U.S. Rare Earth Mining Stocks: Navigating Volatility in a Geopolitically Charged Market

The U.S. rare earth mining sector in 2025 has become a microcosm of the broader tension between geopolitical strategy and market fundamentals. Driven by China's export restrictions, U.S. government interventions, and the global push for clean energy, rare earth stocks have swung between euphoria and caution. For investors, the challenge lies in discerning cyclical opportunities from structural risks in a market where policy and politics often override traditional supply-demand dynamics.

Geopolitical Catalysts and Market Volatility

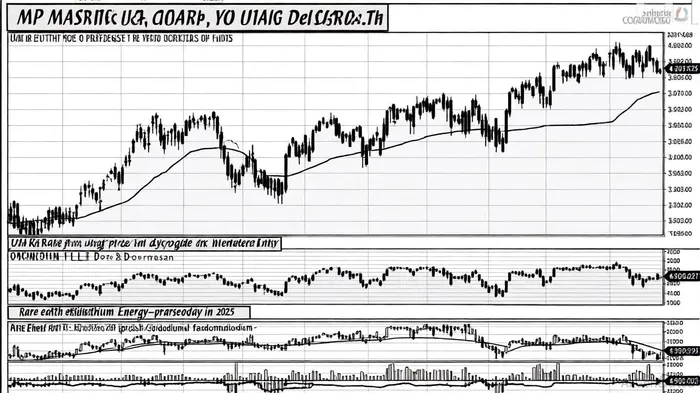

The recent 94% surge in USA Rare EarthUSAR-- (USAR) shares over five weeks underscores the sector's sensitivity to geopolitical narratives. Speculation about potential White House partnerships and a $100 million acquisition of U.K.-based Less Common Metals fueled this rally, even as the company remains pre-revenue and reports widening losses, as noted in a FinancialContent article. Similarly, MP MaterialsMP-- (MP) and Energy FuelsUUUU-- (UUUU) have benefited from U.S. efforts to counter China's dominance, including a $400 million Department of Defense investment in MP and a 15% equity stake in Lithium Americas, according to a Rare Earth Exchanges analysis.

China's export controls on seven rare earth elements-critical for defense and clean energy technologies-have further amplified volatility. According to a CNBC report, these restrictions expose U.S. supply chains to disruption, as domestic heavy rare earth separation remains nascent. While this has driven short-term gains for U.S. producers, it also highlights the sector's reliance on geopolitical contingencies rather than stable market conditions.

Cyclical Risks and Correction Pressures

Despite strategic tailwinds, the rare earth sector remains cyclical and prone to corrections. Prices for key elements like dysprosium oxide and terbium oxide fell by 33% and 22%, respectively, in 2024, reflecting oversupply and weak demand, according to a Fastmarkets report. Industry experts warn of a "tough second quarter" in 2025 as inventories from 2023–2024 are liquidated, and the Fastmarkets analysis adds further context. Light rare earths (e.g., neodymium-praseodymium) have held up better due to production cost floors, but medium-to-heavy rare earths face declining prices amid softer demand for high-performance magnets, as AgMetalMiner notes.

The sector's vulnerability is compounded by permitting delays, high capital costs for refining infrastructure, and regulatory uncertainties. For instance, USA Rare Earth's Round Top mine in Texas and Stillwater magnet facility in Oklahoma represent long-term bets, but their profitability hinges on sustained government support and workforce development, according to a Global Affairs report. Without off-take agreements or subsidies, even strategically vital projects may struggle to attract private capital.

Strategic Opportunities and ESG Considerations

Investors seeking to navigate this volatility must balance geopolitical momentum with financial pragmatism. Companies emphasizing sustainable practices, such as Lynas Rare Earths and Vital Metals, may attract ESG-conscious capital, though their growth trajectories remain unproven, as highlighted in a Rare Earth Exchanges list. Meanwhile, the U.S. government's growing equity stakes in firms like MP Materials and Trilogy Metals signal a shift toward industrial policy, potentially stabilizing returns for politically aligned players, a Bloomberg analysis suggests.

However, overreliance on government support carries risks. A Rare Earth Exchanges insight notes that U.S. rare earth refining capacity remains heavily dependent on China, with 85% of global refining controlled by Beijing. This creates a paradox: while policy aims to reduce reliance on China, the sector's immediate survival may still depend on it.

Investment Implications

For cyclical investors, timing is critical. Argus Media forecasts a gradual recovery in dysprosium prices by 2026 as inventories normalize and clean energy demand accelerates, according to a Global Mining Review article. Yet, short-term corrections could deepen if geopolitical tensions ease or China reverses its export restrictions. A diversified approach-balancing pre-revenue innovators like USARUSAR-- with more established players like MP-may mitigate downside risks.

Conclusion

The U.S. rare earth sector embodies the intersection of industrial strategy and market forces. While geopolitical tailwinds have created compelling narratives for stocks like USAR and MP, investors must remain vigilant about cyclical corrections and structural bottlenecks. Success will depend not only on political will but also on the sector's ability to scale refining capacity, reduce costs, and align with global decarbonization goals. For now, the path forward remains as volatile as the elements themselves.

Comentarios

Aún no hay comentarios