Reasons to Add AngioDynamics Stock to Your Portfolio for Now

AngioDynamics ANGO has been gaining from its solid prospects with NanoKnife and an increased focus on cancer treatment markets. The optimism, led by a solid first-quarter fiscal 2026 performance, positive ongoing studies and a broad product line, bodes well for the stock.

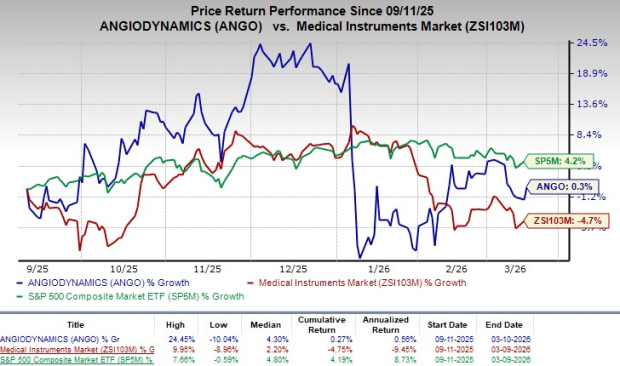

In the last six-month period, the Zacks Rank #1 (Strong Buy) company’s shares have gained 0.3% against the 4.7% decline of the industry. The S&P 500 has increased 4.2% during the said time frame.

The renowned designer, manufacturer and seller of an extensive range of innovative medical, surgical and diagnostic devices has a market capitalization of $444.3 million. The company projects 59.3% growth over the next year and expects to witness continued improvements in its business. AngioDynamics’ earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 82.1%.

Image Source: Zacks Investment Research

Reasons Favoring ANGO’s Growth

Broad Product Line: AngioDynamics reported a solid second-quarter fiscal 2026 performance, driven by strong momentum across its Med Tech platforms. The Auryon franchise remained the standout performer, generating $16.3 million in revenues, up 18.6% year over year, marking its 18th straight quarter of double-digit growth. Management highlighted continued share gains in the atherectomy market, supported by deeper hospital penetration, rising procedure volumes and improving procedure economics. Early international contributions following CE Mark approval also expanded Auryon’s addressable market and reinforced confidence in its long-term growth outlook.

The mechanical thrombectomy portfolio also advanced, with revenues increasing 3.9% year over year to $11 million. Growth was led by AlphaVac, which surged more than 40% as new hospital accounts were added and progressed through value analysis committees. Although AngioVac declined year over year due to a challenging prior-year comparison, it remained positive on a year-to-date basis, with management maintaining a favorable long-term outlook. Meanwhile, regulatory progress during the quarter, including IDE approvals and expanded FDA clearance, strengthened clinical utility and adoption potential, while the Med Device segment continued to provide steady support with 5.6% growth and consistent cash generation.

NanoKnife Driving Growth: During the second quarter of fiscal 2026, management highlighted continued strength in the NanoKnife franchise, with revenue increasing 22.2% year over year and probe sales rising 14.4%, driven primarily by growing adoption in prostate cancer procedures. The quarter marked a record period for prostate procedure volumes, reflecting rising physician interest as the CPT code for prostate ablation became effective on Jan. 1.

Management emphasized that adoption is progressing steadily rather than as an immediate step change, consistent with prior expectations. Capital sales were supported in part by an international distribution transition in France, though leadership stressed that underlying demand is being driven by procedural growth and increasing clinical utilization. Overall, NanoKnife remains well-positioned to benefit from expanding awareness, improving reimbursement clarity and sustained physician engagement in the prostate cancer market.

Solid Q2 Results: AngioDynamics delivered a strong fiscal second-quarter 2026, with revenue rising 8.8% year over year to $79.4 million, reflecting solid execution across both operating segments. Growth was led by the higher-margin Med Tech portfolio, which increased 13% and now accounts for 45% of total revenues, underscoring the company’s ongoing mix shift toward faster-growing platforms. Improved product mix, manufacturing optimization initiatives and pricing actions drove gross margin expansion of 170 basis points to 56.4%.

A Factor That May Offset ANGO’s Gains

Macroeconomic Concerns: Per the earnings call, management noted that tariff-related expenses in the second quarter of fiscal 2026 were in line with expectations and reaffirmed its projection of $4–$6 million in tariff costs for the full fiscal year. Although anticipated, these costs remain a structural margin headwind that is expected to weigh on performance through the rest of the year.

While gross margin expanded year over year, management clarified that the improvement was largely driven by pricing actions, intensified cost-control measures and a favorable shift toward higher-margin Med Tech products, rather than any relief from external cost pressures.

Estimate Trend

AngioDynamics has been witnessing a stable estimate revision trend for fiscal 2026. Over the past 30 days, the Zacks Consensus Estimate for loss has remained stable at 27 cents per share.

The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is pegged at $77.4 million, implying a 7.5% rise from the year-ago reported number. The consensus mark for fiscal third-quarter loss per share is pinned at 11 cents, implying a 466.7% decline year over year.

Other Key Picks

Some other top-ranked stocks in the broader medical space are Intuitive Surgical ISRG, Phibro Animal Health PAHC and Cardinal Health CAH.

Intuitive Surgical, sporting a Zacks Rank #1 at present, reported fourth-quarter 2025 adjusted earnings per share (EPS) of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ISRG has an estimated long-term earnings growth rate of 15.7% compared with the industry’s 14% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 13.2%.

Phibro Animal Health, currently sporting a Zacks Rank #1, reported fiscal second-quarter 2025 adjusted EPS of 87 cents, which surpassed the Zacks Consensus Estimate by 26.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%.

PAHC has an estimated long-term earnings growth rate of 21.5% compared with the industry’s 12.6% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 20.1%.

Cardinal Health, currently carrying a Zacks Rank #2 (Buy), reported second-quarter fiscal 2026 adjusted EPS of $2.63, which surpassed the Zacks Consensus Estimate by 10%. Revenues of $65.6 billion beat the Zacks Consensus Estimate by 0.9%.

CAH has an estimated long-term earnings growth rate of 15% compared with the industry’s 9.1% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 9.3%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AngioDynamics, Inc. (ANGO): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios