Reversal in Consumer Stocks: Is This the Bottom or a False Dip?

The recent rebound in consumer stocks has sparked a critical debate among investors: Is this a sustainable bottom in a late-stage bull market, or merely a temporary reprieve before a deeper correction? To answer this, we must dissect the interplay of sector rotation, valuation metrics, and macroeconomic signals.

Current Performance: A Mixed Picture

From Q1 2024 to Q3 2025, the Consumer Non Cyclical sector surged 20.58%, outpacing the Technology sector's 14.84% and Healthcare's 4.39% [1]. Meanwhile, Consumer Discretionary gained 12.62%, reflecting resilience in categories like dining and grocery delivery despite inflationary pressures [1]. This outperformance contrasts with the struggling Transportation and Energy sectors, which fell 3.00% and 0.59%, respectively [1]. However, the Consumer Staples sector, often a safe haven in late bull markets, has underperformed, with the Consumer Discretionary vs. Staples ratio (XLY:XLP) hitting multi-year highs [2].

Historical Sector Rotation: Lessons from Past Cycles

In late-stage bull markets, investors typically rotate from growth-oriented sectors (e.g., Technology, Discretionary) to defensive ones (e.g., Utilities, Staples) as economic uncertainty rises [3]. For example, during the 2008 financial crisis, healthcare and utilities outperformed as the market neared its peak [3]. Similarly, the 1990s tech boom saw a gradual shift to defensive sectors as growth decelerated [3].

Yet the 2024–2025 cycle defies this pattern. Instead of a migration to Staples, Discretionary has surged, suggesting a market still in expansion mode. This divergence could signal either a broadening bull market or a mispricing of risk. Analysts note that the current rally in Discretionary mirrors the 2009 market low, where a similar relative strength between Discretionary and Staples ETFs preceded a prolonged upturn [4].

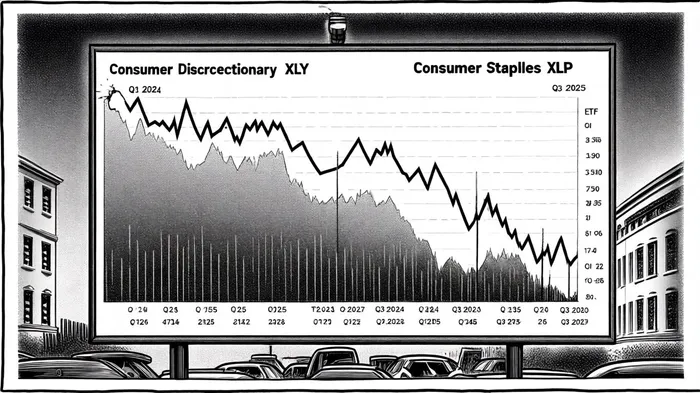

Market Timing Indicators: A Tale of Two Signals

Technical analysis reveals conflicting signals. The Consumer Discretionary Select Sector SPDR ETF (XLY) has outperformed the Consumer Staples Select Sector SPDR ETF (XLP) across large-cap, small-cap, and global markets, with relative strength reaching levels not seen since 2007 [2]. This suggests a "risk-on" environment, where investors are betting on resilient consumer demand.

However, broader economic indicators tell a different story. The inverted yield curve and elevated Fed Funds Effective Rate point to a bearish outlook, with potential market cooling on the horizon [4]. Additionally, J.P. Morgan data highlights building inflationary pressures in goods, which could erode real consumer spending [1]. These factors raise concerns that the current rally in Discretionary may be a false dip, masking underlying fragility.

Valuation Metrics: Discounts and Premiums

Analyst forecasts paint a nuanced picture. The Consumer Discretionary and Healthcare sectors trade at 15% and 13% discounts to fair value, respectively, making them attractive for long-term investors [5]. Conversely, growth stocks are at an 18% premium, a historically bearish sign [5]. Small-cap stocks, trading at a 17% discount, are also undervalued but may lag until monetary policy stabilizes [5].

The Consumer Staples sector, however, is nearing overvaluation, with valuations near the upper end of their historical range [2]. This suggests that while Staples may still offer defensive appeal, its upside is limited.

Conclusion: A Precarious Equilibrium

The reversal in consumer stocks appears to straddle the line between a sustainable bottom and a false dip. On one hand, the outperformance of Discretionary ETFs and undervaluation of key sectors suggest a market still in expansion. On the other, inverted yield curves and inflationary pressures hint at a late-stage correction.

For investors, the path forward hinges on balancing growth and defensive positions. Overweighting undervalued Discretionary and small-cap stocks could capitalize on a broadening bull market, while hedging with Staples and Utilities may protect against a potential downturn. As always, discipline and diversification remain paramount in navigating this precarious equilibrium.

Comentarios

Aún no hay comentarios