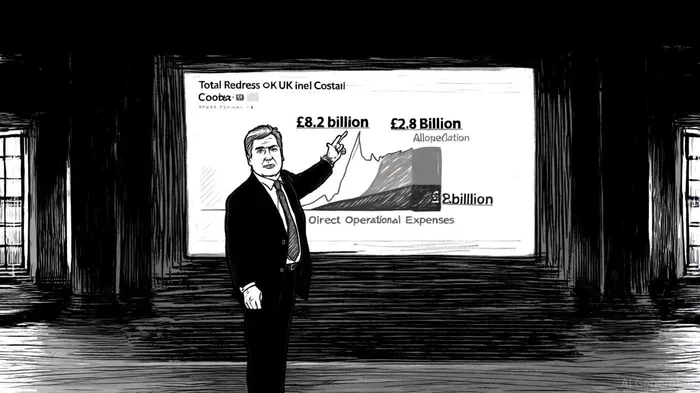

According to a Grant Thornton report, the FCA's proposed redress scheme could impose a total industry cost of £11 billion, comprising £8.2 billion in direct compensation and £2.8 billion in operational expenses. These figures reflect the scale of the problem: the scheme targets up to 30 million motor finance agreements spanning 2007 to 2024, with individual compensation averaging £700 per affected customer, according to the Grant Thornton report. For context, this exceeds the £2 billion in provisions already set aside by UK banks in 2025, as highlighted by Fitch Ratings.

The operational complexity of the redress process further amplifies costs. The FCA's two-tier model-offering either a full commission refund or an APR adjustment remedy-requires meticulous data reconciliation and customer communication, tasks that demand significant resource allocation, Grant Thornton notes. Smaller lenders, in particular, face disproportionate challenges. Bank of Ireland warned, for instance, that its redress provision may double to £350 million, potentially reducing its common equity tier 1 ratio by 35 basis points. This underscores a broader trend: mid-sized banks, already constrained by tighter capital buffers, may struggle to absorb these costs without compromising credit quality.

Credit Risk and Balance Sheet Vulnerability

The redress scheme's impact on credit risk is twofold. First, the sheer magnitude of provisions required could strain liquidity and capital adequacy ratios. As noted by The Banker, the total redress liability could reach £18 billion, with major lenders like Lloyds Banking Group, Santander UK, and Close Brothers Group already provisioning between £30 million and £700 million. Such outflows risk eroding profitability and increasing leverage ratios, particularly for institutions with limited diversification.

Second, the reputational fallout from prolonged redress processes could indirectly affect credit metrics. A protracted resolution may deter new customers, reduce broker partnerships, and trigger regulatory scrutiny, all of which could depress revenue streams. For example, the Supreme Court's recent ruling limiting liability for some mid-sized banks has created uncertainty, forcing institutions to reassess their risk exposures, a point also highlighted by The Banker. This legal ambiguity adds a layer of volatility to balance sheets, complicating forward-looking financial planning.

Investor Considerations

For investors, the redress crisis highlights the importance of sector-specific risk assessment. While large banks with robust capital bases may weather the storm, smaller players face existential threats. Diversification across asset classes and geographies becomes critical, as the UK motor finance sector's vulnerabilities could ripple through broader financial markets.

Moreover, the FCA's emphasis on fairness and proportionality in redress calculations, as outlined in the Grant Thornton report, suggests a regulatory environment that prioritizes consumer protection over institutional flexibility. This shift could lead to stricter compliance requirements, further elevating operational costs and reducing margins. Investors must also monitor the timeline for redress implementation, as delays in compensation disbursement could exacerbate liquidity pressures.

Conclusion

The UK motor finance redress scheme is a watershed moment for the sector, exposing deep-seated vulnerabilities in credit risk management and balance sheet resilience. While the FCA's structured approach aims to balance fairness and efficiency, the financial toll on lenders-particularly smaller institutions-remains a pressing concern. For investors, the path forward demands a nuanced understanding of regulatory dynamics, capital adequacy trends, and the long-term implications of redress costs. As the industry navigates this transition, vigilance and strategic adaptability will be paramount.

Comentarios

Aún no hay comentarios