Can Rising Hyperscaler Demand Fuel Everpure's FY27 Revenue Growth?

Everpure’s PSTG expanding hyperscaler business is emerging as a meaningful driver of its growth strategy, as demand for high-performance, energy-efficient storage accelerates amid the proliferation of AI and large-scale cloud workloads.

PSTG expects fiscal 2027 revenues to be between $4.3 billion and $4.4 billion, indicating 18.8% year-over-year growth at the midpoint, with operating profit of $780–$820 million expected to rise about 26%. A key driver behind this outlook is the continued expansion of its hyperscaler business, especially in the second half of the fiscal year. PSTGPSTG-- also highlighted that the hyperscaler business performed better than expectations in fiscal 2026.

In fiscal 2026, the company focused on scaling its hyperscaler line of business and now anticipates significantly higher shipments and revenues in fiscal 2027 compared with the prior year. However, revenues are aligned with the hyperscalers data center buildouts and are not linear, added PSTG.

Everpure, Inc. Price, Consensus and EPS Surprise

Everpure, Inc. price-consensus-eps-surprise-chart | Everpure, Inc. Quote

The company has also standardized its business model for hyperscale customers. Looking forward, EverpurePSTG-- will procure certain components required for hyperscale deployments, while hyperscalers will source NAND through their own supply chains. This structure is expected to deliver hyperscaler gross margins between 75% and 85%, which management believes will be accretive to both product margins as well as overall gross margins.

However, rising memory and NAND prices and industry-wide component shortages remain potential headwinds. The company noted that it has built a diversified supply chain with contingency plans to reduce disruption risks, supported by strong supplier relationships and in-house hardware design.

The commentary surrounding hyperscale business suggests that this business is meant to be a strategic lever to expand Pure Storage’s addressable market and support long-term growth.

Let’s Look at Rivals’ Hyperscaler Ties

NetApp NTAP is one of Everpure’s direct competitors. On the last earnings call, management noted that first-party ties with hyperscale cloud customers are a key differentiator. Its partnerships with major hyperscalers such as Amazon and Microsoft, through offerings like Amazon FSx for NetApp ONTAP and Microsoft Azure NetApp Files, solidify NetApp’s position as a critical player in the cloud infrastructure space, which is poised for continued growth as enterprises migrate more workloads to the cloud.

Solid momentum in hyperscaler first-party and marketplace storage services has been driving revenue growth in the Public Cloud segment. Excluding Spot, Public Cloud revenues grew 17% year over year. First-party and marketplace cloud storage services grew 27%. Management added that these services are helping it acquire new clients, with half of the revenues from new first-party and marketplace customers coming from organizations new to NetApp.

Western Digital Corporation WDC is working closely with hyperscale customers to deliver high-capacity, reliable drives at scale, focusing on performance and total cost of ownership. The company is advancing areal density gains, accelerating its HAMR and ePMR roadmaps, and driving adoption of higher-capacity and UltraSMR drives. In the fiscal second quarter, Western Digital shipped more than 3.5 million latest-generation ePMR drives, supporting up to 26TB CMR and 32TB UltraSMR capacities, underscoring strong customer adoption. The company shipped a total of 215 exabytes to customers, marking a 22% year-over-year increase. The reliability, scalability and TCO benefits of its ePMR and UltraSMR technologies remain key to its success in the data center market.

Western Digital reaffirmed its dual-path leadership in ePMR and HAMR, with the 40TB UltraSMR ePMR HDD now in qualification at two hyperscalers and volume production targeted for the second half of fiscal 2026, while HAMR drives are also being qualified, with ramp expected in 2027.

PSTG Price Performance, Valuation and Estimates

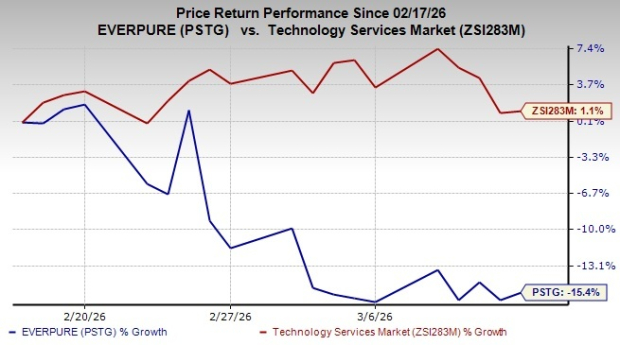

Shares of PSTG have lost 15.4% in the past month against the Technology Services’ industry’s growth of 1.1%.

Image Source: Zacks Investment Research

Regarding the forward 12-month price/earnings ratio, PSTG is trading at 25.68, higher than the sector’s multiple of 21.92.

Image Source: Zacks Investment Research

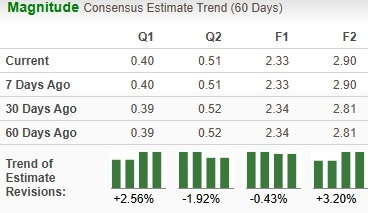

The Zacks Consensus Estimate for PSTG’s earnings for fiscal 2027 has been revised downward marginally over the past 60 days.

Image Source: Zacks Investment Research

PSTG currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NetApp, Inc. (NTAP): Free Stock Analysis Report

Western Digital Corporation (WDC): Free Stock Analysis Report

Everpure, Inc. (PSTG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios