PrairieSky Royalty Ltd (PREKF) Q1 2025 Earnings: Record Oil Volumes Drive Growth Amid Challenges

PrairieSky Royalty Ltd (PREKF) delivered a robust Q1 2025 performance, anchored by record oil production and strategic asset acquisitions. However, the quarter also highlighted vulnerabilities tied to natural gas markets and elevated payout ratios. Below is a deep dive into the key takeaways and their implications for investors.

Financial Highlights: Strong Cash Flow, Elevated Payouts

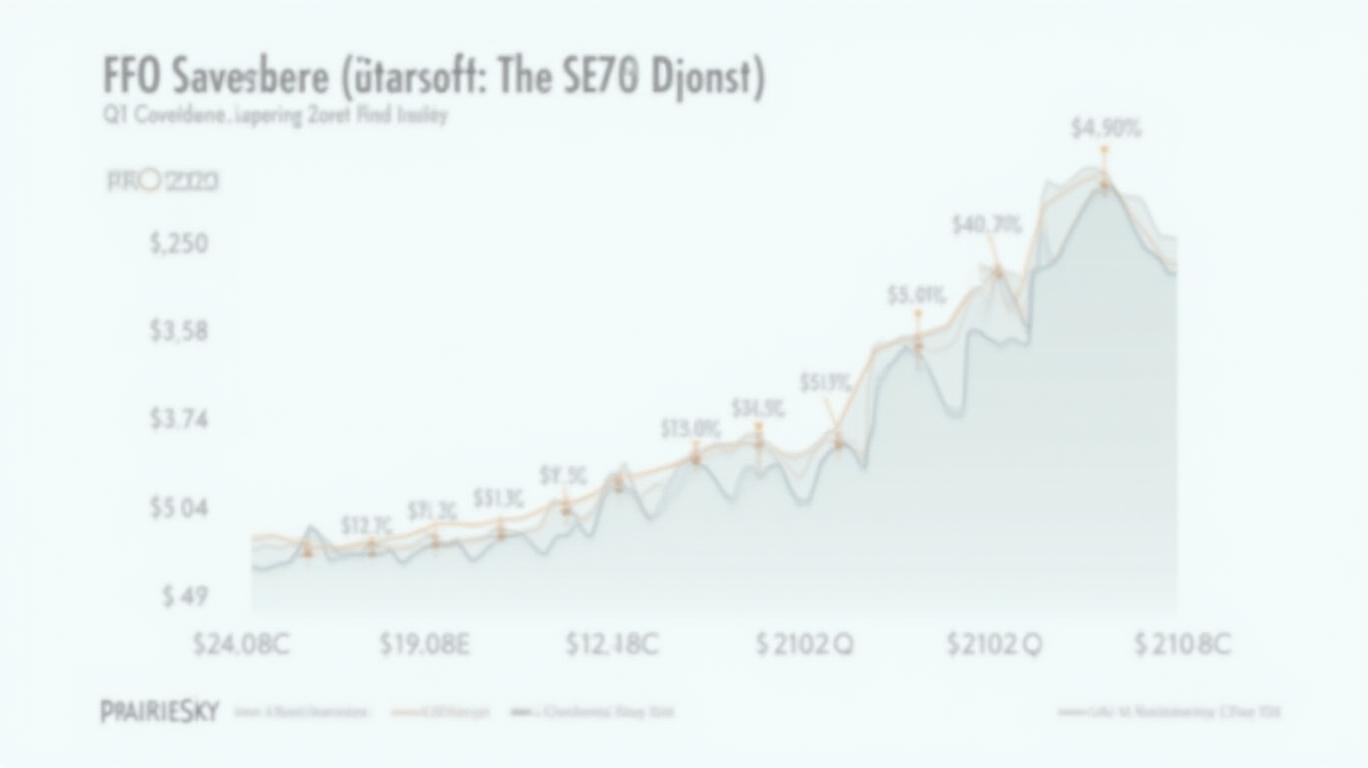

PrairieSky’s Q1 2025 FFO reached $85.8 million, supporting a $0.26 per share dividend (71% payout ratio) and $90 million in share buybacks. While FFO rose 3% year-over-year, the payout ratio’s increase from 61% in Q1 2024 raises questions about capital flexibility.

The company’s net debt rose to $258.8 million, driven by share repurchases and asset acquisitions. Management emphasized balance sheet strength, noting no near-term debt maturities, but incremental borrowing could strain liquidity if oil prices remain depressed.

Operational Strength: Record Oil Volumes and Leasing Momentum

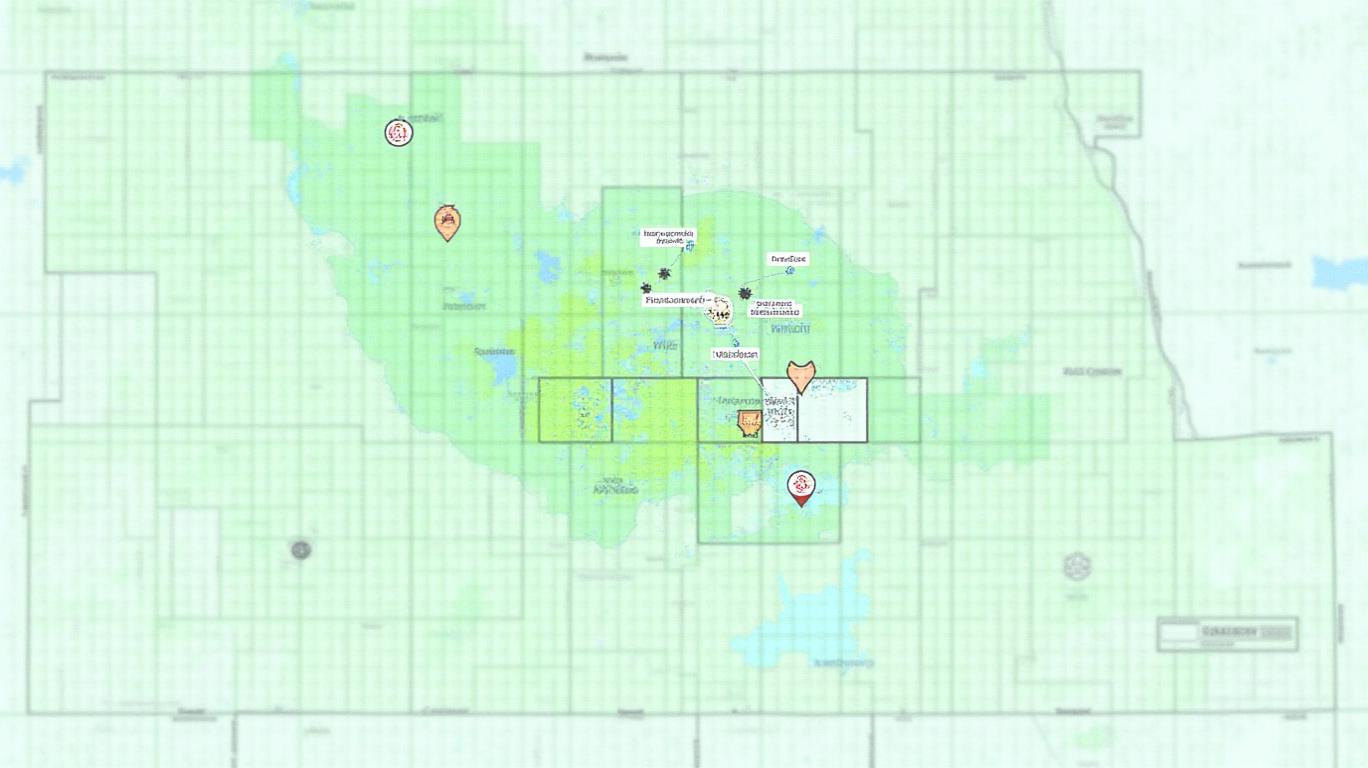

- Oil Production Surge: Oil royalty volumes hit 13,502 barrels per day (bpd), a record high, fueled by activity in the Clearwater, Mannville, and Duvernay plays.

- Strategic Acquisitions: The $50 million Petro-Canada fee title package in Southeast Saskatchewan adds 9.7 million acres of low-leased land, positioning PrairieSky to capitalize on future drilling.

- Lease Activity: 52 new leases with 39 operators generated $5 million in bonuses, underscoring demand for PrairieSky’s acreage in oil-rich basins.

Growth Catalysts: Technology and Investor Day Momentum

PrairieSky is leveraging horizontal drilling and liner circulation techniques to unlock thousands of new drilling locations, particularly in heavy oil plays like the Mannville stack. Management projects 30–50% growth in Mannville production this year, with the play nearing Clearwater volumes.

The upcoming May 14 Investor Day will reveal a new royalty asset book, including Williston Green and Duvernay growth targets. Executives also hinted at hundreds of new locations in heavy oil assets, with a focus on CHOPS (Cold Heavy Oil Production with Sand) technology.

Risks and Challenges

- Natural Gas Declines: Gas volumes fell 10% to 55.9 MMcf/d, partly due to cold weather downtime. Weak pricing ($1.73/Mcf vs. $2.02/Mcf in Q1 2024) exacerbated revenue pressure.

- Oil Price Volatility: Post-Q1 oil price declines (e.g., WCS differential widening) threaten drilling activity, though management cited $50/bbl resilience for dividends.

- Payout Ratio Concerns: The 71% payout ratio limits room for reinvestment, though CFO Pam Cazell stressed dividends remain sustainable below $50/bbl.

Market Reaction and Valuation

PrairieSky’s stock rose 1.06% post-earnings to $22.95, but it remains near its 52-week low of $30.85. The 6.9% dividend yield and 12-year streak of dividend growth offer downside protection, but valuation multiples like EV/EBITDA (8.5x) suggest skepticism about near-term growth.

Conclusion: Opportunistic Buy with Risks

PrairieSky’s Q1 2025 results underscore its ability to drive oil-focused growth through strategic leases and technology adoption. The $50M Petro-Canada acquisition and Mannville/Duvernay momentum position it for long-term gains. However, investors must weigh these positives against gas market headwinds, elevated debt, and $70/bbl oil dependency for aggressive capital allocation.

The stock’s 6.9% dividend yield and decades of inventory make it an attractive high-yield play, but a wait-and-see stance is prudent until oil prices stabilize. PrairieSky’s May 14 Investor Day will be critical in re-rating the stock, as it could validate management’s 3–50% production growth targets and $250M+ annual FFO vision.

Final Takeaway: PrairieSky offers asymmetric upside for investors willing to tolerate commodity risk, but its valuation and payout structure demand caution in volatile markets.

Comentarios

Aún no hay comentarios