The Rise in Japan's Two-Year Government Bond Yield: A Harbinger of Policy Shifts and Market Reallocation

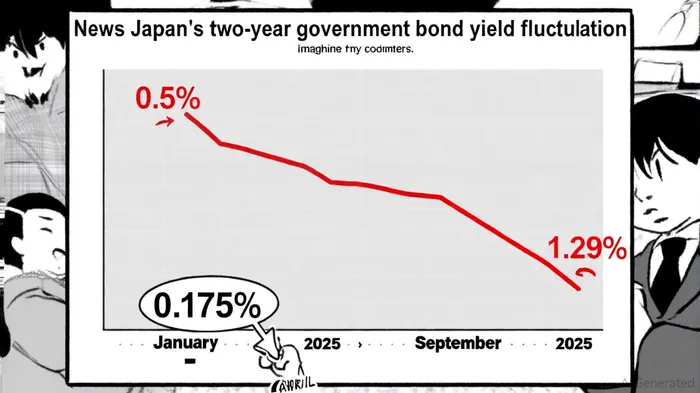

The recent volatility in Japan's two-year government bond yield has emerged as a focal point for global investors and policymakers, signaling a potential inflection point in the country's long-standing monetary strategy. By September 2025, the yield had climbed to 0.89%, a stark contrast to its April 2025 low of 0.625%—a 0.175% plunge driven by U.S. tariffs on Japanese imports and a subsequent flight to safe-haven assets[2]. This trajectory underscores a broader shift in Japan's economic landscape, where domestic policy constraints, global trade dynamics, and investor behavior are converging to reshape asset allocation strategies worldwide.

Drivers of Yield Volatility: Policy, Inflation, and Global Uncertainty

The Bank of Japan (BOJ) has maintained a cautious stance, keeping its short-term policy rate at 0.5% since January 2025 despite inflation hovering above 3%[2]. This reluctance to normalize monetary policy reflects a delicate balancing act: while inflationary pressures persist, the BOJ remains wary of abrupt rate hikes that could destabilize a fragile recovery. Meanwhile, the yen's depreciation—spurred by U.S. tariffs and accommodative BOJ policies—has amplified import costs, particularly for energy and raw materials, further complicating the central bank's calculus[2].

Global factors have also played a pivotal role. The imposition of U.S. tariffs on Japanese goods in early 2025 triggered a surge in demand for Japanese government bonds (JGBs), driving prices up and yields down[2]. However, this trend reversed in August and September as investors priced in the likelihood of tighter monetary policy and fiscal uncertainty. The BOJ's gradual reduction in bond-buying operations—a key component of its quantitative easing (QE) program—has further tightened liquidity, pushing yields upward[4].

Policy Implications: A Tipping Point for the BOJ?

The BOJ's 2025 Financial System Report highlights growing concerns about financial stability, particularly as non-bank financial intermediaries (NBFIs) increase their presence in Japan's bond markets[1]. This development has introduced new layers of volatility, as foreign investors' demand for JGBs becomes more sensitive to global risk sentiment. Additionally, the BOJ faces structural challenges, including a shrinking population and subdued corporate loan demand, which limit its ability to stimulate growth through traditional monetary tools[1].

Speculation is mounting that the BOJ may intensify QE efforts to weaken the yen further, a move that could boost export competitiveness but exacerbate inflationary pressures[2]. Such a policy shift would align with global trends, as nations increasingly prioritize economic self-reliance amid geopolitical tensions. However, with Japan's public debt exceeding 250% of GDP, the central bank's room for maneuver remains constrained[1].

Market Reallocation: Strategic Shifts in a Global Context

The rise in Japan's bond yields has catalyzed a reallocation of capital across asset classes and geographies. Investors are increasingly favoring U.S. dollar-hedged global government bonds, which offer higher returns and lower volatility compared to U.S.-only bond indices[2]. This trend reflects a broader normalization of bond yields, which has restored bonds' role as a core diversifier in portfolios[3].

In Japan, household investors are shifting away from cash holdings into equities and mutual funds to hedge against inflation[2]. The introduction of the Nippon Individual Savings Account (NISA) has further incentivized long-term equity investments, supporting Japanese stock prices[2]. Meanwhile, institutional investors are rebalancing portfolios: depository institutions are prioritizing interest income from core business, while life insurance companies are exploring higher-yield alternatives such as credit and alternative assets[2].

Globally, the surge in long-term JGB yields has prompted a reassessment of sovereign bond allocations. With Japan's fiscal sustainability under scrutiny, capital is flowing toward other developed and emerging markets offering better risk-adjusted returns[1]. This shift is mirrored in currency markets, where the yen's long-term depreciation could be offset by public pension funds' rebalancing of overseas holdings[2].

Looking Ahead: Strategic Considerations for Investors

As Japan navigates this period of transition, investors must remain agile. Active stock-picking, particularly in sectors poised to benefit from yen weakness (e.g., exporters), offers attractive opportunities[3]. Additionally, allocations to investment-grade and municipal bonds with shorter durations can mitigate interest rate risks[1]. For those seeking diversification, dollar-hedged global bonds and commodities may provide a buffer against equity volatility[3].

The BOJ's next moves will be critical. If the central bank signals a more aggressive normalization of policy, bond yields could rise further, pressuring fixed-income investors to adjust their strategies. Conversely, a continuation of the current cautious stance may prolong the yen's depreciation and fuel inflation, necessitating a shift toward inflation-protected assets.

In this evolving landscape, the rise in Japan's two-year bond yield is not merely a technical detail—it is a harbinger of broader policy shifts and a catalyst for global market reallocation. Investors who recognize these dynamics early will be better positioned to capitalize on the opportunities ahead.

Comentarios

Aún no hay comentarios