Quanta Trades at a Premium: Should Investors Buy the Stock or Fold?

Quanta Services, Inc. PWR is currently trading at a premium compared with the Zacks Engineering - R and D Services industry, the broader Zacks Construction sector and the S&P 500 Index, with a forward 12-month price-to-earnings (P/E) ratio of 41.21. The industry’s average currently is 24.78, with the sector’s valuation at 19.37 and the S&P 500 Index at 20.74.

The overvaluation of PWRPWR-- stock stems from the multi-decade power demand trends driven by electrification, AI and data center growth, with the growing project pipeline substantiating the point. Besides, the company’s efforts to generate strong cash flow and report double-digit growth across its key metrics lay a solid foundation for investors to view QuantaPWR-- as a long-term infrastructure compounder.

However, with the stock already trading significantly higher than its industry and sector, any signs of market slowdown or in-house execution mishaps could put it at risk of reduced valuation and growth prospects. Such a scenario would be discouraging for the investors, as the ongoing heightened optimism could make the stock vulnerable if growth or execution disappoints.

Image Source: Zacks Investment Research

Shares of this specialty contracting services provider have gained 31.6% year to date, outperforming the industry, the sector and the S&P 500 Index, as evidenced by the chart below.

Image Source: Zacks Investment Research

What’s Pulling Up Quanta’s Growth Prospects?

Growing AI & Data Center Opportunities: Surging AI-related power demand and expanding utility investments are elevating data center-related project opportunities, making it a central pillar of Quanta’s long-term growth strategy. The rapid expansion of AI workloads is driving unprecedented electricity demand, requiring large-scale upgrades to transmission, substations and load-center infrastructure.

Besides, strategic acquisitions, including Tri-City and Wilson, further enhance Quanta’s ability to execute complex projects tied to load centers and high-voltage transmission, both critical components of data center ecosystems. These investments expand its skilled labor base and strengthen its competitive positioning in a capacity-constrained market. Moreover, the company’s integrated capabilities, from engineering and construction to maintenance, enable it to capture value across the entire power delivery chain, making it a preferred partner for hyperscalers and utilities alike.

Growing Project Pipeline: As of Dec. 31, 2025, Quanta’s total backlog reached $43.98 billion, up 27.3% year over year, with 12-month backlog growing to $25.87 billion from $19.77 billion a year ago. The increase reflects accelerating demand in the Electric Infrastructure Solutions segment, solid activity across end markets and momentum heading into 2026. Management highlighted that a growing portion of this backlog is tied to long-term, programmatic agreements rather than shorter-cycle projects, enhancing revenue visibility and reducing volatility.

PWR also indicated that large projects not yet in backlog, such as upcoming transmission work and the new power generation program, are expected to add further volume once permitting milestones are met. This supports long-term revenue visibility and strengthens the company’s outlook for sustained growth. Furthermore, it believes there is an opportunity to achieve record backlog levels again in 2026 and future years, supported by a pipeline of activity, and plans to provide complete solutions for multi-year programs.

Strong 2026 Outlook: The financial view of PWR into 2026 is an optimism booster, given the current growth momentum of the stock. In 2026, the company expects revenues between $33.25 billion and $33.75 billion, reflecting growth from $28.48 billion reported in 2025, with adjusted EPS projected between $12.65 and $13.35 (up from $10.75 reported in 2025). It also expects adjusted EBITDA between $3.34 billion and $3.50 billion (up from $2.88 billion reported in 2025) and operating cash flow between $2.30 billion and $2.85 billion (up from $2.23 reported in 2025). Record backlog, continued utility spending and anticipated contributions from recent acquisitions are what back Quanta’s expectation for this year.

Earnings Estimate Revision of PWR

PWR’s earnings estimates for 2026 and 2027 have trended upward in the past 60 days to $12.94 per share and $15.33 per share, respectively. The estimates for 2026 and 2027 imply year-over-year growth of 20.4% and 18.4%, respectively.

Image Source: Zacks Investment Research

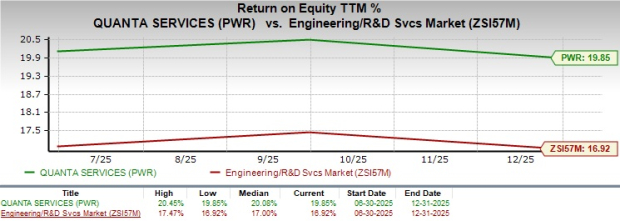

ROE of PWR Stock

Quanta’s trailing 12-month return on equity (ROE) of 19.85% significantly exceeds the industry’s average, underscoring its efficiency in generating shareholder returns.

Image Source: Zacks Investment Research

Quanta vs. Other Market Players

Quanta is well-positioned to benefit from rising AI-driven infrastructure demand, alongside big names including MasTec, Inc. MTZ, AECOM ACM and Fluor Corporation FLR. However, their exposure and competitive positioning differ significantly across the value chain.

MasTec participates in AI demand through power delivery, communications and renewable energy projects. It benefits from data center-driven grid expansion and broadband needs, but its exposure is more diversified and includes higher-risk segments like pipelines and renewables, which can introduce earnings volatility despite strong backlog growth. Conversely, AECOM plays a more indirect role, focusing on design, consulting and program management for infrastructure projects. While AI-driven demand supports its transportation, energy and environmental backlog, its competitive strength lies in high-margin advisory services and global reach rather than execution of power infrastructure itself.

On the other hand, Fluor is positioned as an EPC contractor capturing large-scale data center builds globally. The company sees data centers as a major growth opportunity, driven by AI and cloud expansion, with rising project pipelines across the U.S. and international markets. However, its exposure remains project-based and tied to cyclical capital spending.

Overall, PWR leads in power-driven monetization of AI demand, MasTec offers diversified infrastructure exposure, Fluor captures construction upside from hyperscale builds and AECOM benefits through advisory roles, highlighting complementary yet distinct approaches to the evolving market.

Hurdles to Quanta’s Growth

Macro Concerns: Quanta is operating in an uncertain macro environment despite witnessing robust public infrastructure demand trends. Higher interest rates, geopolitical tensions and energy price volatility continue to create an unpredictable business environment. These factors can delay capital spending by customers and slow construction activity across several end markets. The company’s revenue growth depends heavily on the timing and funding of new project awards.

Execution Risks: Quanta faces execution risks primarily tied to its large, complex infrastructure projects, which are vulnerable to delays, cost overruns and scope changes. Fixed-price contracts expose margins to inflation in labor and materials. Supply-chain bottlenecks and shortages of skilled craft labor can disrupt timelines and increase costs. Additionally, weather disruptions and operational challenges add uncertainty. Frequent acquisitions introduce integration risks, while rising project complexity limits margin expansion. Overall, PWR’s ability to convert its record backlog into profitable, timely execution remains its most critical operational challenge.

Does PWR Stock Show Any Hints of Upside Potential?

Quanta remains a compelling long-term infrastructure play, supported by strong secular tailwinds, but its current valuation warrants a balanced investment stance. Its robust backlog growth, improving earnings outlook and solid cash flow generation reinforce its positioning as a key beneficiary of rising utility investments and grid modernization. Additionally, consistent upward earnings estimate revisions and superior return on equity highlight operational strength and shareholder value creation.

However, the premium valuation of this Zacks Rank #3 (Hold) stock is clouding investors’ judgment, especially in the near term, even if market tailwinds are mirroring the overvaluation. Any slowdown in project execution, delays in customer spending or macroeconomic headwinds could pressure growth expectations and trigger multiple compressions. Execution risks tied to large-scale projects, cost inflation and labor constraints also remain key concerns.

Thus, for now, investors may consider maintaining existing positions while awaiting a more attractive entry point for PWR stock. While long-term fundamentals remain intact, near-term upside appears balanced against valuation risks, making patience a prudent approach. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

Fluor Corporation (FLR): Free Stock Analysis Report

AECOM (ACM): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios