Reassessing Canadian Manufacturing Exposure in a Post-Report Downturn

The Canadian manufacturing sector is at a crossroads. Recent data reveals a stark divergence in performance across subsectors, with Q3 2025 factory sales reflecting both resilience and fragility in the face of U.S. trade tensions. As investors reassess exposure, strategic reallocation and risk mitigation have become imperative.

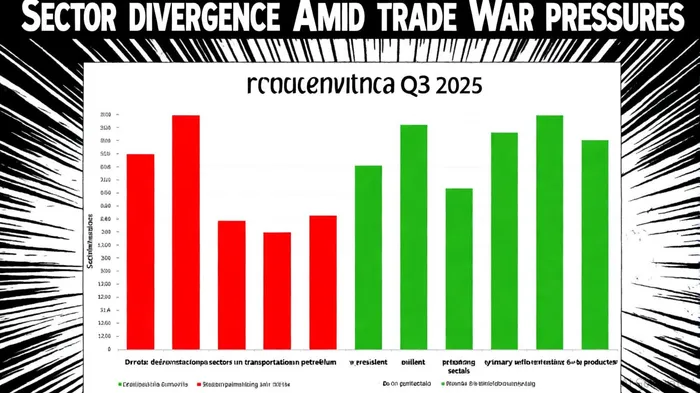

Sector-Specific Trends: Winners and Losers

The latest Statistics Canada data underscores a fragmented landscape. While primary metals-notably aluminum-surged by 45% in August 2025 despite U.S. tariffs, according to a Canadian Mortgage Trends report, transportation equipment and petroleum and coal products contracted sharply, contributing to a 0.8% monthly decline in factory sales, according to Trading Economics. This divergence highlights the need for granular analysis.

For instance, the food products subsector grew by 2.5% in August, suggesting demand stability in essential goods. Conversely, chemical products and transportation equipment led September's contraction, with the S&P Global Canada Manufacturing PMI slipping to 47.7-a sign of broad-based weakness reported in a CME blog post. These trends indicate that investors should prioritize sectors with pricing power and diversified demand, such as primary metals and food manufacturing, while avoiding overexposure to trade-sensitive industries.

Trade War Fallout: A Systemic Risk

The U.S. tariffs on steel, aluminum, and auto parts have created a ripple effect. Over 55% of Canadian manufacturers exporting to the U.S. anticipate operational challenges, according to the Statistics Canada survey, with 69.1% citing cost-related obstacles and 37.2% forecasting difficulties in accessing non-U.S. markets. Retaliatory tariffs have further exacerbated input costs, with 66% of businesses reporting supply chain disruptions.

A report by the Canadian Federation of Independent Business (CFIB) adds urgency: 31% of small manufacturers have absorbed tariff costs directly, while 28% delayed expansion plans. These dynamics suggest that trade tensions are not merely short-term headwinds but structural risks that could erode margins and deter capital investment.

Strategic Reallocation: Navigating the New Normal

Given this environment, investors should adopt a dual strategy: sector rotation and geographic diversification.

- Sector Rotation:

- Overweight resilient subsectors: Primary metals (e.g., aluminum) and food products have shown growth despite tariffs. Aluminum's 45% surge, for example, reflects strong global demand and potential for export diversification beyond the U.S.

Underweight trade-sensitive industries: Transportation equipment and petroleum face dual pressures from tariffs and cyclical demand shifts. The 6.5% Q2 decline in transportation equipment sales signals ongoing vulnerability.

Geographic Diversification:

- 33.6% of exporters are actively seeking alternative markets, a trend investors should mirror. Focusing on Asian and European markets-where demand for Canadian aluminum and machinery remains robust-could mitigate U.S. exposure.

- Currency hedging: With the Canadian dollar under pressure due to trade tensions, hedging strategies (e.g., forward contracts) can protect margins for exporters.

Risk Mitigation: Beyond Sector Shifts

Beyond reallocation, proactive risk management is critical.

- Supply chain resilience: Businesses must diversify suppliers to avoid bottlenecks caused by retaliatory tariffs. Investors should favor firms with agile supply chains or those leveraging nearshoring opportunities.

- Policy advocacy: Supporting policy reforms to reduce trade barriers-such as expedited free trade agreements with non-U.S. partners-could unlock long-term value.

Conclusion

The Canadian manufacturing sector's Q3 2025 performance underscores a pivotal moment for investors. While trade tensions have created headwinds, they also reveal opportunities in resilient subsectors and diversified markets. By reallocating capital to primary metals and food products, while hedging against trade-related risks, investors can position portfolios to weather-and potentially benefit from-the evolving landscape.

Comentarios

Aún no hay comentarios