Pricing Power and Valuation Dynamics in the Live Entertainment Sector: Investor Implications

The live entertainment sector has emerged as a resilient and high-growth investment opportunity in 2025, driven by robust pricing power and strategic control over venues. Companies like Live Nation EntertainmentLYV-- (LYV) have leveraged dynamic pricing models, venue expansion, and ticketing dominance to capture significant market share, even amid macroeconomic headwinds. For investors, understanding the interplay between pricing power, venue control, and valuation multiples is critical to assessing long-term potential and risks.

Pricing Power: Dynamic Strategies and Consumer Demand

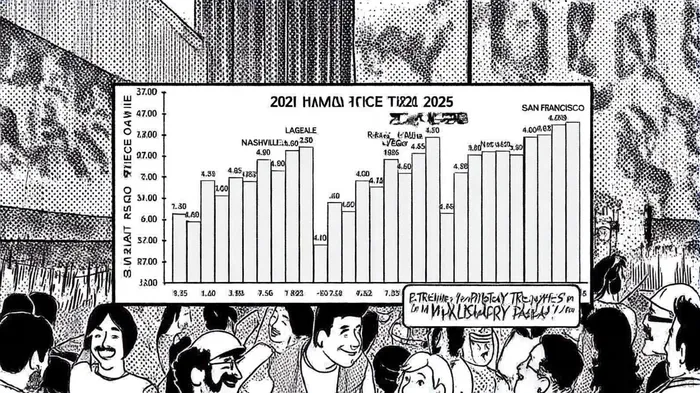

Concert ticket prices have surged by 20% since 2021, fueled by post-pandemic demand and dynamic pricing algorithms[1]. In 2025, cities like San Francisco see resale prices 29% above the multi-city average, while Nashville and Las Vegas offer more affordable options, with resale prices 25–27% below the average[2]. This geographic disparity underscores the effectiveness of dynamic pricing, which adjusts ticket costs based on demand, artist popularity, and venue capacity. Live NationLYV--, which controls 80% of major U.S. concert venues[3], has capitalized on this model, enabling premium pricing for high-demand events while maintaining affordability for budget-conscious attendees through tiered seating options[4].

Dynamic pricing has also amplified secondary market markups, with some resale tickets reaching several times their face value[2]. This trend reflects strong consumer demand for live experiences, particularly among younger demographics who prioritize experiential spending over material goods[1]. For investors, the ability to balance pricing power with accessibility is a key determinant of long-term profitability.

Venue Control: Expansion and Diversification

Live Nation's strategic expansion of its venue portfolio is a cornerstone of its growth strategy. The company plans to add 20 large-scale venues globally by 2026, aiming to accommodate an additional seven million fans annually[5]. This expansion is not limited to the U.S.; international markets like Latin America and Asia Pacific are critical growth drivers, with new stadiums in Colombia and Mexico already generating strong returns[6]. By controlling both ticketing and venue operations, Live Nation creates a closed-loop ecosystem that enhances pricing power and reduces reliance on third-party intermediaries[3].

Venue ownership also allows for diversified revenue streams. Premium offerings such as luxury boxes, upscale dining, and VIP ticketing contribute to higher profit margins[5]. For example, Live Nation's sponsorship-adjusted operating income rose 13% to $764 million in 2024, supported by 95% of its 2025 sponsorship revenue already secured[6]. This diversification mitigates risks associated with talent costs, which account for 75–85% of total ticket sales revenue[7].

Valuation Dynamics: Multiples and Market Leadership

Live Nation's valuation metrics reflect its dominant market position. As of 2025, the company trades at an EV/Revenue multiple of 1.7x and an EV/EBITDA of 23.7x[8], significantly higher than industry peers. These multiples are justified by its high-margin Ticketmaster business, which controls over 60% of the U.S. ticketing market[3], and its ability to generate consistent deferred revenue. For instance, Live Nation reported $5.4 billion in concert-related deferred revenue and $270 million from Ticketmaster in Q1 2025[9].

However, valuation optimism is tempered by regulatory risks. The U.S. Department of Justice (DOJ) and multiple states have filed antitrust lawsuits against Live Nation, alleging anti-competitive practices through its control of venues and ticketing[10]. If the company is forced to divest Ticketmaster or face operational restrictions, its valuation multiples could compress. Investors must weigh these risks against the company's strong balance sheet, with over 90% of debt at fixed rates[6], and its international expansion potential.

Regulatory and Competitive Risks

The DOJ lawsuit highlights the fragility of Live Nation's pricing power. Critics argue that its 80% control of major venues enables price manipulation and suppresses competition[10]. While the company defends its strategies as market-driven, the outcome of this case could reshape the industry's pricing dynamics. Competitors like AEG and Spectra, which focus on niche segments of the market, lack the integrated ecosystem to challenge Live Nation's dominance[11]. However, regulatory intervention could create opportunities for smaller operators to gain market share.

Investor Implications

For investors, the live entertainment sector offers a compelling mix of growth and risk. Live Nation's ability to maintain pricing power while expanding its venue network positions it as a leader in a $651.53 billion U.S. live events market projected to grow at 4.9% CAGR through 2032[12]. However, macroeconomic factors—such as rising interest rates and inflation—could dampen discretionary spending on live events[6]. Additionally, the company's $8.19 billion in 2024 debt[13] raises concerns about leverage in a high-interest-rate environment.

A diversified approach to investing in the sector may mitigate these risks. While Live Nation's valuation reflects its market leadership, investors should also consider companies that focus on technology-driven ticketing solutions or regional venue operators less exposed to regulatory scrutiny.

Conclusion

The live entertainment sector's valuation dynamics are shaped by pricing power, venue control, and regulatory risks. Live Nation's dominance in ticketing and venue operations has driven robust financial performance, but its future depends on navigating antitrust challenges and macroeconomic pressures. For investors, the key is to balance the sector's growth potential with its inherent vulnerabilities, ensuring that valuations align with both current performance and long-term sustainability.

Comentarios

Aún no hay comentarios