Quaker Houghton's Q3 2025 Outperformance: Margin Expansion and Market Share Gains Signal Resilience in Industrial Water Treatment Sector

Margin Expansion: A Strategic Win

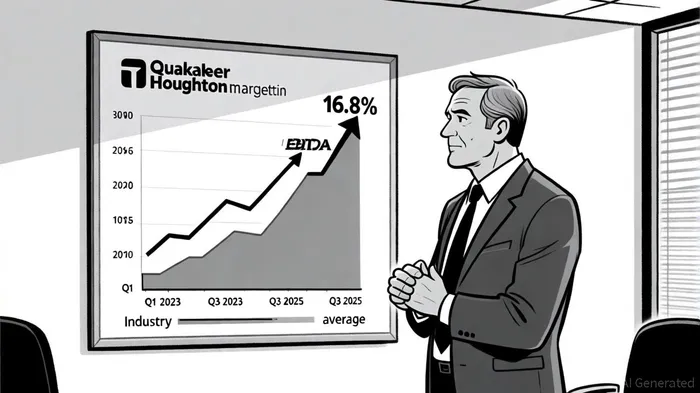

The company's adjusted EBITDA of $82.9 million in Q3 2025 reflects a 5% Y/Y increase, with margins expanding to 16.8%-a notable improvement from 15.22% in December 2024 and 16.12% in June 2024, according to Macrotrends' EBITDA margin data. This acceleration in margin performance is a direct result of disciplined cost management and a shift in product mix, despite a 2% decline in selling prices and product mix due to index-based customer contracts, as the company's press release notes. The ability to offset pricing pressures while maintaining profitability highlights Quaker Houghton's operational agility.

Market Share Gains: Asia/Pacific as a Catalyst

While Quaker Houghton's exact market share in the industrial water treatment sector remains undisclosed, its regional performance provides compelling indirect evidence. The Asia/Pacific segment saw an 8% increase in organic sales volumes, outpacing the 3% global average, as the press release reports. This outperformance aligns with the region's growing industrialization and infrastructure investments, where Quaker Houghton's tailored water treatment solutions are gaining traction. In contrast, softer demand in the Americas and EMEA segments-attributed to cyclical downturns in manufacturing-was more than offset by Asia/Pacific's momentum, according to the same press release.

Strategic Positioning for Long-Term Growth

Quaker Houghton's Q3 results also reveal a broader narrative of strategic reinvention. The company's focus on high-margin industrial water treatment applications-such as cooling tower management and membrane technologies-has enabled it to capture market share from less agile competitors. For instance, new business wins in Asia/Pacific accounted for 5% of global sales growth, signaling a proactive approach to securing long-term contracts in high-growth markets, as detailed in the company's press release.

According to the company's 2024 annual report, despite a third consecutive year of end-market contraction, Quaker Houghton achieved $1.84 billion in sales, with market share gains across all segments. This suggests that the company's Q3 2025 performance is not an isolated success but part of a sustained strategy to dominate niche industrial water treatment applications.

Risks and Opportunities

Investors should remain cognizant of near-term risks, including inflationary pressures on raw material costs and regulatory shifts in water treatment standards. However, Quaker Houghton's diversified geographic footprint and R&D investments in sustainable solutions-such as biodegradable coagulants-position it to navigate these challenges, the press release notes. The company's 8% organic sales growth in Asia/Pacific, coupled with its 16.8% EBITDA margin, indicates a strong foundation for capitalizing on the region's industrialization wave.

Conclusion

Quaker Houghton's Q3 2025 results exemplify a company that is not only weathering macroeconomic turbulence but actively reshaping its competitive landscape. By leveraging margin discipline, geographic diversification, and innovation in industrial water treatment, the firm is well-positioned to outperform peers in a sector poised for long-term growth. For investors, the combination of accelerating EBITDA margins and inferred market share gains presents a compelling case for sustained value creation.

Comentarios

Aún no hay comentarios