RAVE Restaurant Group: Assessing Revenue Growth and Margin Expansion Potential in a Competitive Market

RAVE Restaurant Group (RAVRF) operates in a fragmented but competitive quick-service restaurant (QSR) sector, with its two flagship brands—Pizza Inn and Pie Five—facing challenges from shifting consumer preferences and economic headwinds. This analysis evaluates the company's financial performance, focusing on revenue growth and margin expansion potential, while addressing critical discrepancies in reported data.

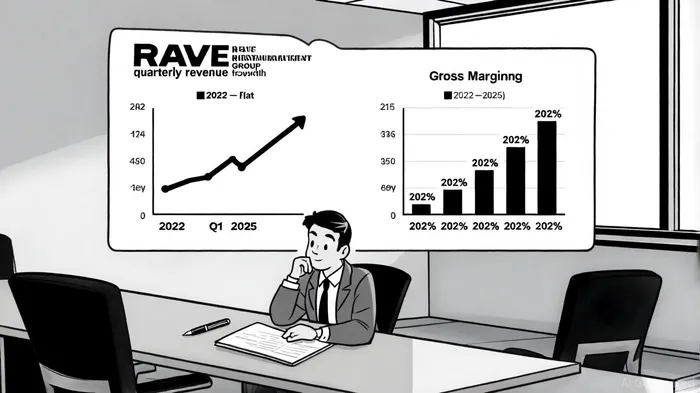

Revenue Trends: Stability Amid Stagnation

RAVE's quarterly revenue has remained relatively flat at approximately $3.0 million since 2022, with only modest annual growth. For instance, total revenue increased from $11.89 million in 2023 to $12.24 million in the trailing 12 months ending March 30, 2025, reflecting a 2.2% year-over-year growth rate[1]. However, Q4 2025 results revealed a 6.0% decline in revenue to $3.2 million compared to the prior year, driven by a 7.2% drop in Pie Five's domestic comparable store sales[2].

The company's strategic focus on value-driven promotions, such as the “I ate at Pizza Inn” $8 buffet deal, has yielded mixed results. While Pizza Inn's domestic comparable sales rose 6.3% in Q4 2025, Pie Five's performance underscored structural challenges in the brand's appeal[3]. This divergence highlights the importance of brand-specific strategies in driving revenue growth.

Gross Margin Volatility and the 100% Anomaly

RAVE's gross margin trends present a paradox. Historical data from Macrotrends and GuruFocus indicate a gradual improvement, with margins rising from 66.67% in 2022 to 74.11% in Q1 2025[4]. However, Q4 2025 results reported a 100% gross margin—a figure that defies conventional accounting logic for a restaurant operator[5]. A 100% margin would imply zero cost of goods sold (COGS), which is implausible given the company's operational model.

This discrepancy raises red flags. SEC filings for Q4 2025, including the 10-Q and 8-K, do not mention a 100% gross margin, instead focusing on net income, revenue, and EBITDA metrics[6]. The absence of COGS details in these filings suggests either a reporting error or a non-standard accounting practice. For context, RAVE's 10-K for fiscal 2025 breaks down revenue by segment (e.g., franchise royalties at 39.87% of total revenue) but omits gross margin specifics[7].

Margin Expansion Potential: Caution and Opportunity

Despite the Q4 anomaly, RAVE's long-term gross margin trajectory appears positive. From 2021 to 2025, margins have oscillated between 66.67% and 75.00%, outperforming the industry median of 46.235%[8]. This resilience likely stems from cost-control measures and franchise royalty structures, which reduce direct operational costs. However, the 100% margin figure—if authentic—would represent an extraordinary outlier, potentially masking underlying inefficiencies or misclassifications of expenses[9].

Investors should prioritize clarity on this issue. A 100% margin would either signal exceptional operational efficiency (unlikely for a QSR) or an accounting misstep. Until RAVERAVE-- provides a detailed explanation or correction, margin expansion assumptions should be treated with caution.

Strategic Outlook: Balancing Innovation and Execution

RAVE's recent initiatives, such as the Pizza Inn value promotion, demonstrate a willingness to adapt to market conditions. The promotion drove a 30.6% year-over-year sales lift in participating locations, illustrating the power of targeted pricing strategies[10]. However, the company's ability to sustain growth hinges on broader factors:

1. Brand Revitalization: Pie Five's declining sales underscore the need for a repositioning strategy.

2. International Expansion: With 22 international Pizza Inn units as of Q4 2025, geographic diversification could offset domestic stagnation[11].

3. Cost Management: Maintaining gross margins above 70% will require disciplined supply chain management and menu pricing.

Conclusion: A Cautious Case for Long-Term Investors

RAVE Restaurant Group's financial performance reflects a company navigating a challenging QSR landscape. While revenue growth remains tepid and margin data inconsistent, strategic innovations and a strong franchise model offer a foundation for future expansion. Investors should monitor the company's response to the Q4 2025 margin discrepancy and its ability to execute brand-specific strategies. For now, RAVE appears more as a speculative play than a core holding, with its potential tied to operational transparency and brand revitalization.

Comentarios

Aún no hay comentarios