The Relevance of Dave Ramsey's Baby Steps in Modern Wealth Building

In an era where financial complexity and behavioral biases increasingly challenge wealth accumulation, Dave Ramsey's Baby Steps remain a polarizing yet influential framework. Designed to simplify personal finance through structured, incremental goals, the Baby Steps blend behavioral psychology with practical money management. This analysis evaluates their relevance in modern wealth building, focusing on their alignment with behavioral finance principles and their impact on long-term financial outcomes.

Behavioral Finance and the Psychology of Incremental Progress

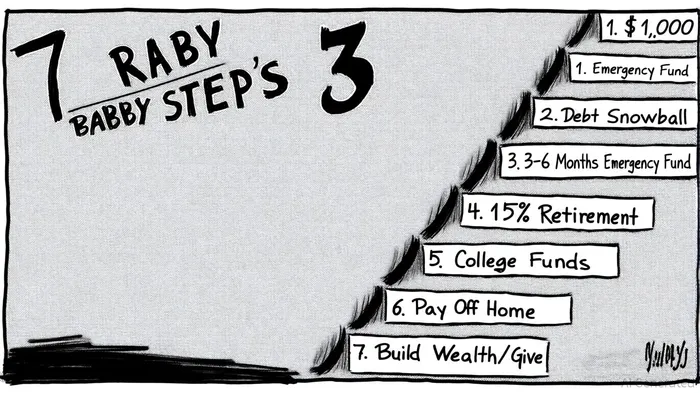

The Baby Steps' core strength lies in its behavioral design. The first step-saving $1,000 for a starter emergency fund-addresses the psychological barrier of "starting" by setting a low, achievable goal. This aligns with the behavioral finance concept of small wins theory, which posits that minor successes build confidence and momentum, fostering long-term commitment a Debt.org analysis. A 2024 Ramsey Solutions study found that Baby Steppers are 36 percentage points more likely to describe themselves as intentional with money compared to the general population, underscoring the plan's effectiveness in cultivating discipline (Ramsey Plan Comparison Study).

The second step, the debt snowball method, prioritizes paying off smaller debts first. While critics argue this approach may incur higher interest costs compared to the mathematically optimal debt avalanche method, behavioral finance research highlights its psychological advantages. The visibility of rapid progress-eliminating debts one by one-creates a positive feedback loop, reinforcing motivation and reducing procrastination a CFA's review. As noted in a 2025 analysis, this method leverages the human tendency to value immediate rewards over abstract long-term savings, making it a powerful tool for behavior change a 2025 analysis.

Long-Term Wealth Accumulation: Compounding and Investor Psychology

The Baby Steps' emphasis on emergency funds and debt elimination lays the groundwork for long-term wealth creation. By prioritizing financial stability before investing, the plan addresses a critical behavioral bias: loss aversion. Individuals who are debt-free and have a robust emergency fund (3–6 months of expenses) are less likely to liquidate investments during market downturns, a common reaction driven by fear a Stephatch guide. A 2024 comparison study revealed that Baby Steppers are 64% optimistic about their financial future versus 38% of the general population, suggesting improved emotional resilience (Redefining Normal: A Ramsey Plan Comparison Study).

However, the Baby Steps face scrutiny regarding retirement savings timing. Step 4 recommends investing 15% of household income into retirement accounts only after becoming debt-free. Critics argue this delays compounding, a cornerstone of wealth accumulation. For example, a 25-year-old who starts saving 15% at age 30 instead of 25 could miss out on over $100,000 in potential returns, assuming a 7% annual return a NewTraderU analysis. Yet, proponents counter that the plan's focus on eliminating high-interest debt first reduces the risk of reaccumulating debt during retirement, a trade-off that prioritizes behavioral sustainability over mathematical precision a Ramsey expert interview.

Critiques and Adaptability in a Complex Financial Landscape

The Baby Steps' one-size-fits-all approach has limitations in diverse financial contexts. For instance, the plan's rigid prioritization of college savings (Step 5) over retirement savings may conflict with evolving economic realities, such as rising student loan defaults and the declining value of traditional pensions an Insurance & Estates analysis. Additionally, the debt snowball method may not suit individuals with high-interest debts requiring immediate attention, such as medical bills or tax obligations, as Debt.org notes.

A 2025 analysis by a CFA highlighted these gaps, noting that while the Baby Steps excel in fostering discipline, they lack flexibility for nuanced scenarios like investment diversification or tax optimization (a CFA's review). Furthermore, the recommended 15% retirement savings target, while ambitious, assumes consistent income and market returns, which may not align with the realities of gig economy workers or those in volatile industries (a Stephatch guide).

Conclusion: Balancing Behavior and Strategy

Dave Ramsey's Baby Steps remain relevant in modern wealth building due to their focus on behavioral change-a domain where personal finance is 80% psychology and 20% math Under30CEO. By addressing procrastination, loss aversion, and the need for immediate feedback, the plan helps individuals overcome emotional barriers to financial success. However, its effectiveness in compounding wealth depends on adapting its principles to individual circumstances. For example, combining the debt snowball's motivational benefits with strategic debt prioritization (e.g., targeting high-interest debts) could optimize both behavior and outcomes.

As financial markets grow more complex, the Baby Steps serve as a foundational framework but should not be viewed as a universal solution. Investors must balance Ramsey's behavioral insights with personalized strategies that account for compounding, risk tolerance, and life goals. In this sense, the Baby Steps are not outdated but rather a starting point-a psychological scaffold for building more sophisticated wealth management practices.

Comentarios

Aún no hay comentarios