The Rising Cost of Higher Education and Its Impact on Consumer Spending and Financial Services

The U.S. higher education system is at a breaking point. Tuition and fees at four-year institutions have surged beyond inflation, with in-state public university costs rising 133% from 2005 to 2025 and private institutions seeing a 126% increase [1]. Total student debt now exceeds $1.77 trillion, with borrowers averaging $40,000 in debt [2]. This crisis is reshaping consumer spending patterns and creating fertile ground for innovation in financial services. For investors, the intersection of rising education costs and evolving financial solutions presents compelling opportunities in student loan refinancing, financial aid technology, and family financial planning services.

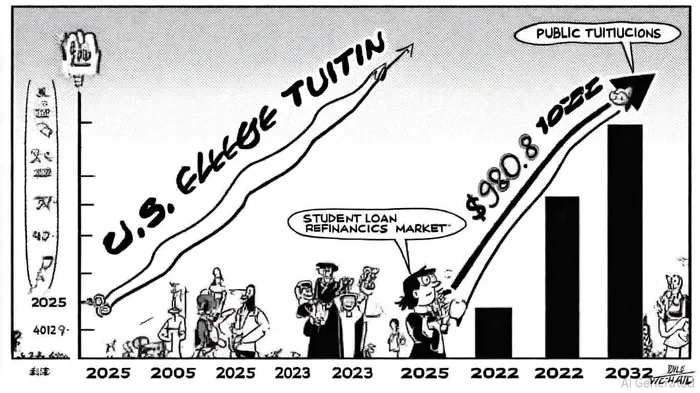

The Student Loan Refinancing Boom

The student loan refinancing market is experiencing explosive growth, driven by fintech disruption and shifting borrower needs. The private student loan sector, valued at $412.7 billion in 2023, is projected to expand to $980.8 billion by 2032, growing at a compound annual rate of 10.1% [3]. Fintechs like SoFiSOFI-- and Ascent are leading the charge, leveraging lower overhead and alternative credit models to offer competitive rates and flexible repayment terms. For example, SoFi's no-fee structure and APRs ranging from 4.19% to 14.83% have attracted borrowers seeking to reduce interest burdens [4]. Traditional banks, including Sallie Mae and Citizens Bank, remain in the market but are increasingly outpaced by fintechs' agility and customer-centric innovation.

Regulatory shifts, such as the phase-out of the SAVE repayment plan and the introduction of the Repayment Assistance Plan (RAP), are further driving demand for refinancing solutions. Borrowers now face stricter repayment terms, with interest resuming for 8 million individuals previously enrolled in the SAVE plan [5]. This creates a window for fintechs to offer tailored refinancing options, particularly for those struggling with the new 30-year forgiveness timeline under RAP.

Financial Aid Tech: A New Frontier

Technology is transforming how students and families navigate financial aid. Platforms like LendKey and Credible are streamlining loan comparisons, while innovators like Stride Funding are experimenting with income share agreements (ISAs), where repayment is tied to future earnings [6]. These models appeal to borrowers wary of traditional debt structures, especially as underemployment rates for recent graduates hover above 40% [7].

The rise of AI and blockchain in financial aid tech is also noteworthy. AI-powered tools analyze spending patterns to predict financial risks and recommend debt management strategies, while blockchain enhances transparency in loan disbursements and repayment tracking [8]. For instance, fintechs are integrating embedded finance solutions into non-financial platforms, making student loan management more accessible to younger, tech-savvy users [9].

Family Financial Planning Services: Adapting to a New Normal

As education costs strain household budgets, demand for holistic financial planning services is surging. Consumers are seeking comprehensive advice that spans student loans, career transitions, and retirement planning. A 2025 KPMG report highlights a “make it count” mindset, with 50% of households cutting back on purchases and 49% prioritizing discounts [10]. This trend underscores the need for personalized, fee-based financial advice—a niche where fintechs are gaining traction.

Robo-advisors and AI-driven platforms are addressing this demand by offering automated budgeting, debt optimization, and tax planning. For example, platforms like FYvie Financial use machine learning to create customized repayment schedules, while blockchain-based solutions enhance security for sensitive financial data [11]. These innovations are particularly appealing to Gen Z and Millennials, who prioritize cost-effective, transparent services over traditional commission-driven models [12].

Consumer Spending and Regulatory Headwinds

The economic ripple effects of rising education costs are evident in broader consumer behavior. U.S. consumer spending growth is projected to slow to 3.7% in 2025, down from 5.7% in 2024, as lower- and middle-income households grapple with tariff-induced inflation and policy uncertainty [13]. Meanwhile, affluent consumers—many of whom are Gen Z and Millennials entering peak earning years—continue to drive discretionary spending [14]. This bifurcation creates opportunities for financial services tailored to both segments: affordable refinancing for middle-income borrowers and premium, tech-driven planning tools for high-net-worth clients.

Regulatory changes, such as the One Big Beautiful Bill Act, have further complicated the landscape. The phase-out of income-driven repayment (IDR) plans like PAYE and ICR, coupled with tighter borrowing caps for Parent PLUS loans, has increased default risks for vulnerable borrowers [15]. However, these challenges also highlight the need for robust financial planning services and innovative refinancing solutions.

Conclusion: A Lucrative but Complex Landscape

The rising cost of higher education is a crisis, but it is also a catalyst for innovation. Investors who target the student loan refinancing sector, financial aid technology, and family financial planning services stand to benefit from a market in flux. Fintechs with agile, customer-centric models are well-positioned to outperform traditional institutions, while regulatory shifts create both risks and opportunities. As borrowers navigate tighter repayment terms and economic uncertainty, the demand for personalized, tech-driven financial solutions will only grow.

For now, the key is to balance optimism with caution. While the market is ripe for disruption, macroeconomic headwinds—such as rising interest rates and regulatory uncertainty—require careful risk management. But for those who can navigate these challenges, the rewards are substantial.

Comentarios

Aún no hay comentarios