Quoin Pharmaceuticals' $104.5M Private Placement: A Strategic Bet in a Shifting Biopharma Landscape

In the high-stakes world of biopharmaceuticals, where innovation and capital are inextricably linked, QuoinQNRX-- Pharmaceuticals' $104.5 million private placement represents both a calculated gamble and a reflection of broader industry dynamics. As the sector grapples with macroeconomic headwinds, regulatory uncertainties, and the relentless pressure to deliver late-stage breakthroughs, Quoin's move underscores the delicate balance between securing growth capital and managing investor skepticism.

Strategic Rationale: Funding the Future, With Warrants as a Hedge

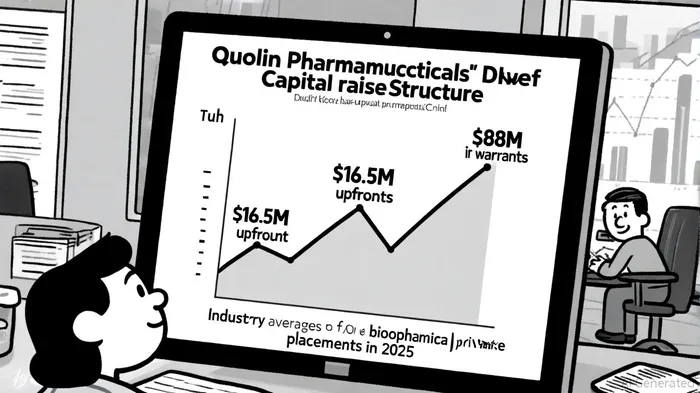

Quoin's financing structure-a blend of upfront capital and deferred proceeds via warrants-exemplifies the nuanced strategies biopharma firms are adopting in 2025. The company is issuing 1,993,940 American Depository Shares (ADSs) and warrants to purchase up to 7,975,760 additional ADSs at prices ranging from $9.075 to $12.375 per share, all priced at a premium to its prior stock price, according to a GlobeNewswire release. This approach allows Quoin to lock in immediate liquidity for its QRX003 clinical trials for Netherton Syndrome while deferring potential dilution until future milestones-such as regulatory approvals or positive trial data-justify higher valuation multiples.

The decision aligns with industry trends. According to a Morgan Stanley report, biopharma companies are increasingly prioritizing capital efficiency, leveraging warrant structures to align investor incentives with long-term value creation. For Quoin, the upfront $16.5 million will fund corporate operations through 2027, a critical window for advancing QRX003, while the warrants provide a "flexible runway" to scale further without immediate share issuance, according to QuiverQuant.

Investor Implications: Premium Pricing vs. Dilution Risks

The participation of healthcare-focused institutional investors like AIGH Capital and Soleus Capital signals confidence in Quoin's pipeline and management. However, the warrant-heavy structure introduces a double-edged sword. If the company's stock price surges post-issuance, warrant exercises could dilute existing shareholders. Conversely, if Quoin underperforms, the warrants may expire worthless, leaving investors with limited upside.

This tension mirrors broader investor behavior in 2025. As noted in McKinsey's analysis, biopharma investors are increasingly favoring later-stage assets with clearer pathways to commercialization, given the high costs and risks of early-stage R&D. Quoin's focus on Netherton Syndrome-a rare, severe skin condition with limited treatment options-positions it to tap into niche markets with premium pricing potential, a strategy that resonates in an era of patent expirations and pricing pressures.

Industry Context: Capital Access and the AI-Driven Rebound

Quoin's raise also reflects the sector's evolving capital landscape. With interest rate cuts anticipated by the Federal Reserve, biopharma firms are cautiously optimistic about reduced borrowing costs and renewed investor appetite, as noted in a Pharmaphorum piece. However, the Inflation Reduction Act and geopolitical uncertainties continue to cloud long-term revenue projections, pushing companies to prioritize near-term cash flow and operational efficiency, according to EY's 2025 report.

Notably, Quoin's financing coincides with a shift toward AI-driven drug discovery, which is compressing R&D timelines and costs. According to Deloitte, 87% of biopharma alliances in 2025 now involve AI platforms, enabling firms to de-risk pipelines and attract capital. While Quoin has not explicitly tied its raise to AI, its QRX003 program likely benefits from computational tools that enhance target identification and trial design.

The Road Ahead: Balancing Ambition and Prudence

For investors, Quoin's private placement raises critical questions: Can the company advance QRX003 through Phase III trials within its projected timeline? Will the warrants be exercised, and at what cost to existing shareholders? And how does Quoin's strategy compare to peers navigating similar challenges?

The answers will hinge on execution. As EY's 2025 Biotech Beyond Borders Report emphasizes, biopharma firms that align capital allocation with long-term innovation goals-while maintaining agile supply chains and transparent communication-are best positioned to thrive. Quoin's raise, if managed prudently, could serve as a blueprint for balancing aggressive growth with investor trust in an increasingly capital-constrained world.

Comentarios

Aún no hay comentarios