The New Reality: Why US Treasuries Are No Longer Safe and What to Do About It

The U.S. Treasury market, long the bedrock of global financial safety, is undergoing a seismic shift. A perfect storm of record debt, soaring interest costs, and geopolitical instability is eroding its hedging power. Investors who cling to long-term Treasuries are increasingly vulnerable, while alternatives like short-duration bonds, safe-haven currencies (JPY/CHF), and gold offer superior risk-adjusted returns. Here's why the playbook must change—and how to adapt.

The Erosion of Treasury's Hedge Power

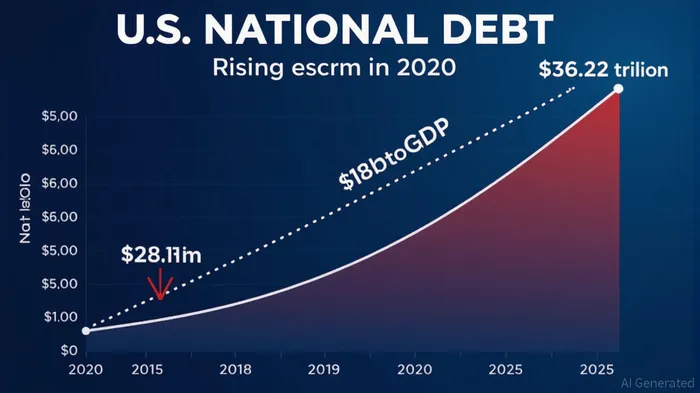

The U.S. national debt has surged to $36.22 trillion, with annual interest payments now consuming 13.55% of federal outlays in 2025. The Congressional Budget Office warns that interest costs could hit $1.8 trillion annually by 2035, surpassing historical highs as a share of GDP. This structural burden undermines Treasury's role as a risk-free asset:

- Debt Dynamics: The debt-to-GDP ratio has exceeded 100% since 2013 and is projected to hit 156% by 2055, per the CBO. Such levels strain fiscal flexibility, leaving the U.S. vulnerable to inflation spikes, rate hikes, or a loss of investor confidence.

- Interest Rate Sensitivity: Long Treasuries face relentless duration risk. A 10-year bond's price drops 10% for every 1% rate rise—a stark reality as the Fed's policy rate remains near 4.5% with no clear path to cuts.

- Geopolitical Risks: Tensions with China, energy market volatility, and a potential debt ceiling crisis amplify uncertainty. The Treasury market, once a haven during crises, now struggles to absorb these shocks.

Why Long-Term Treasuries Failed in 2022—and Still Pose Risks

The 2022 crisis was a watershed moment. Long Treasuries (e.g., 30-year bonds) lost 39.2%—their worst year on record—due to aggressive Fed rate hikes and inflation fears. Even now, their recovery is fragile:

- Duration Risk: A bond fund with a 15-year duration could lose 15% for every 1% rate rise. With yields near 4.5%, further hikes or inflation surprises could trigger fresh declines.

- Low Income vs. Risk: While 10-year yields offer 4.5% income, this barely offsets the risk of capital losses. Meanwhile, short-term bonds deliver similar yields with far less volatility.

The data is clear: long Treasuries are no longer a reliable hedge against downside risks.

The Case for Alternatives: Short-Term Bonds, JPY/CHF, and Gold

To navigate this new landscape, investors must reallocate to assets that thrive in high-debt, volatile environments. Here's the empirical evidence:

1. Short-Term Bonds: The New Cash Equivalent

- Performance: Short-term Treasuries (0–3 years) and bills held up during 2022's turmoil, offering yields of 4.5%–5% with minimal price swings. Their low duration shields investors from rate shocks.

- Data: The ICE BofA 0–1 Year Gilt Index outperformed long-term benchmarks since 1998, with a Sharpe Ratio of 2.1 vs. -0.5 for long Treasuries post-2022.

2. JPY/CHF: Safe-Haven Currencies with Carry Benefits

- JPY: The yen's inverse relationship with U.S. rates and its role as a funding currency in carry trades makes it a buffer against dollar volatility. While yields are low, its stability in crises (e.g., during 2023's bank runs) justifies its place in portfolios.

- CHF: Switzerland's central bank raised rates to 2.25% in 2024, bolstering CHF's appeal. A trading strategy on CHFJPY since 2023 delivered a 3.51% CAGR with a Sharpe Ratio of 8.31%, outperforming Treasuries.

3. Gold: The Ultimate Non-Government Liability

- 2025 Surge: Gold rose 30% year-to-date in 2025, reaching $3,403/oz, as central banks bought $1,100 billion in 2024–2025. Unlike Treasuries, it has no counterparty risk.

- Risk-Adjusted Outperformance: Gold's Sharpe Ratio of 1.8 since 2023 beats long Treasuries' -0.7, while its correlation with equities remains negative, enhancing diversification.

Investment Strategies for the New Reality

The fiscal and macro risks are structural, not cyclical. Here's how to reallocate:

- Reduce Long-Term Treasury Exposure: Cap allocations to maturities <5 years. Avoid 10+ year bonds unless yields hit 5%+.

- Add Short-Term Bonds: Allocate 30–40% of fixed-income holdings to ETFs like SHY (0–1 year Treasuries) or BIL (T-bills).

- Go Global with JPY/CHF: Use currency ETFs like FXY (JPY) or FXF (CHF) for 5–10% of assets. Pair with carry trades if volatility subsides.

- Hoard Gold: Allocate 5–10% to physical gold or ETFs like GLD. Central bank demand and inflation protection justify this.

Conclusion: Adapt or Be Left Behind

The era of Treasury dominance is over. With debt at $36 trillion and interest costs spiraling, investors must embrace alternatives to avoid losses. Short-term bonds, JPY/CHF, and gold offer a safer, higher-return path. The data is clear: clinging to long Treasuries risks exposure to fiscal and policy failures. The time to revise portfolios is now—or risk paying a steep price later.

Act swiftly, diversify strategically, and prioritize assets that thrive in this new fiscal reality.

Comentarios

Aún no hay comentarios