Reducing Geopolitical Exposure: A Deep Dive into Consumer Stocks with Minimal China Risk

In an era of escalating U.S.-China trade tensions and geopolitical volatility, investors are increasingly prioritizing supply chain resilience. The 2025 U.S. tariffs on Chinese goods-now at 20% for many products-have accelerated a global shift toward diversification, with companies rethinking decades of reliance on Chinese manufacturing, as an OptiLogic analysis shows. For the consumer sector, this transition is not merely a strategic adjustment but a survival imperative. As trade wars and regulatory uncertainties intensify, identifying stocks with minimal China exposure has become a cornerstone of portfolio defense.

The Geopolitical Landscape: Tariffs, Retaliation, and Resilience

The U.S. and China have engaged in a tit-for-tat escalation of tariffs since 2023, with the U.S. doubling its duties on Chinese imports to 20% in March 2025, a move the OptiLogic analysis documents. These measures have triggered retaliatory tariffs from China on U.S. exports, including natural gas, crude oil, and automobiles. The ripple effects are profound: production costs for U.S. companies have surged, with laptop prices projected to rise by 45% due to these tariffs. In response, firms like HPHPQ-- have committed to relocating 90% of North American production outside China by 2025, according to the OptiLogic piece.

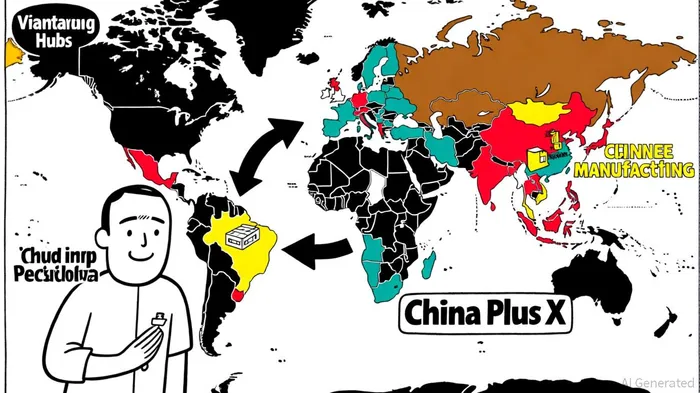

The "China Plus X" model-diversifying production across multiple countries-has emerged as a dominant strategy, a point underscored by a DHL analysis. Companies are now prioritizing geographic redundancy, investing in Vietnam, India, and Mexico to mitigate risks from geopolitical tensions, piracy, and extreme weather events. Vietnam, in particular, has attracted significant foreign direct investment (FDI) due to its trade agreements and infrastructure upgrades. This shift underscores a broader trend: by 2025, 43% of U.S. companies with operations in China had adjusted their sourcing strategies, the OptiLogic analysis found.

Identifying Low-Risk Consumer Stocks: The TD Cowen Framework

A 2025 TD Cowen survey categorized U.S. consumer stocks based on China revenue exposure, defining "low-risk" as companies with less than 10% of revenue derived from China, as reported in a USNewsPer report. These firms are better positioned to navigate trade disruptions and regulatory shifts. For example, Eli Lilly and Starbucks fall into this category. Both companies have demonstrated resilience by focusing on domestic markets and diversifying supply chains.

However, the survey also highlights the vulnerabilities of high-exposure firms. Nike, with 15% of revenue from China, and Estée Lauder, with 32% China sales, face declining consumer preference in the region as local brands like Li-Ning and Anta gain traction. This trend is compounded by China's economic slowdown and rising nationalism, which have eroded the appeal of Western brands.

Actionable Investment Examples: Beyond the High-Exposure List

While the research does not explicitly name all low-risk companies, it provides actionable insights. For instance, Synopsys (SNPS) and Cadence Design (CDNS), both in the electronic design automation (EDA) sector, derive the majority of their revenue from the U.S. market; these firms are less susceptible to geopolitical risks and are poised to benefit from the AI-driven growth of the EDA industry. Similarly, Apple and Tesla generate 16–21% of revenue from China, according to a Levelfields list, a figure that pales in comparison to the 25–35% exposure of fashion and luxury brands like Ralph Lauren and Tapestry.

The S&P 500 as a whole has 7% of its revenue tied to China, based on an Apollo Academy analysis, suggesting that sectors like consumer staples and utilities may offer additional low-exposure opportunities. Companies in these sectors, such as Procter & Gamble and Dow Inc., have historically prioritized regional production and supplier diversification.

Strategic Implications for Investors

The 2025 landscape demands a dual focus: mitigating geopolitical risk while capitalizing on supply chain innovation. Investors should prioritize companies that:

1. Diversify geographically: Firms leveraging the "China Plus X" model, such as HP and Walmart, are reducing single-point vulnerabilities, as noted in earlier analyses.

2. Leverage technology: Advanced analytics and digital twins are enabling real-time risk modeling, as seen in PepsiCo's supply chain strategies.

3. Avoid over-reliance on China: Even companies with minimal exposure must remain vigilant, as the U.S.-China relationship remains a wildcard.

Conclusion: A Portfolio for the New Normal

As trade tensions and geopolitical risks persist, the consumer sector's ability to adapt will define its success. By focusing on stocks with minimal China exposure-such as Eli Lilly, Starbucks, Synopsys, and Cadence-investors can build portfolios resilient to both macroeconomic and geopolitical shocks. The "China Plus X" strategy is not merely a response to tariffs; it is a blueprint for future-proofing supply chains in an increasingly fragmented world.

Comentarios

Aún no hay comentarios