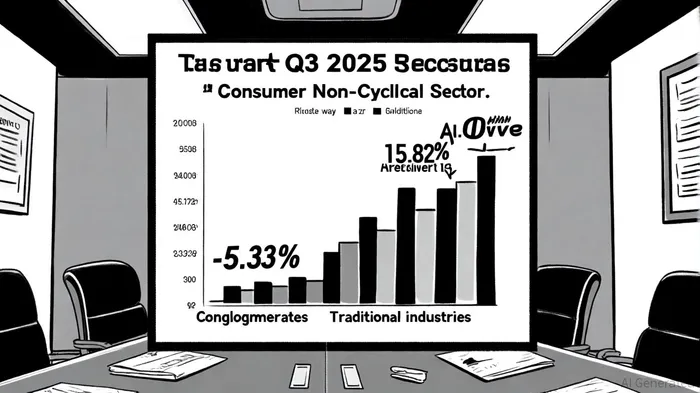

Q3 2025 Stock Market Analysis: Sector Rotation and Macroeconomic Tailwinds Reshape Investment Landscapes

The Q3 2025 stock market unfolded as a tale of two economies: one driven by AI-fueled innovation and resilient consumer demand, and the other weighed down by structural challenges in traditional sectors. According to a FutureStandard report, sector rotation in the quarter was stark, with Consumer Non-Cyclical leading the pack at a 15.82% return, followed by Consumer Discretionary, Capital Goods, Technology, Retail, and Healthcare. Conversely, Conglomerates (-5.33%), Utilities, and Financials lagged, reflecting a broader shift in capital toward industries aligned with macroeconomic tailwinds, the FutureStandard report noted.

Sector Rotation: Winners and Losers

The Department & Discount Retail industry emerged as a standout, surging 44.47%-a performance fueled by aggressive cost-cutting strategies and a rebound in low-income consumer spending, according to the FutureStandard report. Retail giants like Kohl'sKSS-- Corp, Macy'sM-- Inc, and Dillard'sDDS-- Inc capitalized on this trend, leveraging inventory optimization and digital transformation to attract price-sensitive shoppers, the report observed. Meanwhile, the Technology sector benefited from a resurgence in AI-related investments, with tech and media firms now accounting for over 40% of the S&P 500's market cap, the FutureStandard analysis showed.

On the flip side, the Tire Manufacturing industry plummeted by -16.90%, with The Goodyear Tire and Rubber Company bearing the brunt of supply chain disruptions and shifting demand toward electric vehicles, the FutureStandard report highlighted. This divergence underscores the growing importance of aligning with macroeconomic currents, as sectors tied to legacy infrastructure struggled against the tide.

Macroeconomic Tailwinds and Headwinds

The Federal Reserve's dovish pivot and global inflation moderation played a pivotal role in shaping Q3 dynamics. While U.S. short-term rates are expected to decline, inflation data remains a wildcard, keeping monetary policy in flux, the FutureStandard report noted. The bifurcated economic landscape-where wealthy consumers and AI-driven sectors thrive-contrasts sharply with challenges in housing, government spending, and low-end retail, per the same analysis.

Globally, new trade and immigration policies have introduced supply-side inflationary pressures, complicating central banks' efforts to normalize rates. However, according to the Global Macroeconomic Outlook Report, global economic growth is projected to stabilize at 2.42% in 2025, supported by fiscal expansion in key economies and improved financial conditions. Europe and the Middle East, in particular, are expected to see inflation decline to 5.43% by year-end, while the U.S. Federal Reserve's rate hold and the European Central Bank's cuts created a fragmented policy environment, the report added.

Strategic Implications for Investors

The Q3 rotation highlights the need for a nuanced approach to portfolio construction. Fidelity's Third Quarter 2025 update notes that U.S. stocks, though still elevated in valuation, remain anchored by AI-driven earnings growth. However, rising capital expenditures in tech could erode free cash flow, creating valuation risks for overexposed investors, the FutureStandard report cautioned.

For long-term value, diversification into non-U.S. equities and bonds appears compelling, as global markets offer more attractive yield profiles amid U.S. inflationary pressures, the Fidelity update suggested. Additionally, sectors like Healthcare and Retail, which demonstrated resilience in Q3, warrant closer scrutiny for their ability to weather macroeconomic volatility.

Conclusion

Q3 2025 reaffirmed the power of sector rotation as a tool for navigating macroeconomic uncertainty. While AI and consumer-driven industries thrived, traditional sectors like Conglomerates and Utilities faced headwinds. As investors look ahead, balancing exposure to high-growth AI-related assets with defensive plays in resilient sectors will be critical. The evolving interplay between policy shifts, inflation, and technological innovation will likely define the remainder of the year.

Comentarios

Aún no hay comentarios