Here's Why You Should Retain AMN HealthCare Stock in Your Portfolio

AMN Healthcare Services, Inc. AMN is well-poised for growth in the coming quarters, courtesy of its broad array of services. The optimism is led by strong momentum in its Managed Services Program (MSP), rising labor disruption demand and investments in technology and AI-driven platforms. However, industry shifts, pricing pressure from healthcare consolidation and demand volatility following public health disruptions are major downsides.

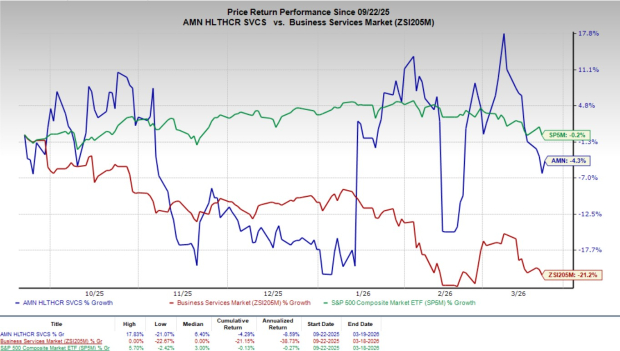

Shares of this Zacks Rank #3 (Hold) company have lost 4.3% in the past six months compared with the industry's 21.2% decline. The S&P 500 Index has also fallen 0.2% in the said timeframe.

This renowned player in the healthcare total talent services space has a market capitalization of $692.84 million. The company projects 44.1% earnings growth for 2026 and expects to witness continued improvements in its business. AMN HealthcareAMN-- surpassed the Zacks Consensus Estimate in all the trailing four quarters, delivering an average earnings surprise of 79.6%.

Image Source: Zacks Investment Research

Factors Favoring AMNAMN-- Stock

Healthcare MSP: AMN Healthcare’s Managed Services Program (MSP) continues to be a key driver of market traction, positioning the company as a strategic workforce partner rather than just a staffing provider. The platform streamlines workforce planning, centralizes contingent labor management and improves operational efficiency for healthcare systems, supporting better patient care delivery.

In 2025, MSP arrangements accounted for 48% of consolidated revenues, including 71% of Nurse and Allied, 18% of Physician and Leadership and 3% of Technology and Workforce Solutions segment revenues. The company managed around $1.8 billion in MSP spend, and when combined with vendor-neutral VMS programs, total spend under management reached $3.3 billion.

Management highlighted a robust and balanced sales pipeline, with increasing client demand for centralized workforce solutions and greater control over contingent labor spend. The company is gaining share in large, complex accounts and expanding within existing clients through cross-selling. These trends, along with new MSP wins expected to ramp up in the coming quarters, support sustained volume growth, stronger client retention and improved revenue visibility over time.

Labor Disruption Services Emerging as a Powerful Growth Driver: Labor disruption has rapidly emerged as a major near-term growth driver for AMN Healthcare. The company reported $124 million of labor disruption revenues in fourth-quarter 2025, nearly doubling year over year, and expects $600 million in first-quarter 2026 from multiple large, ongoing strike events. This business is supported by investments made over the past two years, including a dedicated strike team, specialized operating procedures and a technology-enabled event management system that serves as the backbone of its solution. These capabilities allow AMN to scale and manage large, simultaneous events while continuing to support its core business with minimal disruption.

The company sources clinicians from a mix of known crisis workers, new recruits, travelers, per diem staff and external suppliers, achieving very high fill rates. AI-enabled recruiting tools have improved both speed and efficiency in filling roles during these events. While this business carries lower gross margins, it provides strong operating leverage. AMN views this capability as a strategic differentiator that strengthens relationships with clients, ensures continuity of patient care and expands its clinician network for future opportunities.

Technology, AI and Platform Investments Driving Scalability: Multiyear investments in technology, automation and AI are transforming AMN’s operating model and long-term scalability. The company has deployed AI across recruiting, credentialing, analytics and workforce management to improve speed, efficiency and fill rates. These capabilities were tested during large-scale labor disruption events, where AMN successfully managed higher demand levels while maintaining service quality, reinforcing confidence in its platform.

In its Technology and Workforce Solutions segment, the company continues to enhance its offerings through advanced analytics, generative and agentic AI, and expanded workforce management capabilities, including support for internal float pools and internal agencies.

In language services, AMN is implementing a tiered service strategy to address pricing competition and is investing in AI to support administrative and non-clinical patient interactions while maintaining human interpreters for regulated clinical settings. Management expects these initiatives to drive margin improvement in the second half of the year and support a return to revenue growth.

Enhancements to its VMS platform (ShiftWise Flex), advanced analytics and automation capabilities are expanding its solution set and strengthening its competitive positioning.

These investments are expected to drive operating leverage, with management outlining a long-term framework of 4%-6% organic revenue growth and 10%-15% adjusted EBITDA growth. The company highlighted that AI is already proving accretive by improving recruiting efficiency and operational scalability and it expects these benefits to expand across the business over time.

Downsides of AMN Stock

Adverse Impacts From Public Health Crises: AMN Healthcare can be affected by public health crises such as pandemics. During COVID-19, demand was highly volatile — initially declining due to fewer elective procedures, then surging for staffing services before normalizing. Since then, demand has moderated, with fluctuations in bill rates and volumes, especially in the Nurse and Allied segment.

Future health crises could again disrupt demand patterns while also affecting workforce availability due to illness, quarantines or travel restrictions. These events can increase labor and operational costs and create uneven demand across service lines. Financial pressure on hospitals after such events may reduce spending on contingent labor, impacting AMN’s revenues and profitability.

Current expectations suggest limited growth in the near term, with some segments such as Physician & Leadership Solutions and Technology & Workforce Solutions facing potential revenue declines over the next few years.

Changing Marketplace Conditions: The healthcare industry is evolving rapidly with new care models such as telehealth, home healthcare and retail clinics, along with changing reimbursement structures and regulations. To remain competitive, AMN must adapt its services and invest in new technologies.

At the same time, advancements in AI and data analytics are helping healthcare providers improve internal staffing efficiency, which could reduce reliance on external staffing firms like AMN. The company also faces strong competition and failure to keep up with industry changes or client expectations could impact growth.

Regulatory changes and uncertainty may further influence hiring patterns and workforce strategies, adding another layer of complexity to the business environment.

Consolidation of Healthcare Delivery Units: Consolidation among healthcare providers is increasing their bargaining power, allowing them to negotiate lower prices for staffing services. It can also lead to client losses if merged organizations choose to work with existing vendors instead of AMN.

The growing use of vendor-neutral models and workforce platforms further shifts control toward clients, reducing direct relationships and increasing pricing pressure. In addition, AMN has some exposure to large clients, such as Kaiser Foundation Hospitals, which accounts for 22% of consolidated revenues, raising concentration risk. Currently, healthcare systems are investing more in internal staffing capabilities, which may reduce demand for external providers over time and put additional pressure on revenue growth and margins.

AMN Healthcare Services Inc Price

AMN Healthcare Services Inc price | AMN Healthcare Services Inc Quote

Estimate Trend

AMN Healthcare has been witnessing a positive estimate revision trend for 2026. Over the past 60 days, the Zacks Consensus Estimate for its earnings per share has improved 154.5% to $1.96.

The Zacks Consensus Estimate for first-quarter 2026 revenues and earnings per share is pegged at $1.23 billion and $1.64, respectively, suggesting 78.7% and 264.4% growth from the year-ago reported numbers.

Key Picks

Some better-ranked stocks in the broader medical space are Intuitive Surgical ISRG, Cardinal Health CAH and McKesson MCK. While Intuitive Surgical sports a Zacks Rank #1 (Strong Buy) at present, Cardinal Health and McKesson carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank stocks here.

Intuitive Surgical has an estimated long-term growth rate of 15.7%. ISRG's earnings surpassed estimates in each of the trailing four quarters, with the average being 13.2%.

Intuitive Surgical has gained 8% against the industry's 6.9% decline over the past six months.

Cardinal Health's earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 9.3%.

CAH's shares have rallied 43% in the past six months compared with the industry’s 14.9% growth.

McKesson's earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 3.6%.

MCK's shares have climbed 29% in the past six months compared with the industry’s 14.9% growth.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

McKesson Corporation (MCK): Free Stock Analysis Report

AMN Healthcare Services Inc (AMN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios