Repositioning in International Small-Cap Equities: Opportunities in a Post-Pandemic World

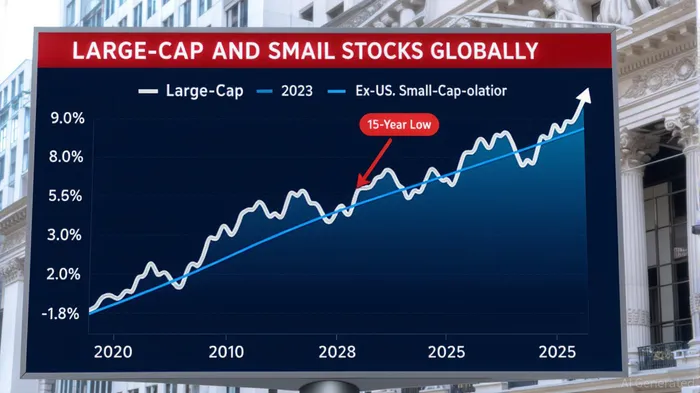

The post-pandemic era has reshaped global equity markets, creating a unique inflection point for international small-cap equities. These stocks, long undervalued relative to their large-cap counterparts, now trade at historically wide discounts—offering compelling entry points amid stabilizing macroeconomic conditions and sector-specific tailwinds. According to a report by T. Rowe Price, ex-U.S. small-cap stocks are currently trading at their cheapest valuations versus large-cap stocks in 15 years[1]. This dislocation, driven by pandemic-era disruptions, inflationary pressures, and interest rate volatility, has created an asymmetric opportunity for investors willing to navigate the inherent risks of smaller, less-liquid assets.

Macro-Driven Valuation Dislocation: A Catalyst for Rebalancing

The valuation gap between large and small caps has been exacerbated by macroeconomic forces. Rising interest rates in 2024 initially favored large-cap growth stocks, which dominate tech-heavy indices, while small-cap companies—often burdened with floating-rate debt—faced higher borrowing costs[2]. However, the anticipated easing of monetary policy, including Federal Reserve rate cuts in 2025, is expected to reverse this trend. Small-cap firms, which are more sensitive to rate changes, stand to benefit disproportionately from lower financing costs. As noted by American Century Investments, global small-cap earnings growth is projected to outpace large caps by 7 percentage points in 2025, with equal-weighted EPS growth estimated at 22% versus 15%[3].

Bottom-Up Fundamentals: Electrification, AI, and Reshoring

Beyond macro trends, bottom-up fundamentals are strengthening. The electrification and AI revolutions are creating fertile ground for small-cap innovation. For instance, companies like Modine Manufacturing (a provider of energy-efficient cooling solutions for data centers) and Capstone Copper (a copper producer critical for electrification infrastructure) are positioned to capitalize on surging demand for AI-driven data centers and renewable energy systems[4]. Similarly, European small-cap firms in industrials and materials are benefiting from reshoring initiatives, as highlighted by Janus Henderson's analysis of Germany's fiscal reforms and Japan's corporate governance improvements[5].

In the AI sector, niche players are outpacing giants by focusing on specialized applications. SoundHound AI, a non-U.S. small-cap, has secured partnerships with automotive brands like Lucid MotorsLCID-- and Alfa Romeo, leveraging voice recognition technology to enhance in-car experiences[6]. Meanwhile, BILL Holdings is using AI to streamline financial operations for small businesses, achieving 21.89% annual revenue growth[7]. These examples underscore the agility of small-cap firms in adapting to sector-specific disruptions.

Regional Opportunities and Risk Mitigation

Emerging markets and developed economies alike present opportunities. In India, small-cap firms are thriving due to supply chain diversification and favorable monetary policies[8]. Japan's small-cap stocks, trading at attractive price-to-book ratios, offer exposure to a reformed corporate landscape[9]. However, investors must remain cautious. Small-cap equities are inherently volatile, and earnings estimates for the sector have historically been prone to downward revisions—nearly 24% on average from 2011 to 2023[10].

Conclusion: A Strategic Case for Rebalancing

The confluence of macro-driven valuation dislocations and robust bottom-up fundamentals positions international small-cap equities as a strategic asset class for 2025. While risks such as regulatory uncertainty and economic volatility persist, the sector's historical mean reversion patterns and exposure to high-growth trends like AI and electrification make it a compelling addition to diversified portfolios. As central banks pivot toward accommodative policies, the time to reposition may be now.

Comentarios

Aún no hay comentarios