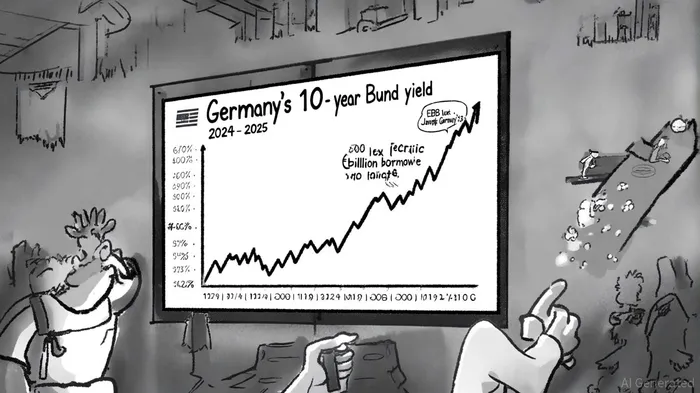

Rising German Bund Yields and the Implications for Global Fixed Income Markets

The global fixed income landscape in 2025 is being reshaped by the interplay of divergent monetary policies, fiscal expansion, and shifting investor preferences. At the heart of this transformation lies the German 10-year Bund, whose yield has climbed to 2.67% as of September 9, 2025, reflecting a complex mix of domestic fiscal pressures and international uncertainties[1]. This rise, though modest compared to historical volatility, signals a structural shift in how investors perceive risk and return in an era of monetary policy divergence between the European Central Bank (ECB) and the U.S. Federal Reserve (Fed).

Monetary Policy Divergence: ECB Caution vs. Fed Easing

The ECB's decision to maintain its policy rate at 4% since September 2023, despite three 25-basis-point cuts in 2024, underscores its cautious approach to inflation and economic stagnation in the eurozone[3]. By contrast, the Fed's anticipated September 2025 rate cut—driven by weak U.S. labor data—has created a stark policy asymmetry. This divergence has pushed the U.S. Treasury-Bund yield spread to 44 basis points, its steepest in years[5]. Investors are recalibrating portfolios to exploit this gap, with Bunds increasingly seen as a hedge against U.S. fiscal and geopolitical risks, including President Trump's proposed tariffs and inflationary pressures[2].

The ECB's reluctance to aggressively cut rates is further complicated by Germany's fiscal ambitions. The country's €500 billion borrowing plan through 2029 to fund defense and infrastructure projects will swell Bund issuance, potentially crowding out private capital and pushing yields higher[1]. This dynamic contrasts with the Fed's easing cycle, which has depressed U.S. Treasury yields and prompted institutional investors to seek higher returns in riskier assets.

Strategic Allocation: Duration, Diversification, and Dovish Bets

Institutional investors are adapting to these conditions by refining duration strategies. With the ECB nearing the end of its rate-cutting cycle, many are favoring 5- to 10-year Bunds to balance yield pickup and interest rate risk[1]. Shorter-duration bonds, meanwhile, have attracted inflows as investors hedge against potential volatility from geopolitical shocks or a reversal in the Fed's dovish stance[2]. This shift is evident in record inflows into short-term euro government bond funds, signaling a preference for liquidity and flexibility[2].

Cross-asset implications are equally significant. When U.S. Treasury returns decline, investors typically reallocate to global corporate or emerging market bonds. However, in the eurozone, rebalancing is largely confined to sovereign bonds, particularly Bunds[1]. This regional substitution reinforces fragmentation in European fixed income markets and limits the global spillover of ECB policy. For example, Germany's pivot to domestic infrastructure spending has reduced its reliance on export-driven growth, altering the eurozone's net international investment position and reshaping EUR/USD dynamics[5].

Term Premium, Fiscal Risks, and the New Normal

Looking ahead, Bund yields are expected to remain elevated due to a combination of structural inflation risks and a higher term premium. Analysts project the 10-year yield to trade between 2.6% and 3.1% through 2026, with the risk-neutral yield climbing above 1.7% and the term premium stabilizing near 1.1%[4]. These trends reflect a broader end to the era of cheap money, as investors demand compensation for heightened fiscal and geopolitical uncertainties.

Germany's ability to service its growing debt burden will hinge on the success of its infrastructure and defense programs in boosting productivity. However, the ECB's shrinking holdings of Bunds—due to reduced quantitative easing—may amplify supply-side pressures, further supporting yields[4]. For global investors, this environment necessitates a nuanced approach: leveraging Bunds' safe-haven appeal while hedging against currency and duration risks in a fragmented world.

Conclusion: Navigating the New Fixed Income Paradigm

The rise in German Bund yields is not an isolated phenomenon but a symptom of broader shifts in global capital flows and policy frameworks. As the ECB and Fed chart divergent paths, investors must prioritize agility in their fixed income strategies. This means favoring intermediate-duration Bunds, closely monitoring fiscal developments in Germany and the U.S., and preparing for a world where safe assets command higher premiums. In this new paradigm, strategic allocation is less about predicting rates and more about managing risk in a landscape defined by uncertainty.

Comentarios

Aún no hay comentarios