Quince Therapeutics: Navigating Earnings Setbacks While Building a High-Stakes Biotech Play

The Science of Resilience: Safety Milestones and Strategic Timing

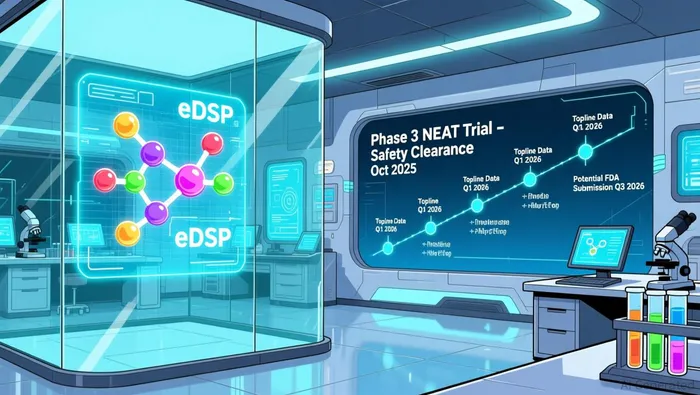

Quince's core asset, encapsulated dexamethasone sodium phosphate (eDSP), is advancing through its Phase 3 NEAT trial for Ataxia Telangiectasia (A-T), a rare neurological disorder with no approved therapies. A critical inflection point came in October 2025, when an independent data and safety monitoring board (iDSMB) confirmed the trial's favorable safety profile, allowing it to proceed without modifications, according to a Press release. This validation, as emphasized by CEO/CMO Dirk Thye, M.D., reinforces investor confidence in the therapy's risk-reward balance and aligns with regulatory expectations for a potential first-to-market treatment, per the Press release.

Analyst Optimism: Price Targets and the Path to Value Creation

Despite the earnings miss, analysts remain bullish. As of Q4 2025, three firms-Oppenheimer, Maxim Group, and another unnamed firm-have set average price targets of $8.00 for QNCXQNCX--, implying a 412% upside from its current $1.56 level, as cited in a Tipranks forecast. This optimism hinges on two factors: the potential approval of eDSP for A-T and the company's ability to secure additional financing through warrant exercises, which could extend its cash runway into the second half of 2026, as noted in the Seeking Alpha report.

The disconnect between Quince's financials and its price targets reflects a broader theme in biotech investing: the premium placed on clinical progress over near-term profitability. While the company's burn rate and lack of revenue remain risks, the iDSMB's endorsement and the rarity of A-T (estimated to affect 1 in 1 million individuals) position eDSP as a niche blockbuster candidate.

Risks and Realities: A Balanced Perspective

Investors must weigh several risks. The Phase 3 trial, though on track, still faces the inherent uncertainties of clinical development. Additionally, Quince's reliance on warrant financing introduces volatility-if investors fail to exercise these instruments, the company may need to raise capital at a discount, diluting existing shareholders. However, the current cash runway through mid-2026 provides a buffer, allowing the stock to trade on optimism without immediate liquidity pressure, as noted in the Seeking Alpha report.

Conclusion: A High-Variance Bet with Asymmetric Potential

Quince Therapeutics exemplifies the duality of biotech investing: a stock that combines the drag of operational losses with the allure of transformative milestones. For investors with a multi-year horizon and a tolerance for volatility, the favorable safety review and analyst price targets suggest that the company's long-term potential may outweigh its short-term challenges. As the NEAT trial approaches its topline readout in early 2026, QNCX could transition from a speculative play to a validated therapeutic contender-provided it navigates the final stretch of its clinical journey without misstep.

Comentarios

Aún no hay comentarios